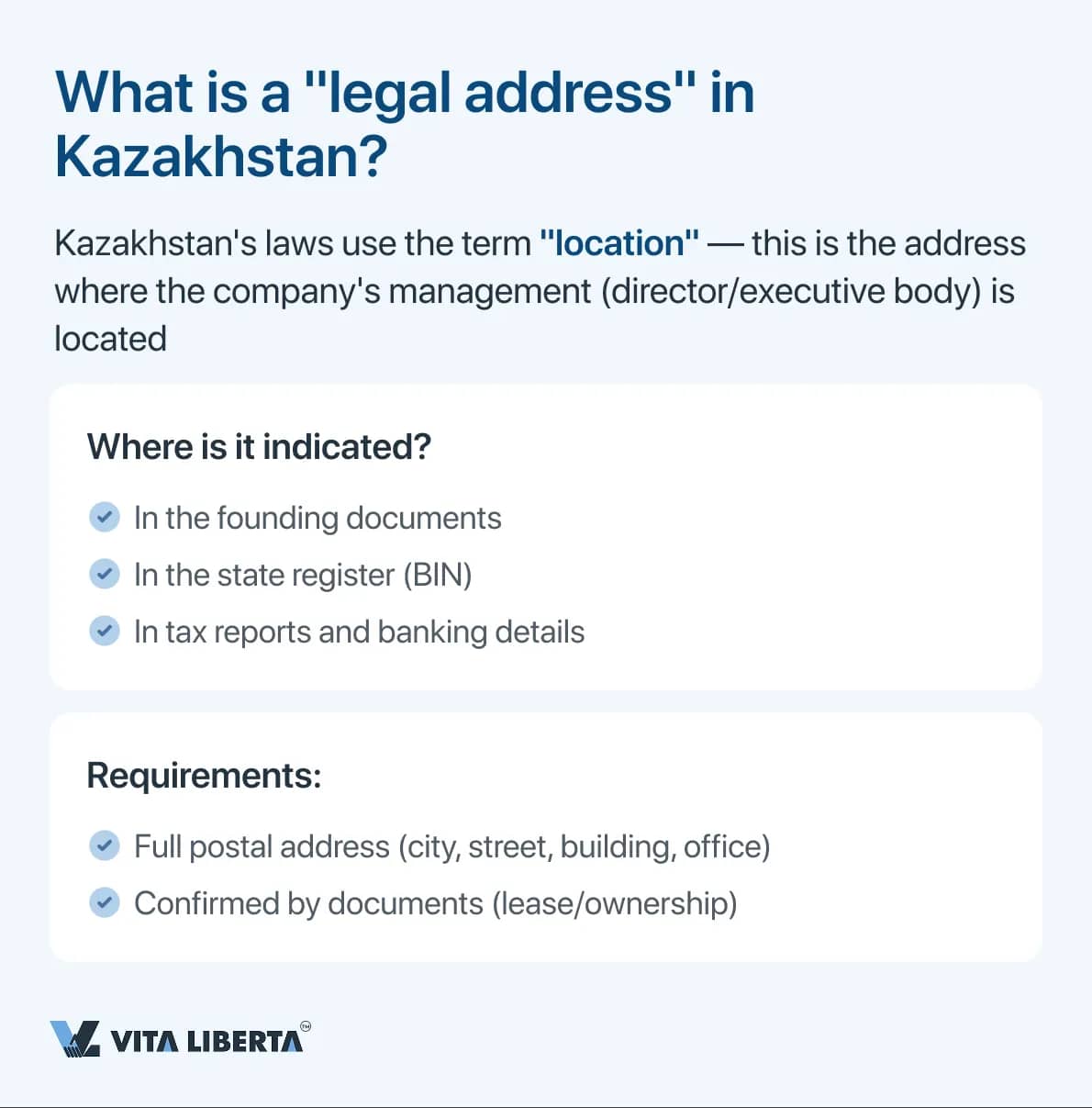

Among entrepreneurs, there is still a prevailing belief that a legal address is just a line in the register, an abstraction unrelated to the real state of affairs. However, in the reality of 2026, this approach is a risky illusion. The State Revenue Committee (SRC) is empowered to conduct "face-to-face meetings" with businesses, and the reason for this could be something as simple as a missing sign or a locked door. Let's take a detailed look at why fiscal authorities visit addresses, how such a "raid" proceeds, and what an empty office means for a director.

Triggers for a Visit: Why Would the Tax Authority Decide to Check on Your Company?Contrary to popular belief, the tax authority does not conduct inspections "according to a plan" or as a scare tactic. There are strictly defined legal grounds upon which an inspector is required to personally verify the existence of a company. In 2026, there are several such grounds:

- "Dead" correspondence. If registered letters (inspection reports, debt notifications, orders) are regularly returned to the sender marked "addressee absent" or "storage period expired," this is an automatic alarm signal. For the tax authority, this is equivalent to a statement: "The company is hiding or not conducting business."

- "VAT Payer" status. If your company works with VAT, you are in a high-risk group. Inspectors have the right to visit you for basic verification: does the entity claiming a tax refund from the budget actually exist? An exception is made only for companies in bankruptcy or official downtime.

- Ignoring the "digital." After a desk (remote) control, the tax authority often sends a notice to eliminate violations. If a businessman ignores this requirement in electronic format, the next step is a physical visit.

- "Dormant" status. Companies that file zero reports and are listed as inactive come under suspicion. The tax authority needs to distinguish between legitimate "hibernation" and an actually abandoned business.

Inspection Report: How the Visit Proceeds and What Inspectors RecordImagine the situation: an inspector arrives at the registered address of an LLP. What happens next? This is not a search, but an inspection. The result is an official report..

- Positive scenario: The door is opened, the office is in place, and a sign is present. The inspector notes "confirmed" and leaves. The company continues to operate peacefully.

- Negative scenario: The door is locked, and instead of an office, there is a residential apartment or an empty premises.

If the absence of the company at the address is recorded, a legal mechanism is triggered:

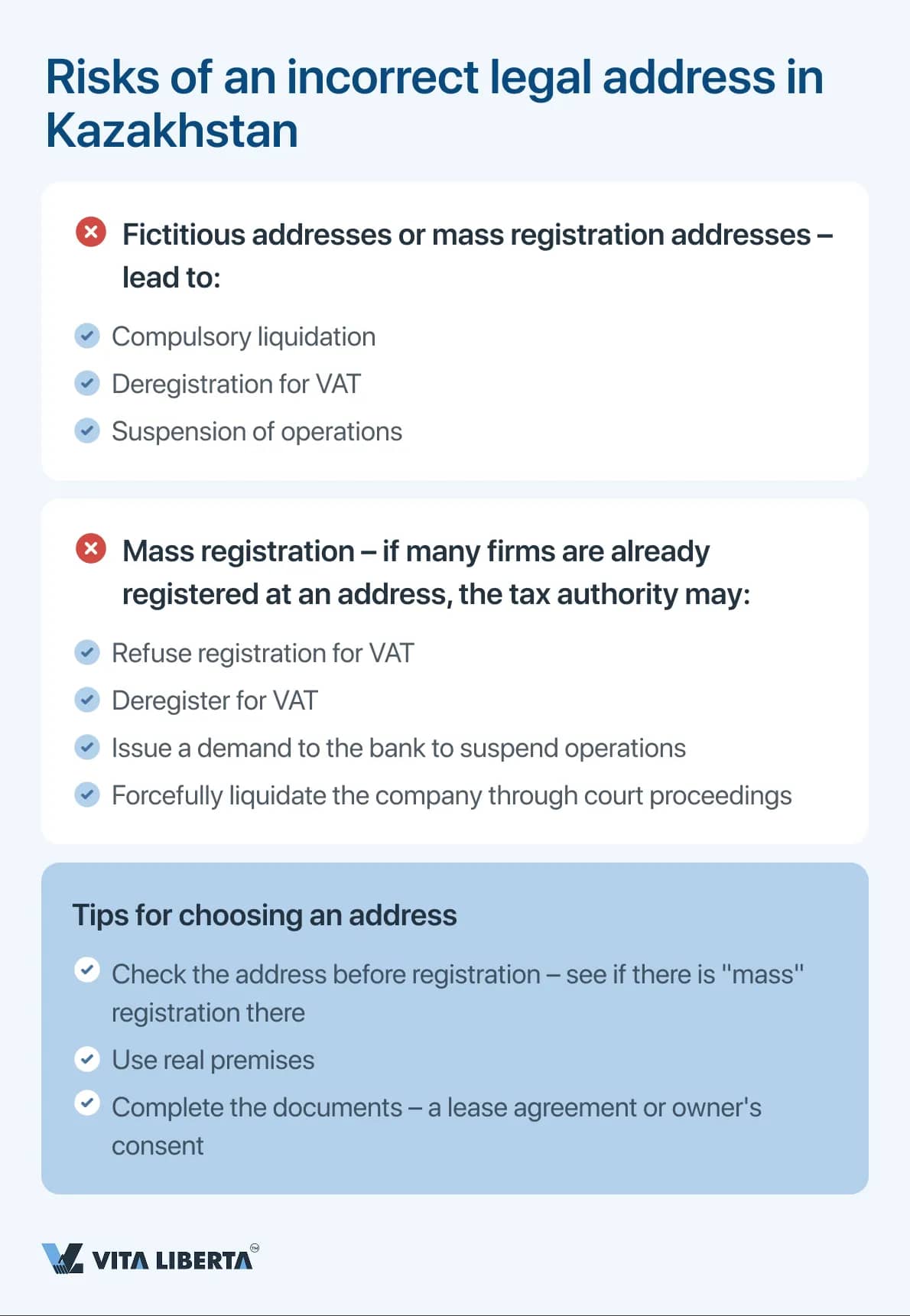

The very next day after the report is drawn up, the company is placed on a "blacklist" — the register of entities absent from their legal address. This is a mark instantly visible to banks (risking account freezes or loan denials) and counterparties (who may break off deals, suspecting a shell company).

Special Regime for VAT Payers: 20 Days for RehabilitationFor those working with VAT, the procedure is stricter. If a company is not found at its address, it is issued an official summons to the tax authority.

- Deadline: You must appear within 20 working days from the date the notice was sent.

- Mission: You will have to personally come to the inspector, write an explanatory note (why you were not there), and provide documents confirming the actual existence of the business (lease agreement, ownership certificate, photo report).

- Important: The inspector has the right to verify originals and keep copies.

The Price of Silence: From Account Freezes to Substantial FinesIgnoring the summons or failing to appear without a valid reason triggers a sanctions conveyor. The consequences come quickly and tangibly:

- Account freeze. The tax authority blocks all debit transactions on bank accounts. You will not be able to pay salaries, settle with suppliers, or pay taxes (except those going to the budget).

- VAT deregistration. If accounts are frozen or blocking does not help, the company is simply removed from the VAT payer register. For many types of businesses, this effectively halts operations and loses key partners.

- Administrative fine (Article 466 of the Administrative Code). This is not just a "warning" but very specific money, tied to the Monthly Calculation Index (MCI) for 2026 (1 MCI = 4,325 tenge):

- For a director: from 5 to 30 MCI (21,625 — 129,750 tenge).

- For small businesses: from 10 to 30 MCI (43,250 — 129,750 tenge).

- For medium businesses: from 20 to 50 MCI (86,500 — 216,250 tenge).

- For large businesses: from 30 to 100 MCI (129,750 — 432,500 tenge).

The Point of No Return: When the Situation Smells of LiquidationFines and freezes are only half the problem. The worst is compulsory closure of the business through court. This is possible when three circumstances coincide (according to the Civil Code):

- The company is physically absent from its address.

- It has no active directors or founders (no one is managing it).

- This condition has lasted for more than one year.

If at least one condition is missing (e.g., there is a director, but no office), the court will most likely refuse liquidation. But if the company is abandoned and empty for more than a year — it has virtually no chance of survival. The court decides on compulsory dissolution.

To prevent your business from falling into the "trap" of an absent address, follow three rules:

- The address must be "alive." Mail must be deliverable there, and there must be people (at least a courier or security guard) capable of receiving a notification.

- Temporary absence. If the office is empty (renovation, holidays), set up mail forwarding or post a sign on the door with a contact phone number and information on where to find you.

- Moving means re-registration. Changed location? Immediately amend the founding documents. Do not rely on "maybe it will pass." In 2026, the tax authority has learned to effectively find and punish those who hide behind fictitious addresses.