Education

Accounting Registration of a Branch and Representative Office of a Foreign Company in Kazakhstan – A Quick and Reliable Solution for Entering the Market

Get a free consultation from an expert on opening branches and representative offices in Kazakhstan. We will consider your unique situation in detail and guide you step-by-step through the entire process of creating a separate subdivision - from preparing the constituent documents of the parent company to opening a settlement account in a Kazakhstani bank and properly organizing tax accounting.

Cost of Accounting Registration of a Branch

You can choose one of three business registration packages based on your personal preferences

Full

97 500 ₽

Payment in ₸, ₽, €, $, ¥

Verification of foreign legal entity documents

Preparation of the decision / minutes on the establishment of the branch

Preparation of the regulations on the branch of a foreign company

Preparation of the order appointing the branch head

Preparation of the power of attorney for the director of the foreign company's branch

Submission of the application to obtain an Individual Identification Number (IIN) for an individual

Submission of the application to obtain Electronic Digital Signature (EDS) keys for an individual

Verification of the Proposed Name of the Branch of a Foreign Company Submitted by the Client

Assistance in selecting General Classifier of Economic Activities (OKED) codes

Preparation of the application for state registration of the branch of a foreign company

Премиум

147 500 ₽

Payment in ₸, ₽, €, $, ¥

Verification of foreign legal entity documents

Preparation of the decision / minutes on the establishment of the branch

Preparation of the regulations on the branch of a foreign company

Preparation of the order appointing the branch head

Preparation of the power of attorney for the director of the foreign company's branch

Submission of the application to obtain an Individual Identification Number (IIN) for an individual

Submission of the application to obtain Electronic Digital Signature (EDS) keys for an individual

Verification of the Proposed Name of the Branch of a Foreign Company Submitted by the Client

Preparation of the application for state registration of the branch of a foreign company

Selection of office premises for subsequent lease

Assistance in the production of the seal for the registered branch of the foreign company

Submission of the application to obtain the registration certificate (public key certificate) of the EDS for the branch's head

Assistance in opening a current account for the branch of the foreign company with a bank

Registration of one employment contract between the branch of the foreign company and its director

Preparation and submission of Form 1-NP report

Бизнес-профессионал

167 500 ₽

Payment in ₸, ₽, €, $, ¥

Verification of foreign legal entity documents

Preparation of the decision / minutes on the establishment of the branch

Preparation of the regulations on the branch of a foreign company

Preparation of the order appointing the branch head

Preparation of the power of attorney for the director of the foreign company's branch

Submission of the application to obtain an Individual Identification Number (IIN) for an individual

Submission of the application to obtain Electronic Digital Signature (EDS) keys for an individual

Verification of the Proposed Name of the Branch of a Foreign Company Submitted by the Client

Assistance in selecting General Classifier of Economic Activities (OKED) codes

Preparation of the application for state registration of the branch of a foreign company

Selection of office premises for subsequent lease

Assistance in the production of the seal for the registered branch of the foreign company

Submission of the application to obtain the registration certificate (public key certificate) of the EDS for the branch's head

Assistance in opening a current account for the branch of the foreign company with a bank

Registration of one employment contract between the branch of the foreign company and its director

Preparation and submission of Form 1-NP report

Setup of the 1С database for the branch of the foreign company

Accounting services for the registered branch of the foreign company — 1 month

Legal services for the registered branch of the foreign company — 1 month

Professional Registration and Support of LLPs - We Are Always in Touch

We value teamwork and achieve the highest results by applying an individual approach to each client.

Madina

Head of the Legal Department, expert in LLP registration and business support

Aneliya

The chief lawyer is a professional with deep knowledge of Kazakhstani legislation

Education

M. S. Narikbaev KAZGUU University, Master of Laws

Aniya

A lawyer is your reliable assistant in matters of business registration and management

Education

M. S. Narikbaev KAZGUU University, Master of Laws

Testimonial from a Satisfied Client

Congratulations from Our Partner Bank

"Vita Liberta" LLP and the March 8 Holiday

The Moment When Paying Taxes Brings Joy

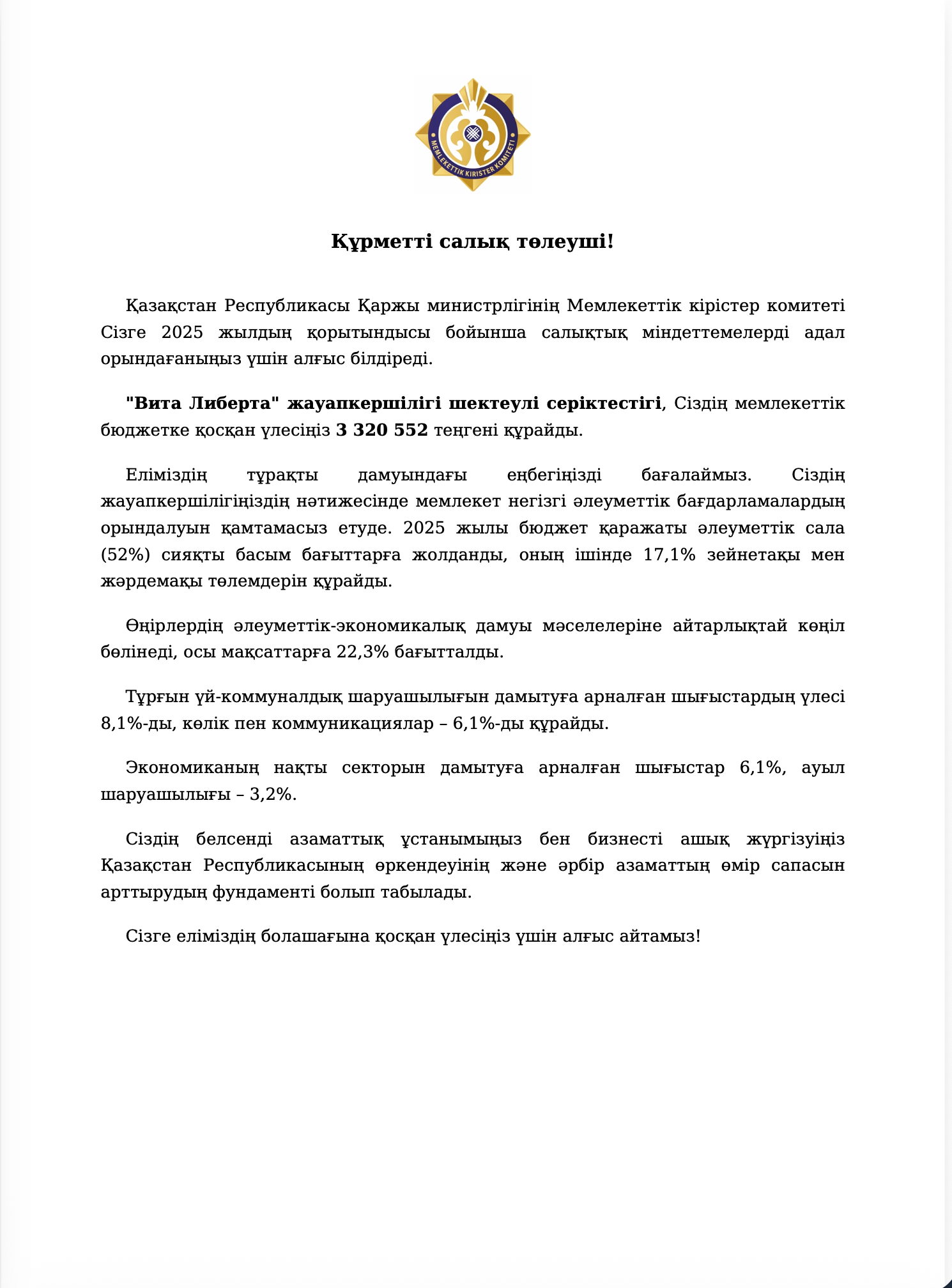

Usually, the words "tax," "State Revenue Committee," and "payment" cause a slight headache for an entrepreneur. But this document is one of those rare exceptions. Seeing it makes you want to take a screenshot and send it to the chat with the caption "Just pleasant!"

The 3,320,552 tenge our company paid to the budget for 2025 is not just a number.

It is 52% going to the social sphere. It is pensions, benefits, schools.

It is 22% going to the regions, 8% to housing and communal services, 6% to roads and communications.

Even 3% to agriculture — perhaps somewhere a new tractor was bought or a water pipe was repaired.

Of course, we understand: tax is not charity, it's an obligation.

But when you see that the fruit of your labor turns into someone's payment, someone's asphalt, someone's housing - something inside resonates.

Thank you for noticing! Being among those who don't hide but contribute to the common cause is gratifying.

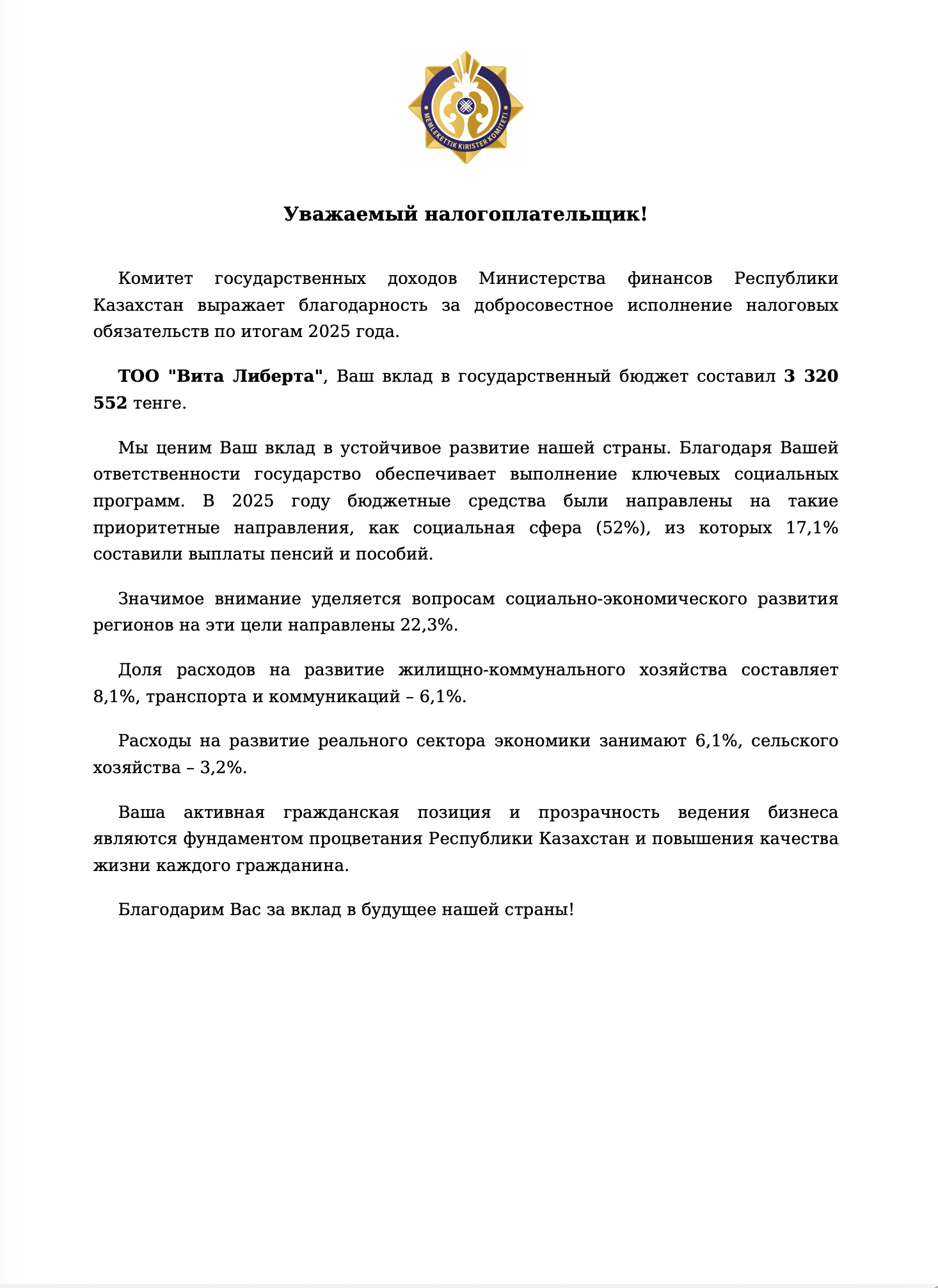

The 3,320,552 tenge our company paid to the budget for 2025 is not just a number.

It is 52% going to the social sphere. It is pensions, benefits, schools.

It is 22% going to the regions, 8% to housing and communal services, 6% to roads and communications.

Even 3% to agriculture — perhaps somewhere a new tractor was bought or a water pipe was repaired.

Of course, we understand: tax is not charity, it's an obligation.

But when you see that the fruit of your labor turns into someone's payment, someone's asphalt, someone's housing - something inside resonates.

Thank you for noticing! Being among those who don't hide but contribute to the common cause is gratifying.

Professional Liability Insurance

Our professional liability is insured by JSC IC "NOMAD Insurance"

(Contract No. 207-25-14142055/811884DS).

Insurance coverage includes:

The insurance applies during the provision of professional services requiring special knowledge and qualifications.

(Contract No. 207-25-14142055/811884DS).

Insurance coverage includes:

- Compensation for harm caused to life and/or health

- Compensation for damage caused to the property of third parties

The insurance applies during the provision of professional services requiring special knowledge and qualifications.

Insurance Policy

Webinar: A Comprehensive Guide to Legal Aspects, Taxation, and Banking Operations in Kazakhstan

Join our webinar "Legal Aspects, Taxation, and Banking Operations in Kazakhstan" and get comprehensive information from experts at Vita Liberta and Jusan Bank. Learn all the important nuances of successfully doing business in Kazakhstan and ask your questions live! Don't miss the opportunity to increase your competence and confidence in your affairs.

Advantages of Doing Business in Kazakhstan

Stages of Registering a Non-Profit Organization (NPO)

1. Collection of documents

Gathering the necessary documents and preparing a power of attorney (if necessary)

2. Choosing an address

Selecting the most suitable address/office for your company

3. Preparation of documents

Preparing a complete set of constituent documents

4. Name verification

Checking the availability of your company's chosen name

5. IIN/BIN, EDS

Obtaining and processing IIN/BIN and electronic digital signature

6. Choosing a bank

Selecting the most suitable bank based on terms and services

7. Bank account

Preparing documents for opening a bank account

8. Accounting

Setting up online accounting and reporting submission

9. Legal support

Full legal support for your company

Answers to Frequently Asked Questions

Concepts of Branch and Representative Office in Kazakhstan

When a business outgrows the boundaries of a single office and begins to develop new territories, the company faces the question: in what format should this presence be organized? Kazakhstani law offers several options, each with its own legal nature, scope of authority, and establishment procedure.

Branch: An Authorized Representative with a Broad Mandate

What is a branch from a legal perspective?

A branch is the most universal form of territorial separation. The law defines it as a subdivision located outside the location of the parent company, which assumes the performance of all or part of its functions, including the functions of a representative office. The concept of "functions" here includes representative activities.

The key characteristic of a branch is its multifunctionality. Unlike other forms, a branch is not limited to a single task. It can simultaneously:

Practical significance of the branch form

For business, a branch is convenient because it allows transferring the entire spectrum of activity to a new territory. A production workshop, a trading house, a service center - all of this can be organized in the form of a branch. The head of the branch has broad powers defined in the regulations and the power of attorney, allowing for prompt resolution of issues without constant coordination with the head office.

Representative Office: Focus on Legal Presence

Legal nature of a representative office

A representative office is a more specialized form of separation. It is also established outside the location of the parent company, but its tasks are concentrated in the legal and communications spheres.

The law defines a representative office as a subdivision intended for:

Limitations on the activities of a representative office

Legislative acts may establish cases where a representative office is not entitled to perform certain legal actions. These are exceptions that confirm the general rule: in all other respects, a representative office has all the necessary powers to perform its functions.In practice, representative offices are often established by large foreign companies for which permanent presence in Kazakhstan is important for coordinating projects, but which do not plan to open full-fledged production or trade facilities here.

Branch: An Authorized Representative with a Broad Mandate

What is a branch from a legal perspective?

A branch is the most universal form of territorial separation. The law defines it as a subdivision located outside the location of the parent company, which assumes the performance of all or part of its functions, including the functions of a representative office. The concept of "functions" here includes representative activities.

The key characteristic of a branch is its multifunctionality. Unlike other forms, a branch is not limited to a single task. It can simultaneously:

- conduct production activities;

- engage in trade or services;

- represent the interests of the parent company;

- enter into transactions on its behalf;

- carry out any other actions within the competence of the organization that created it.

Practical significance of the branch form

For business, a branch is convenient because it allows transferring the entire spectrum of activity to a new territory. A production workshop, a trading house, a service center - all of this can be organized in the form of a branch. The head of the branch has broad powers defined in the regulations and the power of attorney, allowing for prompt resolution of issues without constant coordination with the head office.

Representative Office: Focus on Legal Presence

Legal nature of a representative office

A representative office is a more specialized form of separation. It is also established outside the location of the parent company, but its tasks are concentrated in the legal and communications spheres.

The law defines a representative office as a subdivision intended for:

- protecting the interests of the organization that created it;

- representing these interests before third parties;

- carrying out transactions and other legally significant actions on behalf of the company.

Limitations on the activities of a representative office

Legislative acts may establish cases where a representative office is not entitled to perform certain legal actions. These are exceptions that confirm the general rule: in all other respects, a representative office has all the necessary powers to perform its functions.In practice, representative offices are often established by large foreign companies for which permanent presence in Kazakhstan is important for coordinating projects, but which do not plan to open full-fledged production or trade facilities here.

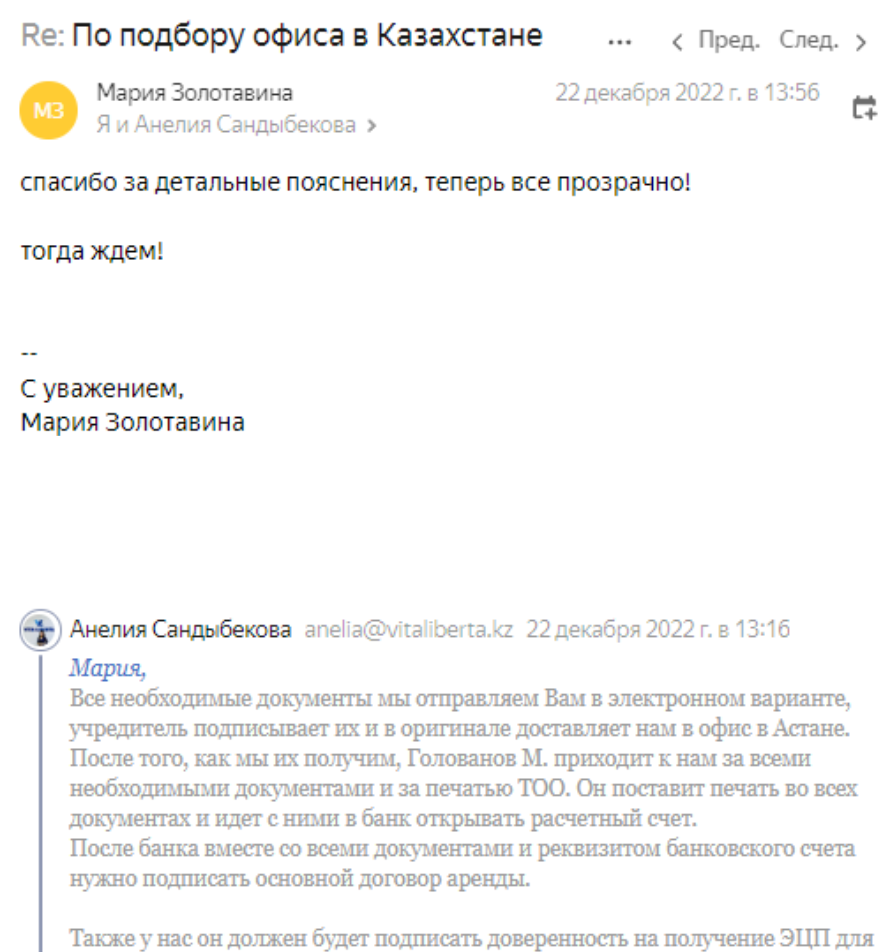

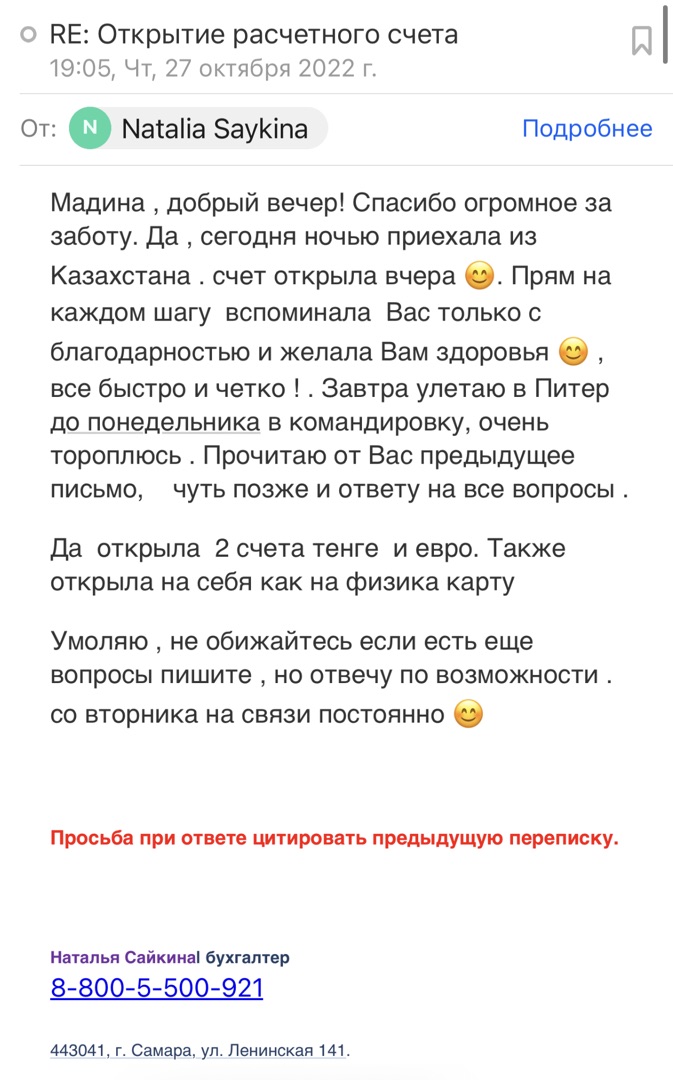

The Concept of Accounting Registration of Branches and Representative Offices in Kazakhstan

A branch or representative office does not have the status of an independent organization. They do not have their own charter capital, cannot be founders of other companies, and do not own property. All rights and obligations arising from their activities belong directly to the parent company. However, to operate legally, open bank accounts, hire employees, and interact with government bodies, a branch or representative office must undergo accounting registration and receive official recognition from the state.

What Does the Accounting Registration Procedure Include?

Accounting registration is not limited to simply making an entry in a register. The legislator has included several sequential stages in it, each with independent significance.

Verification of documents' compliance with the law

The first and most important stage is the analysis of the materials submitted by the applicant. The registering body is obliged to check how well the documents submitted for accounting registration comply with the requirements of Kazakhstani legislation.

This verification concerns not only the formal completeness of the package but also its content. It is assessed whether the regulations on the branch or representative office are correctly executed, whether the head is vested with the necessary powers, and whether the constituent documents of the parent company are properly legalized. If foreign documents require an apostille or consular legalization, the presence of these marks is checked.

The purpose of the verification is to prevent the registration of subdivisions that are established in violation of the established procedure or whose activities may contradict the law. This is a filter that screens out unscrupulous or unprepared applicants.

Issuance of a Business Identification Number

If the verification is successful, the branch or representative office is issued a certificate of accounting registration. Simultaneously, the structure is assigned a business identification number — the BIN, which the subdivision will indicate in all official documents.

For a branch or representative office, the BIN serves the same function as for a legal entity. It is a unique digital code that allows identifying the structure when paying taxes, opening bank accounts, including contracts, and interacting with government bodies. Without a BIN, a branch is not considered to be operating legally, even if the parent company has existed for many years and has an impeccable reputation.

Entering data into the National Register

The final stage of the procedure is entering information about the registered subdivision into the National Register of Business Identification Numbers. This is a unified state database where information is collected on all operating subjects on the territory of Kazakhstan that have a BIN.

Entry into the register has important public significance. Any interested counterparty can use open sources to check whether this subdivision actually exists, when it was registered, who its head is, and whether it is in the process of liquidation. This increases the transparency of business transactions and reduces the risks of fraud.

Legal Status of a Registered Subdivision

After undergoing accounting registration, a branch or representative office acquires official status, but this status has its limitations.

Operating without the status of a legal entity

The law specifically emphasizes: branches and representative offices are subject to accounting registration without the rights of a legal entity. This means they do not become independent participants in civil transactions.

A branch cannot acquire property in its own name, be a plaintiff or defendant in court, or issue powers of attorney in its own name. All transactions concluded by the head of the branch are considered transactions of the parent company. All claims arising from the branch's activities are directed to the parent organization. All assets used by the branch belong to the parent company.

Such a structure creates certain risks for counterparties, as they have to assess the solvency not of the branch itself, but of its parent structure, which may be located in another country. At the same time, this gives advantages to the parent company, allowing it to manage risks and assets centrally.

Scope of authority of a registered subdivision

Despite the lack of legal entity status, a registered branch or representative office has a certain set of powers necessary for its functioning.

Practical Aspects of Accounting Registration

The moment the obligation arises

The obligation to undergo accounting registration for a branch or representative office arises from the moment activities actually begin on the territory of Kazakhstan. The law does not require preliminary registration before the subdivision starts operating. However, delaying registration is also not allowed — carrying out the functions of a branch or representative office without registration entails administrative liability.

Consequences of non-registration

If a branch or representative office operates without accounting registration, its entire activity is considered illegal. Contracts concluded on behalf of such a subdivision may be declared invalid. The head risks being held administratively liable. Additionally, the tax service may make additional tax assessments based on the assumption that activities were conducted but taxes were not paid.

Difference from registering legal entities

It is important to understand the difference between the accounting registration of a branch and the registration of a subsidiary company (LLP). A subsidiary company is an independent legal entity with its own charter capital, its own balance sheet, and its own responsibility. Its registration is subject to the general rules for creating legal entities. A branch, on the other hand, is simply a separate subdivision, and the procedure for legalizing it is significantly simpler, but its legal status is also narrower.

Conclusion

Accounting registration of branches and representative offices in Kazakhstan is a mandatory administrative procedure that includes checking documents, issuing a BIN, and entering information into the National Register. A registered subdivision is not a legal entity but receives official recognition and the opportunity to operate legally.For a business, this means that when opening a branch or representative office, one cannot limit oneself to internal corporate procedures. It is necessary to follow the path of interaction with the state established by law, gather a properly executed package of documents, and obtain a certificate of accounting registration. Only after this can the subdivision be considered legally operating and begin to perform its functions.

What Does the Accounting Registration Procedure Include?

Accounting registration is not limited to simply making an entry in a register. The legislator has included several sequential stages in it, each with independent significance.

Verification of documents' compliance with the law

The first and most important stage is the analysis of the materials submitted by the applicant. The registering body is obliged to check how well the documents submitted for accounting registration comply with the requirements of Kazakhstani legislation.

This verification concerns not only the formal completeness of the package but also its content. It is assessed whether the regulations on the branch or representative office are correctly executed, whether the head is vested with the necessary powers, and whether the constituent documents of the parent company are properly legalized. If foreign documents require an apostille or consular legalization, the presence of these marks is checked.

The purpose of the verification is to prevent the registration of subdivisions that are established in violation of the established procedure or whose activities may contradict the law. This is a filter that screens out unscrupulous or unprepared applicants.

Issuance of a Business Identification Number

If the verification is successful, the branch or representative office is issued a certificate of accounting registration. Simultaneously, the structure is assigned a business identification number — the BIN, which the subdivision will indicate in all official documents.

For a branch or representative office, the BIN serves the same function as for a legal entity. It is a unique digital code that allows identifying the structure when paying taxes, opening bank accounts, including contracts, and interacting with government bodies. Without a BIN, a branch is not considered to be operating legally, even if the parent company has existed for many years and has an impeccable reputation.

Entering data into the National Register

The final stage of the procedure is entering information about the registered subdivision into the National Register of Business Identification Numbers. This is a unified state database where information is collected on all operating subjects on the territory of Kazakhstan that have a BIN.

Entry into the register has important public significance. Any interested counterparty can use open sources to check whether this subdivision actually exists, when it was registered, who its head is, and whether it is in the process of liquidation. This increases the transparency of business transactions and reduces the risks of fraud.

Legal Status of a Registered Subdivision

After undergoing accounting registration, a branch or representative office acquires official status, but this status has its limitations.

Operating without the status of a legal entity

The law specifically emphasizes: branches and representative offices are subject to accounting registration without the rights of a legal entity. This means they do not become independent participants in civil transactions.

A branch cannot acquire property in its own name, be a plaintiff or defendant in court, or issue powers of attorney in its own name. All transactions concluded by the head of the branch are considered transactions of the parent company. All claims arising from the branch's activities are directed to the parent organization. All assets used by the branch belong to the parent company.

Such a structure creates certain risks for counterparties, as they have to assess the solvency not of the branch itself, but of its parent structure, which may be located in another country. At the same time, this gives advantages to the parent company, allowing it to manage risks and assets centrally.

Scope of authority of a registered subdivision

Despite the lack of legal entity status, a registered branch or representative office has a certain set of powers necessary for its functioning.

- It can open bank accounts in its own name (but disposing of funds is carried out within the limits of the authority granted to the head).

- It can conclude employment contracts with employees, acting as an employer on behalf of the parent company.

- It can obtain licenses and permits for certain types of activities, where provided by law.

- It can have its own seal and company letterheads.

Practical Aspects of Accounting Registration

The moment the obligation arises

The obligation to undergo accounting registration for a branch or representative office arises from the moment activities actually begin on the territory of Kazakhstan. The law does not require preliminary registration before the subdivision starts operating. However, delaying registration is also not allowed — carrying out the functions of a branch or representative office without registration entails administrative liability.

Consequences of non-registration

If a branch or representative office operates without accounting registration, its entire activity is considered illegal. Contracts concluded on behalf of such a subdivision may be declared invalid. The head risks being held administratively liable. Additionally, the tax service may make additional tax assessments based on the assumption that activities were conducted but taxes were not paid.

Difference from registering legal entities

It is important to understand the difference between the accounting registration of a branch and the registration of a subsidiary company (LLP). A subsidiary company is an independent legal entity with its own charter capital, its own balance sheet, and its own responsibility. Its registration is subject to the general rules for creating legal entities. A branch, on the other hand, is simply a separate subdivision, and the procedure for legalizing it is significantly simpler, but its legal status is also narrower.

Conclusion

Accounting registration of branches and representative offices in Kazakhstan is a mandatory administrative procedure that includes checking documents, issuing a BIN, and entering information into the National Register. A registered subdivision is not a legal entity but receives official recognition and the opportunity to operate legally.For a business, this means that when opening a branch or representative office, one cannot limit oneself to internal corporate procedures. It is necessary to follow the path of interaction with the state established by law, gather a properly executed package of documents, and obtain a certificate of accounting registration. Only after this can the subdivision be considered legally operating and begin to perform its functions.

Bodies Carrying Out Accounting Registration of Branches and Representative Offices

The choice of authority depends on the status of the parent organization - whether it is commercial or non-commercial.

Two Streams, Two Systems, Two Registrars

Kazakhstani law draws a strict line between the commercial and non-commercial sectors. This line runs not only through tax rules or reporting requirements but also through the procedures for registering separate subdivisions. Branches and representative offices established by different types of organizations fall under the purview of different state mechanisms.

For the applicant, this means the need to correctly identify themselves. A mistake at this stage leads to loss of time and nerves: documents submitted to the wrong address simply will not be accepted for consideration, and the entire procedure will have to be started over.

Justice Authorities: Registration Hub for the Non-Commercial Sector

Who is specifically authorized to register?

If the parent company belongs to the category of non-commercial organizations, its branches and representative offices undergo accounting registration in the structures of the Ministry of Justice of the Republic of Kazakhstan. Depending on the scale and geography of the subdivision's activities, these may be:

Who falls into the category of non-commercial organizations?

Organizations for which profit-making is not the main purpose of their activities are recognized as non-commercial. Even if profit is generated, it is not distributed among participants but is spent to achieve the statutory goals. This category includes:

State Corporation "Government for Citizens": Universal Registrar for Business

Legal nature and functions of the State Corporation

The State Corporation "Government for Citizens" is a unique institution created to implement the "one-stop shop" principle. In everyday life, it is often simply called PSCs (Public Service Centers). This structure aggregates the functions of many departments, allowing citizens and businesses to receive services in one place without endless visits to offices.

Those opening a branch or representative office on behalf of a commercial organization should apply here.

Which organizations are considered commercial?

Organizations for which profit-making is the main purpose of their activity are considered commercial. The profit received is distributed among the participants (shareholders, founders). This sector includes:

Two Streams, Two Systems, Two Registrars

Kazakhstani law draws a strict line between the commercial and non-commercial sectors. This line runs not only through tax rules or reporting requirements but also through the procedures for registering separate subdivisions. Branches and representative offices established by different types of organizations fall under the purview of different state mechanisms.

For the applicant, this means the need to correctly identify themselves. A mistake at this stage leads to loss of time and nerves: documents submitted to the wrong address simply will not be accepted for consideration, and the entire procedure will have to be started over.

Justice Authorities: Registration Hub for the Non-Commercial Sector

Who is specifically authorized to register?

If the parent company belongs to the category of non-commercial organizations, its branches and representative offices undergo accounting registration in the structures of the Ministry of Justice of the Republic of Kazakhstan. Depending on the scale and geography of the subdivision's activities, these may be:

- the central apparatus - the Registration Service Committee of the Ministry of Justice located in the capital;

- territorial divisions - justice departments of regions, cities of republican significance (Almaty, Shymkent), and the capital.

Who falls into the category of non-commercial organizations?

Organizations for which profit-making is not the main purpose of their activities are recognized as non-commercial. Even if profit is generated, it is not distributed among participants but is spent to achieve the statutory goals. This category includes:

- public associations of various types;

- charitable and other foundations;

- associations and unions uniting legal entities;

- non-commercial joint-stock companies;

- institutions established to carry out social, cultural, educational, or scientific tasks;

- religious structures.

State Corporation "Government for Citizens": Universal Registrar for Business

Legal nature and functions of the State Corporation

The State Corporation "Government for Citizens" is a unique institution created to implement the "one-stop shop" principle. In everyday life, it is often simply called PSCs (Public Service Centers). This structure aggregates the functions of many departments, allowing citizens and businesses to receive services in one place without endless visits to offices.

Those opening a branch or representative office on behalf of a commercial organization should apply here.

Which organizations are considered commercial?

Organizations for which profit-making is the main purpose of their activity are considered commercial. The profit received is distributed among the participants (shareholders, founders). This sector includes:

- limited liability partnerships (LLPs) - the most common form of business;

- open and closed joint-stock companies;

- production cooperatives;

- general and limited partnerships;

- state enterprises operating on a commercial basis;

- any other structures created for conducting entrepreneurial activities.

Accreditation of a Foreign Company Branch in Kazakhstan: A Clear Guide to the Procedure

The process can be divided into five main steps:

Step 1. Preparation of Constituent Documents (the most important stage)

The head office needs to prepare a package of corporate documents:

Step 2. Preparation of Local Documents in Kazakhstan

In parallel with legalization, or after it, it is necessary to resolve "local" issues in Kazakhstan itself:

Step 3. Submitting the Application

The collected package of documents is submitted to the justice authorities (registering body). This can be done either directly or through PSCs, which act as intermediaries.

Step 4. The Finale of the Procedure - Receiving Documents

After verification (usually taking several working days) and payment of the state fee, the branch is officially born:

Change of legal address (actual location).

Making amendments to the constituent documents of the head company.

Change of the name of the head company.In these cases, an application is submitted to make changes to the registration data, but it is not required to go through the entire accreditation procedure again.

Step 1. Preparation of Constituent Documents (the most important stage)

The head office needs to prepare a package of corporate documents:

- The company's charter (or similar constituent document).

- The decision of the company's management to establish a branch in Kazakhstan and to approve the Regulations on it.

- The Regulations on the Branch itself (the local document regulating its work).

- A power of attorney issued in the name of the branch head.

- Be translated into Kazakh and Russian.

- Be notarized at the location of the parent company.

- Be legalized for use abroad (apostille or consular legalization procedure, depending on the country where the parent structure is registered).

Step 2. Preparation of Local Documents in Kazakhstan

In parallel with legalization, or after it, it is necessary to resolve "local" issues in Kazakhstan itself:

- Choose a legal address (conclude a preliminary lease agreement for premises or obtain a guarantee letter from the owner).

- Prepare a copy of the passport of the future branch head.

Step 3. Submitting the Application

The collected package of documents is submitted to the justice authorities (registering body). This can be done either directly or through PSCs, which act as intermediaries.

Step 4. The Finale of the Procedure - Receiving Documents

After verification (usually taking several working days) and payment of the state fee, the branch is officially born:

- A certificate of accreditation is issued.

- A BIN is assigned.

- Registration with the Tax Committee is carried out automatically (or upon separate application).

- Validity period: Accreditation in Kazakhstan is indefinite. It is no longer necessary to redo it every 5 years, as before.

- When to update data: Although accreditation is indefinite, changes must be made to the register in the following cases:

Change of legal address (actual location).

Making amendments to the constituent documents of the head company.

Change of the name of the head company.In these cases, an application is submitted to make changes to the registration data, but it is not required to go through the entire accreditation procedure again.

Document Requirements for a Foreign Founder When Opening a Branch in Kazakhstan

The procedure for registering a non-resident's separate subdivision on the territory of the Republic of Kazakhstan requires submitting a package of official papers confirming the legal capacity of the parent structure. The list of necessary materials and the algorithm for confirming their authenticity are determined by the jurisdiction in which the founder is registered.

Comprehensive List of Documentation

To open a branch or representative office, the following materials originating from the head office must be submitted to the authorized authorities:

2. Confirmation of fiscal status:

3. Internal corporate acts and powers of attorney:

4. Personal data of managing persons:

Variability of Legalization Procedures

Granting legal significance to the above documents on the territory of the Republic of Kazakhstan is carried out according to one of three schemes, depending on whether the founder's country is party to international agreements:

2. Standard regime for countries parties to the Hague Convention of 1961

For firms from states that have signed the Convention abolishing diplomatic legalization, a procedure for affixing a special stamp is provided.

3. Full cycle for other states

Companies from countries not party to the above-mentioned agreements must undergo multi-stage consular legalization.

Translation and Formatting Requirements

All documents originally drafted in languages other than Kazakh or Russian are subject to translation.

Comprehensive List of Documentation

To open a branch or representative office, the following materials originating from the head office must be submitted to the authorized authorities:

- Set of registration and constituent data:

- Official extract obtained from the state register of the country of incorporation (confirms the existence of the legal entity).

- Basic regulatory acts of the company - the charter, memorandum, incorporation agreement, or other documents serving their function.

2. Confirmation of fiscal status:

- Certificate of registration with the tax authority of the state of registration, containing a unique taxpayer identification code (or its national equivalent).

3. Internal corporate acts and powers of attorney:

- Official decision of the competent body of the foreign company to establish a branch (representative office) on Kazakhstani territory. Note: the date of such decision must not exceed 12 months prior to the submission of documents for registration.

- Power of attorney issued in the name of the head of the branch being established, granting them the right to represent the interests of the parent company in the Republic of Kazakhstan.

- Separate power of attorney for the person directly handling the registration process.

4. Personal data of managing persons:

- Notarized copy of the identity document of the director (head) of the parent company.

- Notarized copy of the passport of the candidate for the position of head of the branch in Kazakhstan.

Variability of Legalization Procedures

Granting legal significance to the above documents on the territory of the Republic of Kazakhstan is carried out according to one of three schemes, depending on whether the founder's country is party to international agreements:

- Preferential regime for EAEU entities

- Required action: It is sufficient to notarize the authenticity of the head's signature and the company's seal at the location of the head office.

- Result: Documents are accepted by Kazakhstani registrars in this form without additional formalities.

2. Standard regime for countries parties to the Hague Convention of 1961

For firms from states that have signed the Convention abolishing diplomatic legalization, a procedure for affixing a special stamp is provided.

- Required action: The competent authority of the country of origin of the document (Ministry of Justice, Chamber of Commerce, etc.) affixes an "Apostille" stamp to the document.

- Result: This stamp certifies the authenticity of the signature and the status of the person who issued the document, after which it acquires full legal force in Kazakhstan.

3. Full cycle for other states

Companies from countries not party to the above-mentioned agreements must undergo multi-stage consular legalization.

- Required action: The document is sequentially certified by the justice authorities and the Ministry of Foreign Affairs of the country of origin, and then sent to the diplomatic mission (consulate) of Kazakhstan abroad for final endorsement.

Translation and Formatting Requirements

All documents originally drafted in languages other than Kazakh or Russian are subject to translation.

- Language aspect: The translation must be made into both languages that have official status in the Republic of Kazakhstan - Kazakh (state) and Russian.

- Legal confirmation of translation: The conformity of the translated text to the original must be certified by a notary operating on the territory of Kazakhstan.

- Compliance with validity periods. Some documents (eg, extracts from registers) are valid only for a limited period. This period must not expire by the time of the visit to the registering authority.

- Uniformity of name spelling. The transliteration of the name of the parent organization must be identical in all translations and cover letters. Any discrepancies may be interpreted as false information.

- Consequences of errors. Neglecting legalization rules (lack of an apostille where required) or submitting documents without a notarized translation entails a formal refusal. The entire set is returned to the applicant, and the procedure must be started anew after eliminating the shortcomings.

Appointment of the Head of a Branch or Representative Office

The Institution of the Head of a Separate Subdivision in the Republic of Kazakhstan: Corporate Procedures and Law Enforcement Practice

The Nature of Authority: Not a Position, but a Function

In Kazakhstani legal reality, branches and representative offices occupy a special place. They are not independent subjects of law, but merely territorially separated instruments for implementing the will of the legal entity that created them. Hence the main feature of the status of their heads: the scope of rights and obligations of such a manager is determined not so much by the position held, but by the document delegating to them the authority to act on behalf of the company externally.

When we talk about appointing a branch director, it is important to understand the two-level nature of this process.

The Corporate Basis: How the Decision is Made

The initiation of the appointment of a head of a structural subdivision always originates in the head office. The specific body authorized to make such a decision depends on the company's organizational architecture:

The Power of Attorney as a Key Document

If the corporate decision is the internal will of the company, then the power of attorney is the instrument that brings this will to the outside. Without it, even an officially appointed director cannot sign a single legally significant document.

Essential Details Without Which a Power of Attorney is Invalid

Kazakhstani civil legislation imposes a number of mandatory requirements on powers of attorney. Ignoring even one of them entails the nullity of the document:

What Exactly Can Be Entrusted to the Branch Head

The law does not contain a closed list of actions that the head of a separate subdivision can perform. The scope of authority is the result of an agreement between the parent company and its local representative. However, many years of law enforcement practice have developed an optimal set of rights that it is advisable to include in the power of attorney:

Terms and Limits of Validity

A power of attorney cannot be perpetual. The maximum period for which Kazakhstani legislation allows issuing powers of attorney is three years. If the term is not specified in the text of the document, a dispositive norm applies — the power of attorney will be valid for one year from the date of its signing.

It is important to remember that a power of attorney terminates not only upon expiration of its term. It can be revoked at any time by the parent company. The liquidation of the branch itself or the refusal of the head from the granted powers also serve as grounds for termination.

The Institution of Sub-delegation: When Further Delegation is Possible

The branch head is obliged to personally perform the actions for which they are authorized. However, life makes adjustments - business trips, illness, vacation. The law provides for the possibility of sub-delegation: the head can transfer part of their powers to another person (eg, a deputy), but only if such a right is explicitly stated in the original power of attorney.

There is an important procedural rule here: a power of attorney issued by way of sub-delegation must be certified by a notary. The notary checks whether the term of the new power of attorney does not exceed the term of the main one, and whether the sub-delegation expands the scope of authority initially granted to the head.

Specifics of Appointing the Head of a Branch of a Foreign Company

For non-residents opening their structures in Kazakhstan, the procedure for appointing a head acquires an additional dimension — legalization of documents confirming their status.

At the stage of registering the branch with the Ministry of Justice, two key documents related to the head must be submitted:

Both documents must undergo a legalization procedure, the type of which depends on the investor's country of origin.

If the head office is registered in a member state of the Eurasian Economic Union, simple notarization of signatures is sufficient. An apostille or consular certification is not required. For companies from countries that have signed the Hague Convention of 1961, affixing an apostille stamp by the competent authority of the country of origin is mandatory. For residents of other states, full consular legalization is required, including certification by the Ministry of Foreign Affairs of the country of origin and subsequent endorsement at the consulate of Kazakhstan abroad.

Furthermore, all documents drawn up in a foreign language must be translated into Kazakh and Russian. The accuracy of the translation is certified by a notary operating on the territory of the Republic of Kazakhstan.

Responsibility and Risks of Exceeding Authority

In practice, situations often arise where the branch head exceeds the limits of the granted rights. For example, concluding a lease agreement for an amount exceeding the limit set in the power of attorney, or selling property without the sanction of the head office.

In such cases, the mechanism established in Article 167 of the Civil Code applies. A transaction made by a representative exceeding their authority is considered to be made on behalf of the representative themselves. This means that the parent company is not obliged to fulfill it. Moreover, it can apply to the court to declare such a transaction invalid.

For the head themselves, exceeding authority entails financial liability. If their actions caused losses to the company (for example, had to pay a penalty to a counterparty under a disputed transaction), these losses can be recovered from them in court.

Summing up the analysis, several key recommendations can be formulated:

The Nature of Authority: Not a Position, but a Function

In Kazakhstani legal reality, branches and representative offices occupy a special place. They are not independent subjects of law, but merely territorially separated instruments for implementing the will of the legal entity that created them. Hence the main feature of the status of their heads: the scope of rights and obligations of such a manager is determined not so much by the position held, but by the document delegating to them the authority to act on behalf of the company externally.

When we talk about appointing a branch director, it is important to understand the two-level nature of this process.

- The first level is intra-corporate, where the personnel decision is made.

- The second level is external, where the head legitimizes themselves before counterparties and the state.

The Corporate Basis: How the Decision is Made

The initiation of the appointment of a head of a structural subdivision always originates in the head office. The specific body authorized to make such a decision depends on the company's organizational architecture:

- In limited liability partnerships (companies, LTD, LLP, Limited - the most common form in different countries), this is the prerogative of the general meeting of participants or the sole participant, if the business belongs to one person.

- In joint-stock companies, personnel issues of this level are often delegated to the board of directors, unless the charter assigns them to the exclusive competence of the general meeting.

The Power of Attorney as a Key Document

If the corporate decision is the internal will of the company, then the power of attorney is the instrument that brings this will to the outside. Without it, even an officially appointed director cannot sign a single legally significant document.

Essential Details Without Which a Power of Attorney is Invalid

Kazakhstani civil legislation imposes a number of mandatory requirements on powers of attorney. Ignoring even one of them entails the nullity of the document:

- Date of issue. This is an absolute requirement of paragraph 2 of Article 168 of the Civil Code. If the power of attorney does not specify when it was issued, it does not create any legal consequences. The term begins to run from this date.

- Signature of the head. The document is signed by the first person of the company or another employee whom the constituent documents have granted such a right.

- Seal. The requirement for a seal is not universal today. For most commercial structures, the seal has become an optional attribute. However, in practice, many companies retain it in circulation, and if the power of attorney is affixed with a seal, it increases trust from banks and large counterparties.

- Signature of the chief accountant. This requisite appears only in one case — if the power of attorney grants authority to receive or issue inventory items and funds. This requirement comes from accounting rules and is aimed at ensuring double control over the movement of assets.

What Exactly Can Be Entrusted to the Branch Head

The law does not contain a closed list of actions that the head of a separate subdivision can perform. The scope of authority is the result of an agreement between the parent company and its local representative. However, many years of law enforcement practice have developed an optimal set of rights that it is advisable to include in the power of attorney:

- Firstly, these are managerial functions within the subdivision itself: issuing orders on personnel, approving work schedules, organizing document flow. Without this, it is impossible to ensure current activities.

- Secondly, these are external representative functions. The branch head must have the right to sign contracts with counterparties. Here, the parent company should consider limits. You can grant the right to conclude any transactions without restrictions (general power of attorney), or you can set a threshold — for example, up to ten thousand monthly calculation indicators. Anything above that should require additional approval from the head office.

- Thirdly, these are financial powers. Opening settlement accounts, managing funds, signing payment documents - these are critically important functions that are usually clearly specified.

- Fourthly, this is court representation. The branch head must have the right to file lawsuits, sign responses, appeal decisions, and participate in enforcement proceedings on behalf of the company.

- Fifthly, this is interaction with state bodies - the tax service, the antimonopoly authority, statistics. The branch head usually signs the reports submitted at the location of the subdivision.

Terms and Limits of Validity

A power of attorney cannot be perpetual. The maximum period for which Kazakhstani legislation allows issuing powers of attorney is three years. If the term is not specified in the text of the document, a dispositive norm applies — the power of attorney will be valid for one year from the date of its signing.

It is important to remember that a power of attorney terminates not only upon expiration of its term. It can be revoked at any time by the parent company. The liquidation of the branch itself or the refusal of the head from the granted powers also serve as grounds for termination.

The Institution of Sub-delegation: When Further Delegation is Possible

The branch head is obliged to personally perform the actions for which they are authorized. However, life makes adjustments - business trips, illness, vacation. The law provides for the possibility of sub-delegation: the head can transfer part of their powers to another person (eg, a deputy), but only if such a right is explicitly stated in the original power of attorney.

There is an important procedural rule here: a power of attorney issued by way of sub-delegation must be certified by a notary. The notary checks whether the term of the new power of attorney does not exceed the term of the main one, and whether the sub-delegation expands the scope of authority initially granted to the head.

Specifics of Appointing the Head of a Branch of a Foreign Company

For non-residents opening their structures in Kazakhstan, the procedure for appointing a head acquires an additional dimension — legalization of documents confirming their status.

At the stage of registering the branch with the Ministry of Justice, two key documents related to the head must be submitted:

- Decision of the competent body of the foreign company to establish the branch and appoint the manager.

- Power of attorney in the name of this head.

Both documents must undergo a legalization procedure, the type of which depends on the investor's country of origin.

If the head office is registered in a member state of the Eurasian Economic Union, simple notarization of signatures is sufficient. An apostille or consular certification is not required. For companies from countries that have signed the Hague Convention of 1961, affixing an apostille stamp by the competent authority of the country of origin is mandatory. For residents of other states, full consular legalization is required, including certification by the Ministry of Foreign Affairs of the country of origin and subsequent endorsement at the consulate of Kazakhstan abroad.

Furthermore, all documents drawn up in a foreign language must be translated into Kazakh and Russian. The accuracy of the translation is certified by a notary operating on the territory of the Republic of Kazakhstan.

Responsibility and Risks of Exceeding Authority

In practice, situations often arise where the branch head exceeds the limits of the granted rights. For example, concluding a lease agreement for an amount exceeding the limit set in the power of attorney, or selling property without the sanction of the head office.

In such cases, the mechanism established in Article 167 of the Civil Code applies. A transaction made by a representative exceeding their authority is considered to be made on behalf of the representative themselves. This means that the parent company is not obliged to fulfill it. Moreover, it can apply to the court to declare such a transaction invalid.

For the head themselves, exceeding authority entails financial liability. If their actions caused losses to the company (for example, had to pay a penalty to a counterparty under a disputed transaction), these losses can be recovered from them in court.

Summing up the analysis, several key recommendations can be formulated:

- Firstly, always formalize the appointment of a branch head with two separate acts: an internal decision of the authorized body and an external power of attorney. Substituting one document for the other creates risks when interacting with counterparties.

- Secondly, detail the powers in the power of attorney as much as possible. The more specific the rights and limitations are spelled out, the less room there is for abuse and corporate conflicts. Avoid general phrases like "perform all necessary actions" — they create an illusion of complete authority, but in practice give rise to disputes over interpretation.

- Thirdly, for foreign companies, it is critically important to comply with the legalization requirements precisely at the stage of branch registration. Errors related to the absence of an apostille or incorrect translation can only be corrected by re-submitting the documents, which entails a loss of time.

- Fourthly, monitor the validity periods of powers of attorney. Implement an accounting system that automatically reminds you of the expiration of the head's authority one month before the end. This will avoid situations where the branch is left without a legal representative at the most inopportune moment.

Taxation of a Branch of a Foreign Company in Kazakhstan from 2026

From January 1, 2026, a new version of the Tax Code is in effect in Kazakhstan, which fundamentally changes approaches to calculating Corporate Income Tax (CIT). The changes affect not only rates, but also the procedure for calculating advance payments, rules for recognizing expenses, and even accounting for asset disposal.

For branches of foreign companies that are recognized as permanent establishments and are independent taxpayers, these innovations are particularly significant. This article examines how the new rules apply specifically to branches, what to pay attention to, and how to avoid tax risks.

Status of a Branch in Tax Relations

Branch as a Permanent Establishment

According to subparagraph 57 of Article 1 of the Tax Code of the Republic of Kazakhstan, structural subdivisions of legal entities (including branches) are recognized as taxpayers. This means that a branch of a foreign company:

Branch Income: What is Subject to CIT

Branches of foreign companies pay CIT on taxable income received from activities in Kazakhstan. Income includes all receipts from the parent company for the maintenance of the branch - rent, salaries, operating expenses. The Tax Code does not differentiate between commercial revenue and financing from the head office: both are recognized as income of the branch.

Simultaneously, the branch has the right to deduct expenses related to obtaining this income, provided they are documented and comply with the requirements of the Code.

CIT Rates in 2026

Basic Rate of 20% for Most Branches

For branches whose activities do not fall under special categories, the basic rate of 20% applies (subparagraph 5, paragraph 2, Article 357 of the Tax Code of the Republic of Kazakhstan). This applies to most representative offices of foreign companies operating in trade, services, production, and other industries.

Special Rates for Specific Types of Activities

If the branch carries out activities subject to preferential or increased rates, the following rules apply:

Important: Preferential rates apply only on condition that the income is received precisely from the specified types of activities, and the taxpayer can document this.

Taxation of Net Income upon Profit Repatriation

Special attention should be paid to the norm of subparagraph 4, paragraph 1 of Article 357 of the Tax Code of the Republic of Kazakhstan: the net income of a non-resident legal entity carrying out activities through a permanent establishment is subject to CIT at a rate of 15%. This is a tax on profit transferred to the parent company outside Kazakhstan.

Thus, the taxation of a branch has a two-level structure:

Advance Payments for CIT: New Procedure

How Advances Are Now Calculated

Since 2026, the algorithm for calculating advance payments has been changed:

Who is Exempt from Advances

Taxpayers whose total annual income, considering adjustments for the period preceding the previous one, does not exceed 600,000 MCI (the previous threshold was 325,000 MCI) are exempt from paying advance payments.

Important Exception: Companies engaged in activities related to digital assets are obliged to pay advances regardless of the amount of income.

Branches of foreign companies, like residents, apply these rules on a general basis. When determining the threshold, the income of the branch itself is considered, not that of the parent company.

Expenses: What Cannot Be Taken into Account When Calculating Tax

The Main Limitation: Transactions with "Simplified" Taxpayers

From 2026, expenses for the purchase of goods, works, or services from persons applying the special tax regime based on a simplified declaration are included in the list of costs not subject to deduction (subparagraph 16, paragraph 1, Article 286 of the Tax Code of the Republic of Kazakhstan).

What does this mean for the branch:

If a branch on the general established regime purchases goods or services from an Sole Proprietor or LLP on the "simplified" regime, it cannot reduce its taxable income by the cost of these purchases. The determining date is the date of receipt of goods (according to transfer documents) or the date of signing the certificate of completed work/services.

Recommendation: Review your supplier portfolio. If a critically important counterparty operates under the special tax regime, assess the possibility of them switching to the general regime or factor the loss of the deduction into the transaction price.

What Has Been Excluded from the List of Non-Deductible Items

A number of restrictions that were previously in effect have been removed:

General Principle: Connection with Income

All expenses claimed for deduction must be directly related to activities aimed at generating income and must be documented. Expenses that do not meet these criteria are not accepted.

Disposal of Assets: New Logic for Calculating Income and Losses

Previously, the result from the sale or other disposal of an asset was calculated for each object separately. Since 2026, an aggregate method for entire groups of assets has been introduced.

For branches owning fixed assets in Kazakhstan, these changes require restructuring of analytical accounting.

New Opportunities to Reduce Taxable Income

Controlled Foreign Companies (CFCs)

Although CFC rules are aimed at residents controlling foreign structures, it is important for branches to understand the context: if a foreign company has a branch in Kazakhstan recognized as a permanent establishment, and at the same time is itself controlled by a Kazakhstani resident, complex cross-border situations may arise.

Since 2026, the threshold amount of CFC income allowing them not to be recognized as controlled (in the absence of registration in offshore zones) has been reduced from 150,495 MCI to 195 MCI. This means that even small foreign structures fall under the scope of the rules.

Insurance Companies: Detailed Accounting

For branches that are insurance or reinsurance organizations, detailed lists of income and expenses recognized for CIT purposes have been introduced. Accounting is maintained according to IFRS data. Companies in this sector need to adapt their accounting policies.

What Has Been Canceled: Benefits That No Longer Exist

The following types of reduction of taxable income have been excluded from the Tax Code:

International Agreements on Avoidance of Double Taxation

Branches of foreign companies have the right to apply the provisions of international treaties on the avoidance of double taxation, if such treaties are concluded between Kazakhstan and the country of the parent company (Articles 666–674 of the Tax Code of the Republic of Kazakhstan).To apply the benefits, it is necessary to confirm the status of a tax resident (obtain a residency certificate) and provide it to the tax authority of Kazakhstan with a notarized translation.

For branches of foreign companies that are recognized as permanent establishments and are independent taxpayers, these innovations are particularly significant. This article examines how the new rules apply specifically to branches, what to pay attention to, and how to avoid tax risks.

Status of a Branch in Tax Relations

Branch as a Permanent Establishment

According to subparagraph 57 of Article 1 of the Tax Code of the Republic of Kazakhstan, structural subdivisions of legal entities (including branches) are recognized as taxpayers. This means that a branch of a foreign company:

- independently calculates and pays taxes;

- submits tax reports;

- acts as a tax agent for income paid to individuals and non-residents.

Branch Income: What is Subject to CIT

Branches of foreign companies pay CIT on taxable income received from activities in Kazakhstan. Income includes all receipts from the parent company for the maintenance of the branch - rent, salaries, operating expenses. The Tax Code does not differentiate between commercial revenue and financing from the head office: both are recognized as income of the branch.

Simultaneously, the branch has the right to deduct expenses related to obtaining this income, provided they are documented and comply with the requirements of the Code.

CIT Rates in 2026

Basic Rate of 20% for Most Branches

For branches whose activities do not fall under special categories, the basic rate of 20% applies (subparagraph 5, paragraph 2, Article 357 of the Tax Code of the Republic of Kazakhstan). This applies to most representative offices of foreign companies operating in trade, services, production, and other industries.

Special Rates for Specific Types of Activities

If the branch carries out activities subject to preferential or increased rates, the following rules apply:

Type of Activity | CIT Rate |

|---|---|

| Agriculture, aquaculture (production, processing, sale of own products) | 3% |

| Agricultural cooperatives (except producers) | 6% |

| Activities in the social sphere (education, medicine, culture) — for commercial organizations | 5% in 2026, 10% from 2027 |

| Banking activities (except business lending) | 25% |

| Gambling business (casinos, gaming machine halls, betting shops) | 25% |

Taxation of Net Income upon Profit Repatriation

Special attention should be paid to the norm of subparagraph 4, paragraph 1 of Article 357 of the Tax Code of the Republic of Kazakhstan: the net income of a non-resident legal entity carrying out activities through a permanent establishment is subject to CIT at a rate of 15%. This is a tax on profit transferred to the parent company outside Kazakhstan.

Thus, the taxation of a branch has a two-level structure:

- CIT at a rate of 20% on taxable income (income minus deductions).

- Withholding tax at a rate of 15% on net income upon its repatriation.

Advance Payments for CIT: New Procedure

How Advances Are Now Calculated

Since 2026, the algorithm for calculating advance payments has been changed:

- Advance payments for the first quarter are calculated by the tax authority. The amount of the monthly payment = 1/12 of the total amount of advances calculated in the calculations for the previous tax period. They must be paid by January 25, February 25, and March 25.

- Advance payments after filing the declaration (for the second to fourth quarters) = 1/12 of the amount of CIT actually calculated for the previous year.

Who is Exempt from Advances

Taxpayers whose total annual income, considering adjustments for the period preceding the previous one, does not exceed 600,000 MCI (the previous threshold was 325,000 MCI) are exempt from paying advance payments.

Important Exception: Companies engaged in activities related to digital assets are obliged to pay advances regardless of the amount of income.

Branches of foreign companies, like residents, apply these rules on a general basis. When determining the threshold, the income of the branch itself is considered, not that of the parent company.

Expenses: What Cannot Be Taken into Account When Calculating Tax

The Main Limitation: Transactions with "Simplified" Taxpayers

From 2026, expenses for the purchase of goods, works, or services from persons applying the special tax regime based on a simplified declaration are included in the list of costs not subject to deduction (subparagraph 16, paragraph 1, Article 286 of the Tax Code of the Republic of Kazakhstan).

What does this mean for the branch:

If a branch on the general established regime purchases goods or services from an Sole Proprietor or LLP on the "simplified" regime, it cannot reduce its taxable income by the cost of these purchases. The determining date is the date of receipt of goods (according to transfer documents) or the date of signing the certificate of completed work/services.

Recommendation: Review your supplier portfolio. If a critically important counterparty operates under the special tax regime, assess the possibility of them switching to the general regime or factor the loss of the deduction into the transaction price.

What Has Been Excluded from the List of Non-Deductible Items

A number of restrictions that were previously in effect have been removed:

- Costs for the acquisition, construction, and installation of social facilities can now be deducted in the general procedure.

- Expenses for services of non-residents from low-tax jurisdictions (related parties) can be deducted within 3% of taxable income (previously not deductible at all).

General Principle: Connection with Income

All expenses claimed for deduction must be directly related to activities aimed at generating income and must be documented. Expenses that do not meet these criteria are not accepted.

Disposal of Assets: New Logic for Calculating Income and Losses

Previously, the result from the sale or other disposal of an asset was calculated for each object separately. Since 2026, an aggregate method for entire groups of assets has been introduced.

- For real estate (Group I)

- For shares and securities

- For privileged securities (eg, government securities), the result is calculated separately.

- For non-depreciable assets

For branches owning fixed assets in Kazakhstan, these changes require restructuring of analytical accounting.

New Opportunities to Reduce Taxable Income

- R&D: Double Deduction

- Endowment Funds: New Basis for Income Reduction

- Organizations of Persons with Disabilities: New Rules

- average annual number of employees with disabilities - at least 51%;

- expenses for their remuneration - at least 51% of total labor costs;

- employees must not be listed in other organizations of persons with disabilities.

Controlled Foreign Companies (CFCs)

Although CFC rules are aimed at residents controlling foreign structures, it is important for branches to understand the context: if a foreign company has a branch in Kazakhstan recognized as a permanent establishment, and at the same time is itself controlled by a Kazakhstani resident, complex cross-border situations may arise.

Since 2026, the threshold amount of CFC income allowing them not to be recognized as controlled (in the absence of registration in offshore zones) has been reduced from 150,495 MCI to 195 MCI. This means that even small foreign structures fall under the scope of the rules.

Insurance Companies: Detailed Accounting

For branches that are insurance or reinsurance organizations, detailed lists of income and expenses recognized for CIT purposes have been introduced. Accounting is maintained according to IFRS data. Companies in this sector need to adapt their accounting policies.

What Has Been Canceled: Benefits That No Longer Exist

The following types of reduction of taxable income have been excluded from the Tax Code:

- the amount of excess of expenses over income when operating social facilities;

- the cost of gratuitously transferred property to autonomous educational organizations;

- for small business entities in the manufacturing industry - expenses for the acquisition of industrial buildings.

- remuneration on leasing and on government securities — now tax can only be reduced by 50% of the amount (previously it was 100%).

International Agreements on Avoidance of Double Taxation

Branches of foreign companies have the right to apply the provisions of international treaties on the avoidance of double taxation, if such treaties are concluded between Kazakhstan and the country of the parent company (Articles 666–674 of the Tax Code of the Republic of Kazakhstan).To apply the benefits, it is necessary to confirm the status of a tax resident (obtain a residency certificate) and provide it to the tax authority of Kazakhstan with a notarized translation.

Net Income of a Branch in Kazakhstan: What It Is and How to Calculate It Correctly

For foreign companies operating in Kazakhstan through a branch, the tax system has its own specifics. The main feature is the presence of two-level taxation of profit. While the concept of Corporate Income Tax (CIT) at a rate of 20% is more or less clear, the concept of tax on net income often raises questions.

What is the net income of a branch (permanent establishment)?

According to Article 652 of the Tax Code of the Republic of Kazakhstan, net income is the income of a non-resident legal entity from activities in Kazakhstan through a permanent establishment (branch) that remains after the payment of corporate income tax.

In simple terms: it is the profit that the branch earned in Kazakhstan, on which it has already paid CIT, and which the parent company (non-resident) can theoretically withdraw from the country.

It is on this amount that the state withholds the so-called "tax on net income" (or tax on the profit of a permanent establishment) at a rate of 15% (or 5% if a benefit under the Convention applies, eg, with the PRC).

How a Branch Pays Taxes: A Two-Tier System

To better understand the nature of net income, imagine the tax path of a branch as a staircase with two steps:

1.First step (CIT): The branch receives income, deducts expenses, and arrives at taxable income. CIT is paid on this at a rate of 20%.

2.Second step (Tax on Net Income): CIT is again subtracted from the remaining amount, and the resulting figure is called net income. Tax is paid on this at a rate of 15%.

Example: A branch earned 1,000,000 tenge of net profit (taxable income). It pays 200,000 tenge CIT (20%). 800,000 tenge remains. But the tax authorities see it differently: the tax on net income is levied on the amount remaining after deducting CIT from the taxable income.

What Constitutes a Branch's Income?

To determine taxable income (the first step towards calculating net income), one must understand what the branch needs to include in its reporting.

The aggregate annual income of a branch includes:

1.Income from Kazakhstani sources: sale of goods, works, services on the territory of the Republic of Kazakhstan.

2.Income from foreign sources: if received through the activities of the permanent establishment.

3.Income from gratuitously received property: for example, if the parent company transfers equipment to the branch free of charge, this is also recognized as branch income.

What Can Be Deducted? (Branch Expenses)

When determining taxable income, the branch has the right to deduct expenses related to generating income. This is a general principle: expenses must be documented and aimed at generating profit.

However, for branches, there is an important limitation. According to paragraph 6 of Article 198 of the Tax Code, the following cannot be deducted:

Step-by-Step Calculation of Net Income

To calculate the tax on net income, a strict formula prescribed in Article 652 of the Tax Code is used.

Let's break it down with numbers.

Formula: Net Income = (Taxable Income – Adjustments – Losses Carried Forward) – (CIT calculated on this amount)

Where:

Calculation Example :

Net Income Calculation:

Net Income = 18,000,000 – 3,600,000 = 14,400,000 tenge

It is on this amount (14.4 million tenge) that the branch must pay the tax on net income.

Tax on Net Income Rates

Payment Deadlines and Reporting

The calculation and payment of the tax on net income are inextricably linked to the CIT declaration.

Summary

The net income of a branch is not simply "profit in the account." It is a strictly calculated tax indicator. To determine it, you need to:

1.Calculate the taxable income (Aggregate Annual Income minus allowed deductions).

2.Account for losses carried forward.

3.Subtract the calculated CIT at a rate of 20% from the resulting amount.