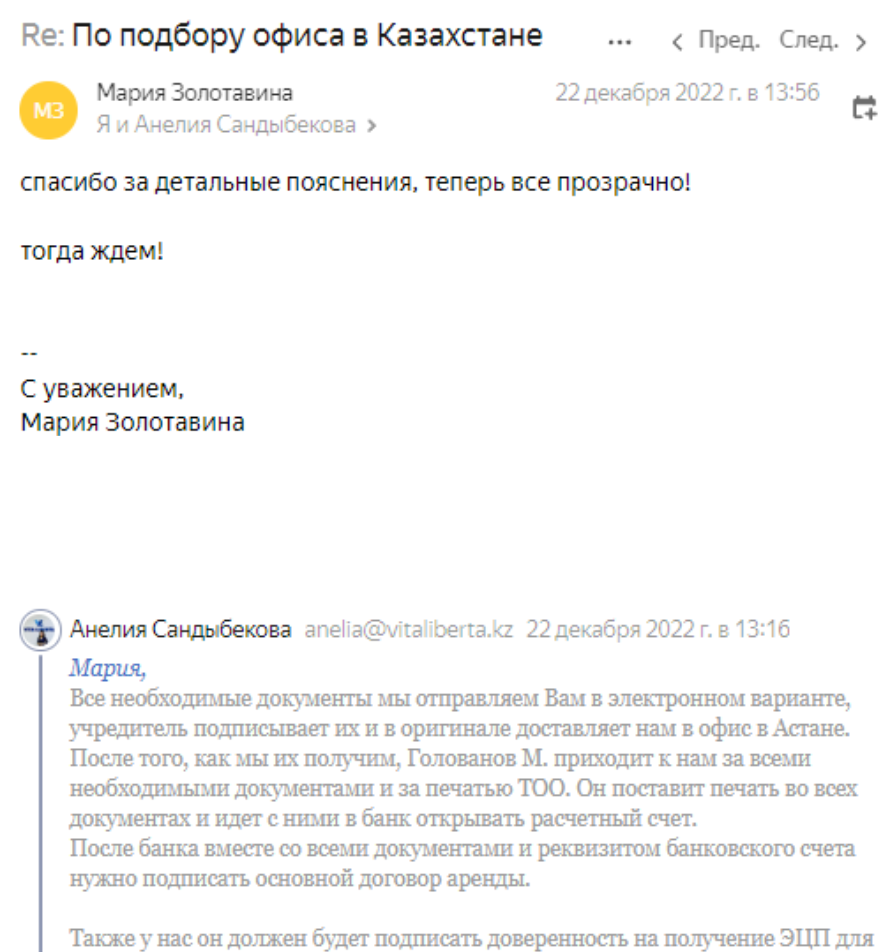

Education

Professional registration of an LLP in Kazakhstan for non-residents — with a guaranteed bank account opening and full compliance with migration legislation!

Get a free consultation from a qualified accountant! Learn how to choose the optimal tax regime for your business and how to legally optimize your tax payments. We will thoroughly analyze your situation and provide a comparative report so you can make an informed and effective decision.

Professional LLP Registration and Support – We Are Always in Touch

We value teamwork and achieve the highest results by applying an individual approach to each client

Madina

Head of the Legal Department, expert in LLP registration and business support

Aneliya

The chief lawyer is a professional with deep knowledge of Kazakhstani legislation

Education

M. S. Narikbaev KAZGUU University, Master of Laws

Aniya

A lawyer is your reliable assistant in matters of business registration and management

Education

M. S. Narikbaev KAZGUU University, Master of Laws

A Satisfied Client's Testimonial

Congratulations from Our Partner Bank

International Women's Day, March 7, 2025

International Women's Day, March 6, 2026

Legal Department Management

Accounting and Legal

Choose a registration package

"Business Start" Package

36 500 ₽

Full LLP registration — for those who already have a lease agreement, personal EDS, and a "Business Migrant" temporary residence permit.

Verification of documents for LLP registration

Consulting on the choice of tax regime for your LLP

Verification of the name during LLP registration

Preparation of the sole founder's decision / minutes of the general meeting on the establishment of the LLP

Selection of a standard charter and foundation agreement for the LLP

Selection of General Classifier of Economic Activities (OKED) codes for the LLP

Registration of the director on the egov.kz portal

Registration of the LLP director in the "Mobile Citizens" database

Determination of the business entity category for the LLP

Consulting on the amount of the authorized capital for the LLP

Completion and submission of the application for state registration of the LLP

Preparation of the order appointing the director of the LLP

"Business Start+" Package

79 900 ₽

From the registration address, individual identification number, and EDS — through submission of the application for a "Business Migrant" temporary residence permit — to full LLP registration.

Verification of documents for LLP registration

Consulting on the choice of tax regime for your LLP

Verification of the name during LLP registration

Preparation of the sole founder's decision / minutes of the general meeting on the establishment of the LLP

Selection of a standard charter and foundation agreement for the LLP

Selection of General Classifier of Economic Activities (OKED) codes for the LLP

Registration of the director on the egov.kz portal

Registration of the LLP director in the "Mobile Citizens" database

Determination of the business entity category for the LLP

Consulting on the amount of the authorized capital for the LLP

Completion and submission of the application for state registration of the LLP

Preparation of the order appointing the director of the LLP

Assistance at the Public Service Center for obtaining an individual identification number

Assistance in obtaining an EDS: at the Public Service Center or through the Consulate

Preparation for submission of application for a temporary residence permit under the "Business Migrant" basis

Selection of suitable office space or legal address

Verification of the lessor's rights to the premises

Negotiation of the preliminary lease agreement for signing by the founder (director)

Arrangement for reissuance of the main lease agreement to the LLP (after registration)

Approval, production, and delivery of the LLP seal

Assistance in obtaining an EDS for the head of the LLP

Submission of the application for a special tax regime based on a simplified declaration

"Business Standard" Package

114 900 ₽

After registration — a complete start: opening of the LLP account and director's account, setup of 1С, integration with the IS ESF, and accounting support from day one.

Verification of documents for LLP registration

Consulting on the choice of tax regime for your LLP

Verification of the name during LLP registration

Preparation of the sole founder's decision / minutes of the general meeting on the establishment of the LLP

Selection of a standard charter and foundation agreement for the LLP

Selection of General Classifier of Economic Activities (OKED) codes for the LLP

Registration of the director on the egov.kz portal

Registration of the LLP director in the "Mobile Citizens" database

Determination of the business entity category for the LLP

Consulting on the amount of the authorized capital for the LLP

Completion and submission of the application for state registration of the LLP

Preparation of the order appointing the director of the LLP

Assistance at the Public Service Center for obtaining an individual identification number

Assistance in obtaining an EDS: at the Public Service Center or through the Consulate

Preparation for submission of application for a temporary residence permit under the "Business Migrant" basis

Selection of suitable office space or legal address

Verification of the lessor's rights to the premises

Negotiation of the preliminary lease agreement for signing by the founder (director)

Arrangement for reissuance of the main lease agreement to the LLP (after registration)

Approval, production, and delivery of the LLP seal

Assistance in obtaining an EDS for the head of the LLP

Submission of the application for a special tax regime based on a simplified declaration

Registration of a new Legal Entity user on the "e-government" portal

Preparation of an employment contract and job description for the director

Registration of the employment contract on the Enbek.kz electronic labor exchange

Assistance in verifying the phone number of the LLP director

Legal support for opening a current account for the LLP at a bank of your choice

Legal support for opening a personal account and bank card for the LLP director

Consulting on VAT and registration for VAT (if necessary)

Registration on the State Portal of the EI IS (Electronic Invoice Information System)

Creation of a database for your LLP in "1С:Accounting"

The Moment When Paying Taxes Brings Joy

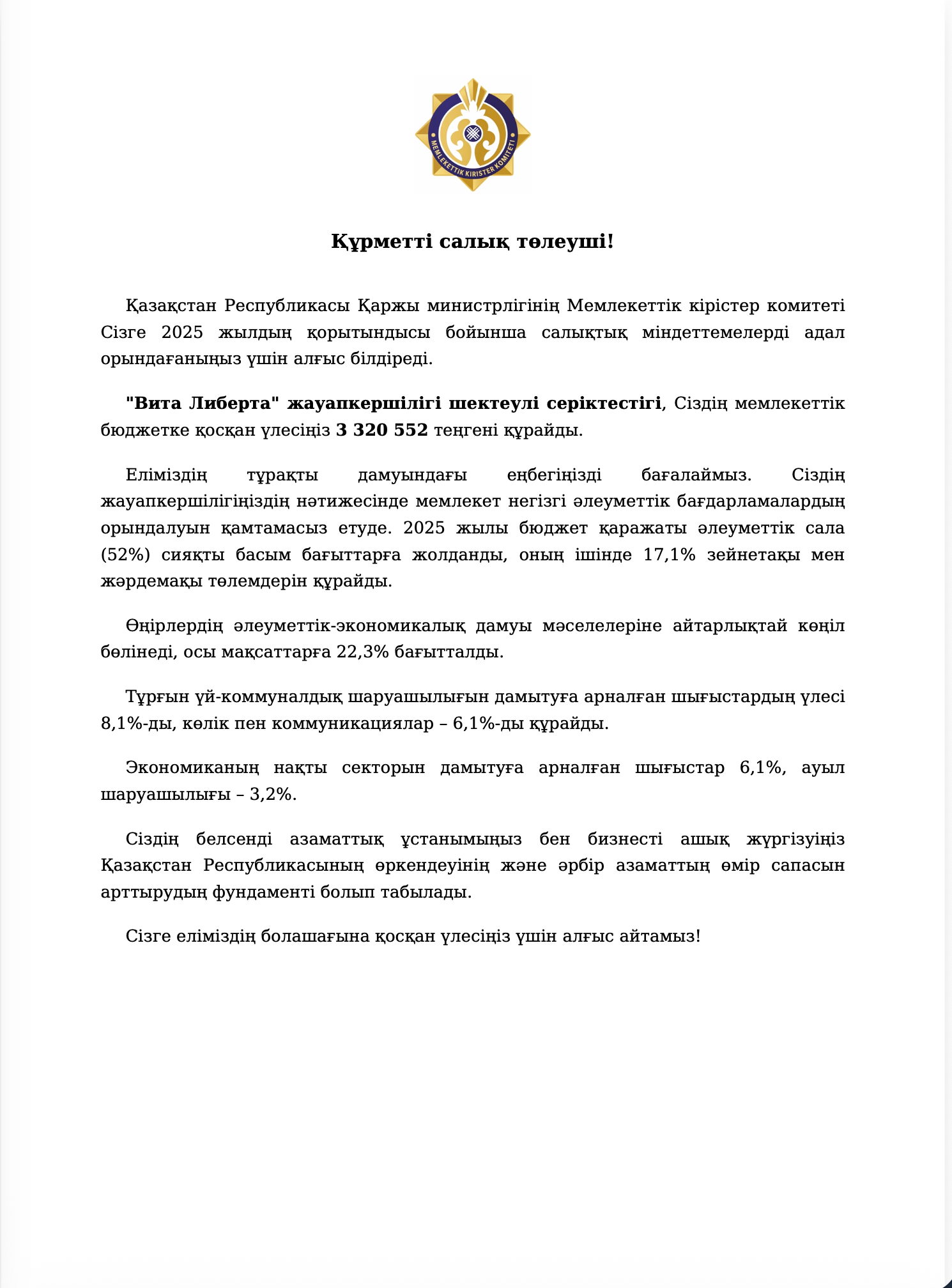

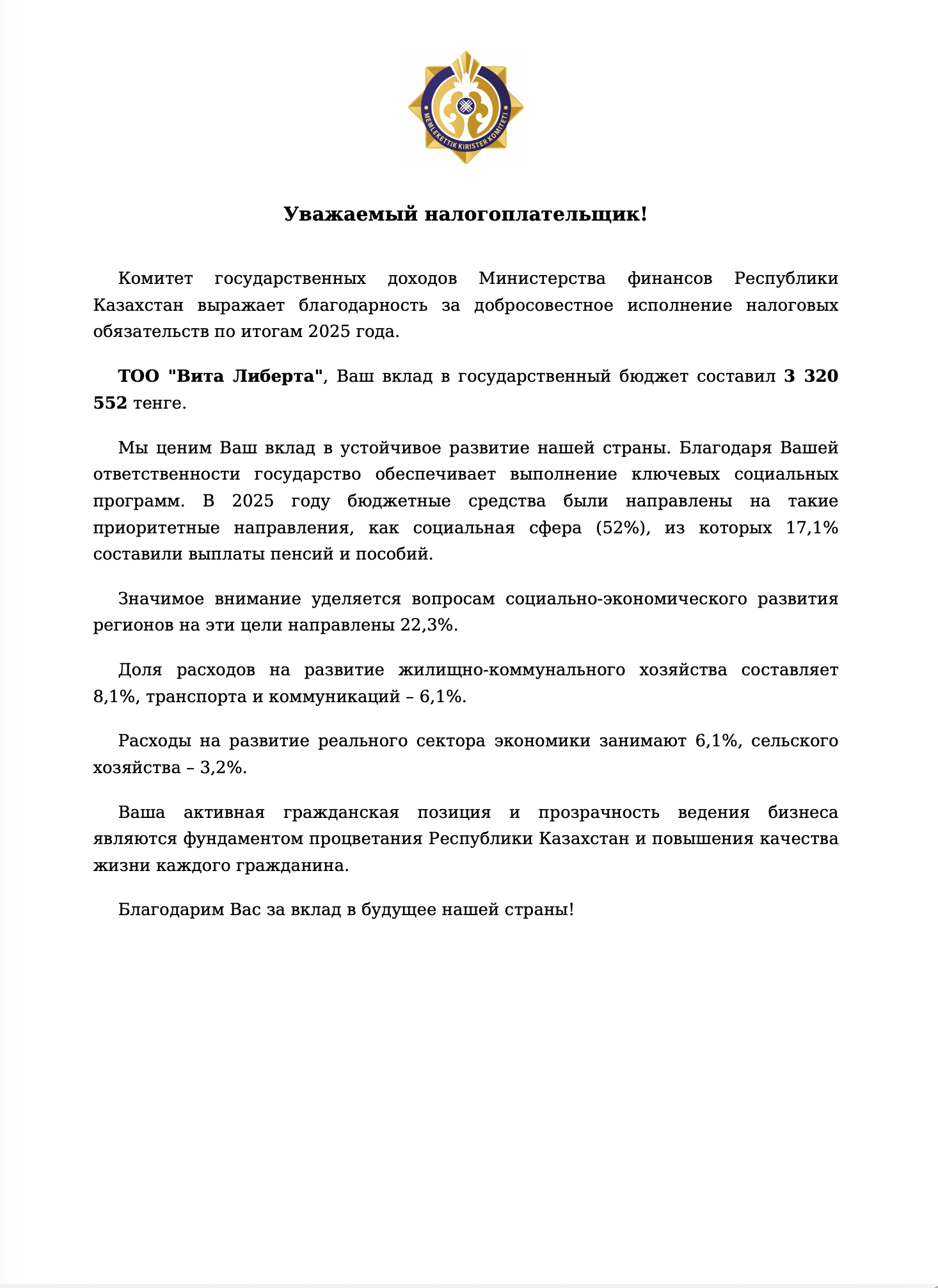

Usually, the words "taxes," "State Revenue Committee," and "payment" give an entrepreneur a slight headache. But this document is one of those rare exceptions. When you see it, you want to take a screenshot and send it to the chat with the caption: "Just something pleasant!"

The 3,320,552 tenge our company paid to the budget for 2025 is not just a number.

This is 52% going to the social sector. This is pensions and benefits.

This is 22% going to the regions, 8% to housing and communal services, 6% to roads and communications.

Even 3% goes to agriculture — perhaps somewhere a new tractor is being purchased or a water pipe is being repaired.

Of course, we understand: taxes are not charity, it's an obligation.

But when you see the fruit of your labor become someone's paycheck, someone's asphalt, someone's home, you feel a sense of pride.

Thank you for your attention! It's gratifying to be among those who don't hide but contribute to the common cause.

The 3,320,552 tenge our company paid to the budget for 2025 is not just a number.

This is 52% going to the social sector. This is pensions and benefits.

This is 22% going to the regions, 8% to housing and communal services, 6% to roads and communications.

Even 3% goes to agriculture — perhaps somewhere a new tractor is being purchased or a water pipe is being repaired.

Of course, we understand: taxes are not charity, it's an obligation.

But when you see the fruit of your labor become someone's paycheck, someone's asphalt, someone's home, you feel a sense of pride.

Thank you for your attention! It's gratifying to be among those who don't hide but contribute to the common cause.

Professional Liability Insurance

Our professional liability is insured by JSC IC "NOMAD Insurance"

(Contract No. 207-25-14142055/811884DS).

Insurance coverage includes:

The insurance applies during the provision of professional services requiring special knowledge and qualifications.

(Contract No. 207-25-14142055/811884DS).

Insurance coverage includes:

- Compensation for harm caused to life and/or health

- Compensation for damage caused to the property of third parties

The insurance applies during the provision of professional services requiring special knowledge and qualifications.

Insurance Policy

Advantages of Doing Business in Kazakhstan

Stages of Company Registration in Kazakhstan (for Non-Residents)

1. Migration Permission for Opening an LLP

Migration Requirements for Foreign Founders

Frequently asked questions when a foreign citizen registers an LLP in Kazakhstan: is a visa required, is a temporary residence permit needed, and how to legally participate in the business. The answer depends on the type of founder: an individual (a citizen of another country) or a foreign company. Additionally, whether the country of citizenship is a member of the Eurasian Economic Union (EAEU) is also important.

Let's consider all three cases separately

Citizens of the EAEU: Russia, Belarus, Armenia, Kyrgyzstan

Citizens of these countries benefit from a simplified migration regime within the EAEU. They do not need a visa to do business in Kazakhstan.

However, visa-free entry does not automatically grant the right to be a founder of an LLP. To legally participate in a business, it is necessary to obtain a temporary residence permit (TRP) with the status of a business immigrant.

A TRP grants a business immigrant the right to:

Procedure for obtaining a TRP:

Citizens of Other Countries (Non-EAEU)

For citizens of all other countries, a business visa under category C5 is provided for opening an LLP or becoming a founder of an existing company in Kazakhstan.

This visa status is intended for foreign "business immigrants" — whose purpose of entry into Kazakhstan is related to entrepreneurial activity.

Basic rule: The C5 visa must be obtained in advance, before taking any legal action.

Difference between a C5 visa and visa-free entry or a tourist visa

Some people mistakenly think they can enter visa-free (for example, citizens of China or Turkey for 30 days) and register an LLP during that period. This is incorrect.

When registering an LLP with a foreign founder in Kazakhstan, the registering authority checks the migration status. The absence of a C5 visa (or a TRP for EAEU citizens) is grounds for refusal of registration.

Types of C5 visas:

What is needed to obtain a C5 visa

List of documents:

Foreign Legal Entities

The requirements are completely different for a foreign legal entity wishing to open a subsidiary (LLP) or a branch in Kazakhstan. If the founder is a foreign legal entity (regardless of the country of registration), obtaining a TRP or a C5 visa is not required.

Why? Because the founder is the company itself, not an individual. Migration requirements apply to foreign citizens, not corporate structures.

A founder-company:

A representative (e.g., the future director) acts on behalf of the company, but the founder remains the foreign legal entity.

This route is often chosen for the purpose of:

Documents required for registering an LLP through a foreign legal entity:

Frequently asked questions when a foreign citizen registers an LLP in Kazakhstan: is a visa required, is a temporary residence permit needed, and how to legally participate in the business. The answer depends on the type of founder: an individual (a citizen of another country) or a foreign company. Additionally, whether the country of citizenship is a member of the Eurasian Economic Union (EAEU) is also important.

Let's consider all three cases separately

Citizens of the EAEU: Russia, Belarus, Armenia, Kyrgyzstan

Citizens of these countries benefit from a simplified migration regime within the EAEU. They do not need a visa to do business in Kazakhstan.

However, visa-free entry does not automatically grant the right to be a founder of an LLP. To legally participate in a business, it is necessary to obtain a temporary residence permit (TRP) with the status of a business immigrant.

A TRP grants a business immigrant the right to:

- Officially register a new LLP;

- Join the founders of an already operating company; Reside in Kazakhstan legally for the period of conducting business.

Procedure for obtaining a TRP:

- Obtaining an Individual Identification Number (IIN);

- Undergoing a medical examination (confirming fitness for work);

- Fingerprinting;

- Submitting documents to the migration service.

Citizens of Other Countries (Non-EAEU)

For citizens of all other countries, a business visa under category C5 is provided for opening an LLP or becoming a founder of an existing company in Kazakhstan.

This visa status is intended for foreign "business immigrants" — whose purpose of entry into Kazakhstan is related to entrepreneurial activity.

Basic rule: The C5 visa must be obtained in advance, before taking any legal action.

- If you plan to register a new company - the visa must be obtained before submitting the registration documents;

- If you are purchasing a stake in an existing LLP - it must be obtained before including the notarized transaction.

Difference between a C5 visa and visa-free entry or a tourist visa

Some people mistakenly think they can enter visa-free (for example, citizens of China or Turkey for 30 days) and register an LLP during that period. This is incorrect.

When registering an LLP with a foreign founder in Kazakhstan, the registering authority checks the migration status. The absence of a C5 visa (or a TRP for EAEU citizens) is grounds for refusal of registration.

Types of C5 visas:

- Single-entry — issued for up to 90 days, for initially registering a company. Issued only outside Kazakhstan, through a consulate or embassy.

- Multiple-entry — issued for up to 2 years after the company is registered. To obtain it, you apply to the migration service in Kazakhstan with a petition from the local akimat (municipal administration).

What is needed to obtain a C5 visa

List of documents:

- An invitation letter processed through the Ministry of Internal Affairs;

- A foreign passport valid for at least 6 months;

- Medical insurance;

- A certificate of no criminal record from the country of citizenship (apostilled or legalized);

- A medical certificate confirming fitness for work.

- Register the LLP or join the founders;

- Contribute the charter capital (at least 100 MCI, in cash).

Foreign Legal Entities

The requirements are completely different for a foreign legal entity wishing to open a subsidiary (LLP) or a branch in Kazakhstan. If the founder is a foreign legal entity (regardless of the country of registration), obtaining a TRP or a C5 visa is not required.

Why? Because the founder is the company itself, not an individual. Migration requirements apply to foreign citizens, not corporate structures.

A founder-company:

- Cannot physically come to the country;

- Is not required to obtain an IIN;

- Does not undergo medical examinations or fingerprinting.

A representative (e.g., the future director) acts on behalf of the company, but the founder remains the foreign legal entity.

This route is often chosen for the purpose of:

- Simplifying migration procedures;

- Saving time on obtaining a TRP or visa;

- Opening a branch to enter the Kazakhstani market.

Documents required for registering an LLP through a foreign legal entity:

- A legalized extract from the trade register of the country of incorporation;

- A notarized translation of the constituent documents;

- The decision of the competent body of the foreign company to open an LLP in Kazakhstan.

2. Appointment of an LLP Director in Kazakhstan

When registering an LLP, the founders must determine the candidate for director.

1. Director is a Citizen of Kazakhstan

If a citizen of the Republic of Kazakhstan is appointed to the position of director, no additional permits, visas, or migration procedures are required. Such a director has full authority and can assume their position immediately after appointment in accordance with the company's charter.

2. Director is a Citizen of EAEU Countries (Russia, Belarus, Armenia, Kyrgyzstan)

Citizens of EAEU member states have a special legal regime for employment in Kazakhstan:

However, migration time limits must be considered:

If the director plans to stay in Kazakhstan continuously for more than 90 days or for a total of more than 180 days within a year, a temporary residence permit (TRP) must be obtained.

The basis for obtaining a TRP is the employment contract concluded with the LLP. When a complete and correctly prepared package of documents is submitted, the procedure is completed in the shortest possible time.

3. Director is a Citizen of Non-EAEU Countries

For citizens of non-EAEU countries (e.g., China, USA, Turkey, India, EU countries, etc.), appointing a director involves mandatory permit and visa stages: quota → permit for the employer → C3 visa for the employee.

Quota and Permit for the Employer: The Initial Mandatory Stage

Before inviting a specialist from outside the EAEU, the company in Kazakhstan must undergo the permit procedure established by law. The employer is granted the right to attract a foreign worker within the annual quota approved by the government.

Exceptions to the Quota: Cases Where a Permit is Not Required

The legislation provides for a number of cases where the employer is exempt from the obligation to obtain a permit to attract foreign labor.

This mechanism is called the "out-of-quota procedure" and applies to the following categories of foreign specialists:

C3 Visa: The Personal Entry Document for the Foreign Employee

Regardless of whether the employer has obtained a permit under the quota or applied an out-of-quota exception, the foreign citizen themselves must obtain a work visa under category C3.

This requirement is not a formality but a fundamental condition for:

1. Director is a Citizen of Kazakhstan

If a citizen of the Republic of Kazakhstan is appointed to the position of director, no additional permits, visas, or migration procedures are required. Such a director has full authority and can assume their position immediately after appointment in accordance with the company's charter.

2. Director is a Citizen of EAEU Countries (Russia, Belarus, Armenia, Kyrgyzstan)

Citizens of EAEU member states have a special legal regime for employment in Kazakhstan:

- No permit to attract foreign labor (IRS) or approval from migration authorities is required to hold the position of director.

- Managerial functions are carried out in full, without any restrictions.

However, migration time limits must be considered:

If the director plans to stay in Kazakhstan continuously for more than 90 days or for a total of more than 180 days within a year, a temporary residence permit (TRP) must be obtained.

The basis for obtaining a TRP is the employment contract concluded with the LLP. When a complete and correctly prepared package of documents is submitted, the procedure is completed in the shortest possible time.

3. Director is a Citizen of Non-EAEU Countries

For citizens of non-EAEU countries (e.g., China, USA, Turkey, India, EU countries, etc.), appointing a director involves mandatory permit and visa stages: quota → permit for the employer → C3 visa for the employee.

Quota and Permit for the Employer: The Initial Mandatory Stage

Before inviting a specialist from outside the EAEU, the company in Kazakhstan must undergo the permit procedure established by law. The employer is granted the right to attract a foreign worker within the annual quota approved by the government.

Exceptions to the Quota: Cases Where a Permit is Not Required

The legislation provides for a number of cases where the employer is exempt from the obligation to obtain a permit to attract foreign labor.

This mechanism is called the "out-of-quota procedure" and applies to the following categories of foreign specialists:

- Heads of branches and representative offices. Foreign citizens holding the position of the first head of an accredited branch or representative office of a foreign legal entity in Kazakhstan. In this case, the status of top manager is an automatic basis for exemption from permit procedures.

- Employees of the AIFC and Astana Hub. Residents of the Astana International Financial Center and participants of the Astana Hub technopark operate under a special legal regime. This allows them to attract foreign personnel in a simplified manner, without considering the general state quota.

- Top management of companies with 100% foreign participation. Directors and their deputies of legal entities in Kazakhstan that are wholly owned by foreign shareholders. The legislator assumes that the owner can independently determine the candidate for the person managing their assets.

- Specialists under intra-corporate transfer. Foreign employees working in Kazakhstan as part of an intra-corporate transfer (personnel rotation) by an employer within an international structure.

C3 Visa: The Personal Entry Document for the Foreign Employee

Regardless of whether the employer has obtained a permit under the quota or applied an out-of-quota exception, the foreign citizen themselves must obtain a work visa under category C3.

This requirement is not a formality but a fundamental condition for:

- Legally crossing the state border of the Republic of Kazakhstan;

- Lawful presence in the country;

- Legally carrying out subsequent work activities.

- The visa is issued at Kazakhstani consular offices abroad (in the country of citizenship or permanent residence).

- The basis for issuing the visa is a package of documents confirming the existence of an employment relationship:

- Permit for IRS (if required);

- Employment contract or a guarantee letter from the employer;

- Other documents as required by the consulate.

3. Preparing the Package of Documents for Registering an LLP with Foreign Capital Participation

The procedure for establishing a legal entity with foreign investments in Kazakhstan requires careful document preparation. The package of documents varies depending on the founder's status – whether they are an individual or a legal entity.

Section 1. Documents for Founders who are Individuals

If the founder of an LLP is a foreign citizen, the required package of documents includes:

1.1. Identity Document

Depending on citizenship and the basis for presence in the country, one of the following documents is provided:

If registration actions are carried out not by the founder personally but through their representative, a notarized power of attorney is required. The document must clearly specify the scope of authority and the validity period of the actions.

1.4. Individual Identification Number (IIN)

A mandatory requisite for all LLP participants, including the future director. The IIN is issued by the state revenue authorities of Kazakhstan and serves to uniquely identify an individual when interacting with government bodies, tax services, and registration authorities.

Section 2. Documents for Founders who are Legal Entities

If the founder is a foreign company, the package of documents differs:

2.1. Business Identification Number (BIN)

A unique code assigned to a foreign legal entity upon registration with the tax authorities in Kazakhstan. A BIN is a mandatory condition for any registration actions and subsequent interaction with government bodies.

2.2. Power of Attorney on Behalf of the Legal Entity

The document confirms the authority of an individual to carry out registration actions on behalf of the company;

The power of attorney must:

A document confirming the legal capacity, registration status, and current details of the foreign legal entity. Document requirements:

Section 1. Documents for Founders who are Individuals

If the founder of an LLP is a foreign citizen, the required package of documents includes:

1.1. Identity Document

- A copy of the foreign passport or other official document identifying the founder;

- Mandatory requirement: a notarized translation of the document into Kazakh and Russian.

Depending on citizenship and the basis for presence in the country, one of the following documents is provided:

- TRP (temporary residence permit) with the status "business immigrant" – for citizens of EAEU member states;

- Business visa under category C5 – for citizens of non-EAEU countries;

- Other document confirming the right to legally carry out entrepreneurial activity in the Republic of Kazakhstan.

If registration actions are carried out not by the founder personally but through their representative, a notarized power of attorney is required. The document must clearly specify the scope of authority and the validity period of the actions.

1.4. Individual Identification Number (IIN)

A mandatory requisite for all LLP participants, including the future director. The IIN is issued by the state revenue authorities of Kazakhstan and serves to uniquely identify an individual when interacting with government bodies, tax services, and registration authorities.

Section 2. Documents for Founders who are Legal Entities

If the founder is a foreign company, the package of documents differs:

2.1. Business Identification Number (BIN)

A unique code assigned to a foreign legal entity upon registration with the tax authorities in Kazakhstan. A BIN is a mandatory condition for any registration actions and subsequent interaction with government bodies.

2.2. Power of Attorney on Behalf of the Legal Entity

The document confirms the authority of an individual to carry out registration actions on behalf of the company;

The power of attorney must:

- be executed in accordance with the legislation of the country of origin;

- be notarized and, if necessary, translated into Kazakh and Russian;

- be apostilled or certified by a consulate if required.

A document confirming the legal capacity, registration status, and current details of the foreign legal entity. Document requirements:

- Legalization: Consular legalization for countries not party to the Hague Convention, apostille for participating countries;

- Translation: Notarized translation into Kazakh and Russian;

- Validity period: Must be current at the time of submission (usually should not exceed 6 months, but it is recommended to clarify with the registering authority).

4. Obtaining Identification Numbers: IIN and BIN

During the business registration process with foreign participation in Kazakhstan, each applicant is assigned a unique identification code, the type of which is determined by their legal status — an individual or a legal entity. This stage is mandatory and precedes the full functioning of the company.

IIN - Individual Identification Number for Individuals

An IIN is issued to all individuals, regardless of their citizenship and residency status. This unique digital code serves as a universal key to accessing public services and systems of the Republic of Kazakhstan.

The presence of an Individual Identification Number grants a foreign citizen access to the following services and procedures:

The procedure for issuing an IIN to non-residents is as follows:

Section 2. BIN - Business Identification Number for Legal Entities

The Business Identification Number (BIN) is a unique digital code assigned to all subjects of entrepreneurial activity operating in the territory of the Republic of Kazakhstan. This identifier serves as the company's official digital passport when interacting with government bodies, financial institutions, and counterparties.

A BIN is assigned to subjects of entrepreneurial activity, including:

To obtain a BIN for a foreign legal entity, it is necessary to submit a set of documents confirming its legal capacity and the legality of its intentions:

Official documents originating from foreign jurisdictions must undergo one of the following procedures to confirm their authenticity:

Documents executed in a foreign language must be translated into Russian and Kazakh. The translation must be made by a professional translator and certified by a notary (the translator's signature is certified).

Documents must be issued no later than 6 months before the date of submission. Outdated extracts are grounds for refusal to issue a BIN.

IIN - Individual Identification Number for Individuals

An IIN is issued to all individuals, regardless of their citizenship and residency status. This unique digital code serves as a universal key to accessing public services and systems of the Republic of Kazakhstan.

The presence of an Individual Identification Number grants a foreign citizen access to the following services and procedures:

- Obtaining documents granting the right to temporary or permanent residence in the RK;

- Participating in the establishment of a legal entity as a founder or director;

- Opening accounts in Kazakhstani financial institutions;

- Formally registering employment relations with an employer;

- Accessing the "Mobile Citizens" portal and obtaining an electronic digital signature (EDS).

The procedure for issuing an IIN to non-residents is as follows:

- Personal Presence: The foreigner must personally visit a Public Service Center (PSC) of the "Government for Citizens" NJSC. Remote processing is not provided.

- Required Documents :

- A valid foreign passport (original);

- A notarized translation of the passport into Kazakh and Russian (if the passport was issued in another language).

- Timeframe and Cost:

- Processing time — from 1 to 2 working days;

- The service is provided free of charge.

- Result: After the IIN is issued, the foreign citizen gains access to the "Mobile Citizens" database and the opportunity to obtain an EDS for electronic interaction with government bodies.

The Business Identification Number (BIN) is a unique digital code assigned to all subjects of entrepreneurial activity operating in the territory of the Republic of Kazakhstan. This identifier serves as the company's official digital passport when interacting with government bodies, financial institutions, and counterparties.

A BIN is assigned to subjects of entrepreneurial activity, including:

- Kazakhstani companies registered in accordance with the established procedure;

- Foreign companies operating in the RK through permanent establishments;

- Foreign companies opening bank accounts with banks in Kazakhstan;

- Separate subdivisions of foreign companies accredited in Kazakhstan;

- Persons engaged in entrepreneurship within the framework of joint activities (simple partnership).

To obtain a BIN for a foreign legal entity, it is necessary to submit a set of documents confirming its legal capacity and the legality of its intentions:

- The charter, foundation agreement, or other document defining the legal status of the company in its country of origin;

- Registration certificate, extract from the register of legal entities, tax registration document (depending on the jurisdiction) — submitted in two copies. The validity period of the extract, as a rule, should not exceed 6 months from the date of issue;

- Copies of identity documents with a notarized translation into Kazakh;

- An Individual Identification Number (IIN) for the head, obtained in advance in accordance with the procedure established for individuals;

- A document confirming the authority of the person authorized to carry out registration actions on behalf of the company (power of attorney).

Official documents originating from foreign jurisdictions must undergo one of the following procedures to confirm their authenticity:

- Notarization. For EAEU member states.

- Apostille. For states party to the 1961 Hague Convention (affixed by the competent authority of the country where the document was issued).

- Consular legalization. For states not party to the Hague Convention (carried out through consular offices of the RK abroad).

Documents executed in a foreign language must be translated into Russian and Kazakh. The translation must be made by a professional translator and certified by a notary (the translator's signature is certified).

Documents must be issued no later than 6 months before the date of submission. Outdated extracts are grounds for refusal to issue a BIN.

5. Connecting to the Mobile Citizens Base: Digital Registration in Kazakhstan

After obtaining an Individual Identification Number, the foreigner faces the next mandatory stage — integration into the Mobile Citizens Base. Without this step, it is impossible to speak of a full presence in the country's digital space. The MCD system acts as a kind of digital concierge that accompanies any user every time, they access state information resources.

The Anatomy of the Mobile Citizens Base: How It Is Organized

The Mobile Citizens Base is a unified register that stores up-to-date information about the assignment of subscriber numbers to specific individuals. This is not just a state phone book, but a complex verification mechanism that guarantees that behind every online request there is a real person, not an automated script or an attacker.

The system's operating principle is based on simple logic: any significant request to state information systems requires double confirmation. The first factor is knowledge of the login and password, the second is possession of a specific mobile device that receives a one-time code. The MCB ensures this second level of security.

The system performs a number of tasks that the average user often doesn't think about. When a citizen logs into the e-government portal and enters an SMS code, a request to the Mobile Citizens Base lies behind this action. When the state automatically notifies about the possibility of applying for benefits or obtaining a certificate - this is also the work of the MCB. When several public services are combined into one package and provided in a proactive mode — this would be impossible without data from the Mobile Citizens Base.

What a Foreigner Needs for Registration

Unlike many bureaucratic procedures that require piles of paper and hours of waiting, registration in the MCD is as concise as possible in terms of requirements, but strict in terms of execution.

Geography of Operation: Where Does the SIM Card Work After Activation

There is a common misconception that a Kazakhstani SIM card turns into useless plastic outside the country. In practice, everything is different. After the number is initially activated within the republic, it retains the ability to receive SMS messages anywhere in the world where there is mobile coverage.

This means that by flying on a business trip to Europe, going on vacation to their homeland, or going on a business trip to Asia, a foreigner can still receive confirmation codes to access Kazakhstani state systems. The roaming function works normally, and the geographical location of the number owner does not affect the ability to authorize on the egov.kz portal or in the mobile applications of state bodies.

The Anatomy of the Mobile Citizens Base: How It Is Organized

The Mobile Citizens Base is a unified register that stores up-to-date information about the assignment of subscriber numbers to specific individuals. This is not just a state phone book, but a complex verification mechanism that guarantees that behind every online request there is a real person, not an automated script or an attacker.

The system's operating principle is based on simple logic: any significant request to state information systems requires double confirmation. The first factor is knowledge of the login and password, the second is possession of a specific mobile device that receives a one-time code. The MCB ensures this second level of security.

The system performs a number of tasks that the average user often doesn't think about. When a citizen logs into the e-government portal and enters an SMS code, a request to the Mobile Citizens Base lies behind this action. When the state automatically notifies about the possibility of applying for benefits or obtaining a certificate - this is also the work of the MCB. When several public services are combined into one package and provided in a proactive mode — this would be impossible without data from the Mobile Citizens Base.

What a Foreigner Needs for Registration

Unlike many bureaucratic procedures that require piles of paper and hours of waiting, registration in the MCD is as concise as possible in terms of requirements, but strict in terms of execution.

- First of all, a mobile phone is needed — any device capable of receiving text messages. The technical specifications of the device are not important: a new smartphone or a simple "feature phone" will do.

- The second component is a SIM card from one of the Kazakhstani operators. The republic's mobile communications market is represented by four players: Activ , Beeline, Tele2, and Altel, and any of them is suitable for registration purposes. However, this is where the most important nuance lies: the SIM card must be activated for the first time strictly within the territory of Kazakhstan. This condition is fundamentally important because the system records the moment of the number's initial registration on the network and links it to a specific subscriber. Cards purchased outside the country or previously activated in other states are not suitable for registration.

- The third necessary condition is the presence of a valid IIN. The Mobile Citizens Base works in conjunction with identification numbers, so attempting to register without first obtaining an IIN will fail.

Geography of Operation: Where Does the SIM Card Work After Activation

There is a common misconception that a Kazakhstani SIM card turns into useless plastic outside the country. In practice, everything is different. After the number is initially activated within the republic, it retains the ability to receive SMS messages anywhere in the world where there is mobile coverage.

This means that by flying on a business trip to Europe, going on vacation to their homeland, or going on a business trip to Asia, a foreigner can still receive confirmation codes to access Kazakhstani state systems. The roaming function works normally, and the geographical location of the number owner does not affect the ability to authorize on the egov.kz portal or in the mobile applications of state bodies.

6. Obtaining an Electronic Digital Signature: The Legal Analog of a Handwritten Signature in the Digital Space

An Electronic Digital Signature is a special cryptographic tool recognized in the legal framework of Kazakhstan as a full-fledged equivalent of a handwritten signature on a paper medium. For a foreign citizen carrying out entrepreneurial activities or labor functions in the republic, obtaining an EDS signifies a transition to a qualitatively new level of interaction with state institutions and business partners.

Legislative Basis for Using EDS

The regulatory framework for using an electronic digital signature is the Law of the Republic of Kazakhstan "On Electronic Document and Electronic Digital Signature." This legislative act establishes a fundamentally important norm: a document existing in electronic form and certified by an EDS has the same legal force as a document executed on paper and certified by a traditional signature.

Far-reaching practical consequences follow from this provision. A contract signed with an electronic signature via the egov.kz portal has the same evidentiary force in judicial instances as a multi-page paper contract with wet seals. A tax declaration sent in electronic form and certified by an EDS is considered submitted on time, with all formalities observed. An application submitted digitally to amend a company's registration data is processed by government bodies just as quickly as if the applicant had visited a PSC in person.

Internal Structure of EDS: The Cryptographic Nature of the Digital Key

Technically, an electronic digital signature consists of two interconnected files containing unique cryptographic sequences of characters. These files perform different functions but are inextricably linked.

The first component is the private key. It is known only to the owner and is used directly for signing electronic documents. This file cannot be transferred to third parties, as its possessor gains the ability to sign any documents on behalf of the legal owner.

The first component is the private key. It is known only to the owner and is used directly for signing electronic documents. This file cannot be transferred to third parties, as its possessor gains the ability to sign any documents on behalf of the legal owner.

Both components are ordinary computer files that have no physical form but can be stored on various media. The user can choose any convenient storage option depending on their preferences and technical capabilities:

Prerequisites for a Foreign Citizen to Obtain an EDS

The procedure for obtaining an electronic digital signature becomes available to a foreigner only after fulfilling two mandatory prerequisites.

Methods for Obtaining an Electronic Digital Signature

Processing at a Public Service Center

When visiting a PSC, you must have with you:

Practical Areas of EDS Application in a Foreigner's Activities

After obtaining an electronic digital signature, a foreign citizen gains access to a wide range of opportunities for interacting with government bodies and commercial structures.

Interaction with Government Bodies

EDS allows the following procedures to be completely transferred to a digital format:

In commercial activities, EDS is used for:

For entrepreneurs planning to participate in public procurement or commercial tenders, having an EDS is a mandatory condition. Without it, it is impossible to submit an application, sign protocols, or conclude a contract based on the auction results.

Opening and Managing Bank Accounts

Many banks in Kazakhstan allow remote opening and management of accounts by signing applications and orders using an EDS. This significantly simplifies banking services for foreigners, especially when they are outside the republic.

Registering Real Estate and Vehicles

Procedures for registering rights to real estate and vehicles are also available in electronic format when an EDS is available, allowing property transactions to be conducted without personally visiting registering authorities.

Legislative Basis for Using EDS

The regulatory framework for using an electronic digital signature is the Law of the Republic of Kazakhstan "On Electronic Document and Electronic Digital Signature." This legislative act establishes a fundamentally important norm: a document existing in electronic form and certified by an EDS has the same legal force as a document executed on paper and certified by a traditional signature.

Far-reaching practical consequences follow from this provision. A contract signed with an electronic signature via the egov.kz portal has the same evidentiary force in judicial instances as a multi-page paper contract with wet seals. A tax declaration sent in electronic form and certified by an EDS is considered submitted on time, with all formalities observed. An application submitted digitally to amend a company's registration data is processed by government bodies just as quickly as if the applicant had visited a PSC in person.

Internal Structure of EDS: The Cryptographic Nature of the Digital Key

Technically, an electronic digital signature consists of two interconnected files containing unique cryptographic sequences of characters. These files perform different functions but are inextricably linked.

The first component is the private key. It is known only to the owner and is used directly for signing electronic documents. This file cannot be transferred to third parties, as its possessor gains the ability to sign any documents on behalf of the legal owner.

The first component is the private key. It is known only to the owner and is used directly for signing electronic documents. This file cannot be transferred to third parties, as its possessor gains the ability to sign any documents on behalf of the legal owner.

Both components are ordinary computer files that have no physical form but can be stored on various media. The user can choose any convenient storage option depending on their preferences and technical capabilities:

- Stationary computer or laptop - a classic solution for office work, providing constant access to keys at the workplace;

- Mobile phone - a modern option for those who value mobility and the ability to sign documents anywhere in the world;

- Tablet computer — an intermediate solution combining functionality and portability;

- External USB drive — a traditional medium that can be carried around as a key fob and used on any computer;

- Secure cloud storage — an innovative storage method where keys are not tied to a specific device but are accessible through a personal account on the e-government portal.

Prerequisites for a Foreign Citizen to Obtain an EDS

The procedure for obtaining an electronic digital signature becomes available to a foreigner only after fulfilling two mandatory prerequisites.

- The first and main condition is the presence of an Individual Identification Number. The IIN acts as the digital foundation upon which all subsequent interaction of the foreigner with state information systems is built. Applying for an EDS without an assigned IIN is pointless — the system simply will not find the subject to whom the keys could be issued.

- The second condition is registration in the Mobile Citizens Base using a local subscriber number that has passed the biometric identification procedure. This requirement ensures two-factor authentication when working with state portals and the ability to confirm operations using an EDS.

Methods for Obtaining an Electronic Digital Signature

Processing at a Public Service Center

When visiting a PSC, you must have with you:

- An identity document (foreign passport);

- A document confirming the assignment of an IIN;

- A notarized translation of the passport (if it was issued in a language other than Russian and Kazakh).

Practical Areas of EDS Application in a Foreigner's Activities

After obtaining an electronic digital signature, a foreign citizen gains access to a wide range of opportunities for interacting with government bodies and commercial structures.

Interaction with Government Bodies

EDS allows the following procedures to be completely transferred to a digital format:

- Submitting tax and statistical reports;

- Sending applications for registration of legal entities and amendments to constituent documents;

- Obtaining official certificates and extracts from state registers;

- Monitoring the status of submitted documents;

- Sending official inquiries and receiving responses;

- Appealing the actions of officials through administrative procedures.

In commercial activities, EDS is used for:

- Concluding contracts with counterparties and partners;

- Signing additional agreements to existing contracts;

- Executing acts of completed work and rendered services;

- Issuing invoices for payment;

- Sending official offers and commercial inquiries;

- Conducting correspondence with legal significance.

For entrepreneurs planning to participate in public procurement or commercial tenders, having an EDS is a mandatory condition. Without it, it is impossible to submit an application, sign protocols, or conclude a contract based on the auction results.

Opening and Managing Bank Accounts

Many banks in Kazakhstan allow remote opening and management of accounts by signing applications and orders using an EDS. This significantly simplifies banking services for foreigners, especially when they are outside the republic.

Registering Real Estate and Vehicles

Procedures for registering rights to real estate and vehicles are also available in electronic format when an EDS is available, allowing property transactions to be conducted without personally visiting registering authorities.

7. Who We Are by Size: Small, Medium, or Large Business?

Before registering an LLP, it is advisable to understand in advance which category of entrepreneurship your company will fall into. This affects not only reporting and taxes but also the volume of administrative burden, capital requirements, and sometimes access to state support.

In Kazakhstan, businesses are divided into three categories - based on the number of employees and the volume of assets.

Small Business

This includes companies with:

Medium Business

A category for those who have outgrown the small format:

Large Business

This category includes companies with:

What Else Is Important to Know About the MCI

All calculations are tied to the Monthly Calculation Index (MCI). This is not just a number, but a universal coefficient that changes annually.

For 2026, the MCI amount is set at 4,235 tenge. This amount is used to calculate:

In Kazakhstan, businesses are divided into three categories - based on the number of employees and the volume of assets.

Small Business

This includes companies with:

- Number of employees up to 50 people;

- Assets not exceeding 60,000 MCI.

Medium Business

A category for those who have outgrown the small format:

- Staff - from 51 to 250 people;

- Assets — up to 325,000 MCI.

Large Business

This category includes companies with:

- Number of employees over 250 people;

- Assets over 325,000 MCI.

What Else Is Important to Know About the MCI

All calculations are tied to the Monthly Calculation Index (MCI). This is not just a number, but a universal coefficient that changes annually.

For 2026, the MCI amount is set at 4,235 tenge. This amount is used to calculate:

- Tax liabilities;

- Social contributions;

- Fines and state duties;

- Limit values for assets and income.

8. Forming the Charter Capital

Charter capital is not just a formality; it is the company's initial financial foundation. It is formed from the contributions of the founders and serves several purposes simultaneously:

«What the Law Requires

The legislation divides businesses by size and imposes different requirements:

What to Choose in Practice?

Zero tenge is a working option, but with caveats.

If the goal is to save at the start, you can contribute nothing. However, be prepared that a company with zero capital may sometimes seem less credible. Partners, banks, or tender participants may view a legal entity with no financial foundation cautiously.

It's better to link capital to initial expenses.

Calculate how much will be needed for the first month's rent, basic equipment, or registration fees. Contribute this amount - often it is 100,000 – 250,000 tenge. Then capital becomes not just a number, but a working tool.

If the business is immediately focused on large contracts, the capital should correspond to the scale of the transactions. Major clients and creditors look not only at promises but also at the balance sheet.

Three Important Rules

- Provides initial liquidity - something is needed to pay rent, purchase equipment, make advance payments;

- Shows counterparties that the business has substance;

- Creates a minimal "cushion" for creditors if things go wrong.

«What the Law Requires

The legislation divides businesses by size and imposes different requirements:

- Small businesses can operate without any charter capital at all. The minimum limit is 0 tenge.

- Medium and large companies are obliged to form capital of no less than 100 MCI. In 2026, this is 432,500 tenge.

What to Choose in Practice?

Zero tenge is a working option, but with caveats.

If the goal is to save at the start, you can contribute nothing. However, be prepared that a company with zero capital may sometimes seem less credible. Partners, banks, or tender participants may view a legal entity with no financial foundation cautiously.

It's better to link capital to initial expenses.

Calculate how much will be needed for the first month's rent, basic equipment, or registration fees. Contribute this amount - often it is 100,000 – 250,000 tenge. Then capital becomes not just a number, but a working tool.

If the business is immediately focused on large contracts, the capital should correspond to the scale of the transactions. Major clients and creditors look not only at promises but also at the balance sheet.

Three Important Rules

- Who contributes? Only the founders. If the director is hired externally, they are not involved in forming the capital.

- When to contribute. You have one year from the moment the LLP is registered to contribute the funds. Earlier is possible, delaying is not allowed.

- How to contribute if the founder is remote. There's no need to visit the bank in person. You can issue a power of attorney to a representative in advance or, if the bank allows, make a non-cash transfer. The main thing is to think this through before registration, not to urgently look for workarounds later.

9. Choosing and checking the LLP Name

The name of an LLP is not just a line in the charter. It is the face of your business. Acquaintance with clients, partners, and banks begins with it. A successful name is remembered, inspires confidence, and works for your reputation. An unsuccessful one creates problems, lawsuits, and extra costs.

Therefore, choosing a name should be approached not creatively, but strategically.

What the Law Says: Mandatory Requirements

According to Article 38 of the Civil Code of the RK and Article 4 of the Law "On Limited and Additional Liability Partnerships," the name of an LLP must consist of two parts:

Example: "Vita Liberta" LLP, Vita Liberta LLP

The name may additionally use:

Three Main Prohibitions: What Cannot Be Used

1. No duplication of existing companies

The company name must be unique. The law directly prohibits using a name that fully or substantially coincides with a previously registered legal entity.

If you are named like another player in the market, the registrar will refuse. If you are mistakenly registered, the owner of the previously established company can demand through court that you stop using the name and compensate for losses.

2. No infringement of trademark rights

Even if a name is free as a legal entity name, it may turn out to be someone else's registered trademark. The trademark owner has the exclusive right to use it. If you register an LLP with a name confusingly similar to another brand, the rights holder can:

3. No use of prohibited elements

It is forbidden to include in the name:

Checklist: How to Choose a Name That Won't Cause Problems

1. Check uniqueness among legal entities

This is the first and simplest filter. You can check for free on the egov.kz portal. Go to the "Business" section, then to "Business Registration and Development," select the item "Information about legal entities, branches, representative offices." Enter your desired name and check if it is available.

If the name is taken, you'll have to think of another one. Even minor differences, like one letter or a different word order, might allow the name to pass, but it's important not to create confusing similarity here.

2. Check trademarks

This is a deeper check, but it is this one that will protect you from future court cases. Checks can be carried out through the open registers of the National Institute of Intellectual Property (NIIP, Qazpatent). If the budget allows, you can use paid databases and services or consult a patent attorney.

What to check for: identical designations (full match) and confusingly similar designations (by sound, meaning, spelling). If your future brand coincides with a registered trademark in the same field of activity, it's better to abandon the idea immediately.

3. Consider the Kazakh language

If you plan to use a Kazakh-language name for operating in the domestic market, make sure it is spelled correctly, translated properly, does not lose meaning during transliteration, and does not create unexpected associations.

The use of the Kazakh language is mandatory for state organizations and encouraged for private ones.

4. Think about the future

If the business is aimed at the international market, the name should be easily readable and memorable in the Latin alphabet, have no negative or funny meanings in other languages, and be suitable for international registration trademark if you plan to expand.

For international trademark registration, you can use the Madrid System, but for this, you must first have a national registration in Kazakhstan.

5. Check domain and social media

Even if the name is legally free, check the availability of the domain in kz, com, ru, and other zones, as well as the availability of accounts on Instagram, Facebook, Telegram. It's good if the company name, domain, and social media match - it's convenient for clients and strengthens the brand.

What Happens If You Neglect the check?

1. Refusal of Registration

The registrar automatically checks the uniqueness of the name among operating legal entities through the PSC or eGov. If there's a match — refusal follows. You'll have to change the name and resubmit documents, losing time and state fees.

2. Lawsuit from the Trademark Owner

Imagine: you registered an LLP, opened an account, printed a signboard, launched advertising. Then you receive a letter from a lawyer demanding you stop using the name and pay compensation.

According to Article 1020 of the Civil Code of the RK, the exclusive right to a means of individualization has priority for the means whose right arose earlier. If the trademark was registered before your LLP, you are in the risk zone. Consequences may include a ban on using the name, changing the name and re-registering the LLP, compensating the rights holder for losses, and covering court costs.

3. Confusion in the Market

Even without court cases, if your name is similar to a well-known competitor, clients will get confused. Some of the audience will think you are them and go there, while another part will distrust you because of the dubious similarity. Reputational losses are hard to measure, but they are inevitable.

Can the Name Be Changed After Registration?

Yes, such a possibility exists. The procedure depends on the number of founders. With one founder, a decision of the sole participant is made; with several, a protocol of the general meeting is drawn up.

After the decision is made, you need to amend the charter or develop a new version of the charter, submit documents for re-registration to the PSC or via eGov, and then obtain new documents with the changed name.

It is important to understand: when changing the name, you will have to renegotiate contracts with counterparties, notify the bank, replace the seal, update the signboard and website. These are significant costs, which are better avoided by choosing the right name the first time.

Name and Brand: What's the Difference

It is important to understand that an LLP name and a trademark are different tools.

The LLP name is fixed in the charter and the register of legal entities. It protects the company's identification as a legal entity within Kazakhstan and is valid for as long as the company exists.

A trademark is registered in the NIIP register and protects the brand, product, or service. It can operate both in Kazakhstan and in other countries as desired and must be renewed every ten years.

Therefore, even if you register an LLP name, it does not protect you from competitors copying your brand. For full protection, you need to register a trademark separately.

Therefore, choosing a name should be approached not creatively, but strategically.

What the Law Says: Mandatory Requirements

According to Article 38 of the Civil Code of the RK and Article 4 of the Law "On Limited and Additional Liability Partnerships," the name of an LLP must consist of two parts:

- The name (what you come up with);

- A reference to the organizational and legal form is “limited liability partnership” or the abbreviation “LLP”.

Example: "Vita Liberta" LLP, Vita Liberta LLP

The name may additionally use:

- An abbreviated form;

- Equivalents in foreign languages;

- An indication of state affiliation if there are foreigners among the founders (eg, "Kazakhstan-Russian...").

Three Main Prohibitions: What Cannot Be Used

1. No duplication of existing companies

The company name must be unique. The law directly prohibits using a name that fully or substantially coincides with a previously registered legal entity.

If you are named like another player in the market, the registrar will refuse. If you are mistakenly registered, the owner of the previously established company can demand through court that you stop using the name and compensate for losses.

2. No infringement of trademark rights

Even if a name is free as a legal entity name, it may turn out to be someone else's registered trademark. The trademark owner has the exclusive right to use it. If you register an LLP with a name confusingly similar to another brand, the rights holder can:

- Prohibit the use of that name;

- Demand compensation for losses.

3. No use of prohibited elements

It is forbidden to include in the name:

- Words contrary to public morals;

- Official names of state bodies (if you are not a state body);

- Names of famous persons without permission (or permission from their heirs).

Checklist: How to Choose a Name That Won't Cause Problems

1. Check uniqueness among legal entities

This is the first and simplest filter. You can check for free on the egov.kz portal. Go to the "Business" section, then to "Business Registration and Development," select the item "Information about legal entities, branches, representative offices." Enter your desired name and check if it is available.

If the name is taken, you'll have to think of another one. Even minor differences, like one letter or a different word order, might allow the name to pass, but it's important not to create confusing similarity here.

2. Check trademarks

This is a deeper check, but it is this one that will protect you from future court cases. Checks can be carried out through the open registers of the National Institute of Intellectual Property (NIIP, Qazpatent). If the budget allows, you can use paid databases and services or consult a patent attorney.

What to check for: identical designations (full match) and confusingly similar designations (by sound, meaning, spelling). If your future brand coincides with a registered trademark in the same field of activity, it's better to abandon the idea immediately.

3. Consider the Kazakh language

If you plan to use a Kazakh-language name for operating in the domestic market, make sure it is spelled correctly, translated properly, does not lose meaning during transliteration, and does not create unexpected associations.

The use of the Kazakh language is mandatory for state organizations and encouraged for private ones.

4. Think about the future

If the business is aimed at the international market, the name should be easily readable and memorable in the Latin alphabet, have no negative or funny meanings in other languages, and be suitable for international registration trademark if you plan to expand.

For international trademark registration, you can use the Madrid System, but for this, you must first have a national registration in Kazakhstan.

5. Check domain and social media

Even if the name is legally free, check the availability of the domain in kz, com, ru, and other zones, as well as the availability of accounts on Instagram, Facebook, Telegram. It's good if the company name, domain, and social media match - it's convenient for clients and strengthens the brand.

What Happens If You Neglect the check?

1. Refusal of Registration

The registrar automatically checks the uniqueness of the name among operating legal entities through the PSC or eGov. If there's a match — refusal follows. You'll have to change the name and resubmit documents, losing time and state fees.

2. Lawsuit from the Trademark Owner

Imagine: you registered an LLP, opened an account, printed a signboard, launched advertising. Then you receive a letter from a lawyer demanding you stop using the name and pay compensation.

According to Article 1020 of the Civil Code of the RK, the exclusive right to a means of individualization has priority for the means whose right arose earlier. If the trademark was registered before your LLP, you are in the risk zone. Consequences may include a ban on using the name, changing the name and re-registering the LLP, compensating the rights holder for losses, and covering court costs.

3. Confusion in the Market

Even without court cases, if your name is similar to a well-known competitor, clients will get confused. Some of the audience will think you are them and go there, while another part will distrust you because of the dubious similarity. Reputational losses are hard to measure, but they are inevitable.

Can the Name Be Changed After Registration?

Yes, such a possibility exists. The procedure depends on the number of founders. With one founder, a decision of the sole participant is made; with several, a protocol of the general meeting is drawn up.

After the decision is made, you need to amend the charter or develop a new version of the charter, submit documents for re-registration to the PSC or via eGov, and then obtain new documents with the changed name.

It is important to understand: when changing the name, you will have to renegotiate contracts with counterparties, notify the bank, replace the seal, update the signboard and website. These are significant costs, which are better avoided by choosing the right name the first time.

Name and Brand: What's the Difference

It is important to understand that an LLP name and a trademark are different tools.

The LLP name is fixed in the charter and the register of legal entities. It protects the company's identification as a legal entity within Kazakhstan and is valid for as long as the company exists.

A trademark is registered in the NIIP register and protects the brand, product, or service. It can operate both in Kazakhstan and in other countries as desired and must be renewed every ten years.

Therefore, even if you register an LLP name, it does not protect you from competitors copying your brand. For full protection, you need to register a trademark separately.

10. Choosing Types of Activities (GC)

In Kazakhstan, entrepreneurs can indeed engage in any types of activities not prohibited by law. This is not just a phrase — it is a principle that gives businesses freedom to maneuver. You are not rigidly tied to one direction and can flexibly respond to market changes, add new services, or change your profile.

But freedom does not mean "just put anything down." The choice of GC codes should be approached consciously. Because not only the elegance of the charter depends on this, but also taxes, reporting, licenses, and sometimes the very ability to work legally.

What is General Classifier and Why is it Needed?

General Classifier stands for General Classifier of Types of Economic Activity. In essence, it is a digital code that shows the state what your company actually does. Whether you make furniture, sell flowers, consult startups, or rent out premises - everything has its own code.

These codes are not just for formality. They affect:

Main and Additional Codes: What's the Difference

When registering an LLP, you need to choose one main code and up to four additional codes. The main one is the type of activity that brings in the largest portion of revenue or defines the company's profile. The additional ones are everything else you plan to do.

The law does not prohibit adding codes as a reserve, even if it's not yet certain whether you will actually conduct this activity. But it's important to have a sense of proportion and understand the consequences. For example, if you add a code that requires a license, but you don't have one — that's a risk. Formally, you have declared that you can engage in this activity, but in reality, you have no right. It's better not to add such codes until you are actually ready to obtain the permit.

Where to Find Codes and How to Check Them

The current KVED classifier can be found on the website of the National Statistics Bureau (stat.gov.kz) or on specialized resources. Codes are detailed up to five characters - exactly what is needed for registration.

Before finalizing the list, it is useful to:

Licensed Types of Activities: When a Code is Not Enough, You Need a Permit

In Kazakhstan, some types of activities cannot be started simply by indicating the code during registration. They require a license. This includes, for example:

Notification Procedure: When You Just Need to Notify

For some types of activities, a license is not required, but it is necessary to send a notification to state bodies. This is easier than obtaining a license, but still mandatory. For example, notification is required for:

How Many Codes Can Be Added?

The maximum number of codes that can be specified during registration is 5 (one main and four additional). But this does not mean you are forever limited to five types of activities. After registration, you can add new codes through the same services — there are no restrictions on the total number. The main thing is that all added codes correspond to actual or planned activities.

Changes in 2026: What to Pay Attention To

From 2026, important amendments come into force in Kazakhstan for certain categories of business.

But freedom does not mean "just put anything down." The choice of GC codes should be approached consciously. Because not only the elegance of the charter depends on this, but also taxes, reporting, licenses, and sometimes the very ability to work legally.

What is General Classifier and Why is it Needed?

General Classifier stands for General Classifier of Types of Economic Activity. In essence, it is a digital code that shows the state what your company actually does. Whether you make furniture, sell flowers, consult startups, or rent out premises - everything has its own code.

These codes are not just for formality. They affect:

- The tax regime (whether you can work on a simplified basis or have to switch to the general regime);

- The need to obtain licenses or send notifications;

- The form of statistical reporting;

- Participation in public procurement and tenders;

- Interaction with banks and partners.

Main and Additional Codes: What's the Difference

When registering an LLP, you need to choose one main code and up to four additional codes. The main one is the type of activity that brings in the largest portion of revenue or defines the company's profile. The additional ones are everything else you plan to do.

The law does not prohibit adding codes as a reserve, even if it's not yet certain whether you will actually conduct this activity. But it's important to have a sense of proportion and understand the consequences. For example, if you add a code that requires a license, but you don't have one — that's a risk. Formally, you have declared that you can engage in this activity, but in reality, you have no right. It's better not to add such codes until you are actually ready to obtain the permit.

Where to Find Codes and How to Check Them

The current KVED classifier can be found on the website of the National Statistics Bureau (stat.gov.kz) or on specialized resources. Codes are detailed up to five characters - exactly what is needed for registration.

Before finalizing the list, it is useful to:

- Look at what codes competitors or companies in your industry use;

- Check that the selected code does not require a license or notification;

- Ensure that the code actually describes what you plan to do (sometimes the name sounds similar, but the meaning is different).

Licensed Types of Activities: When a Code is Not Enough, You Need a Permit

In Kazakhstan, some types of activities cannot be started simply by indicating the code during registration. They require a license. This includes, for example:

- Financial services (banks, insurance, microcredits);

- Medical and pharmaceutical activities;

- Production and circulation of alcohol;

- Educational services (schools, universities, training centers);

- Construction and installation works (under certain conditions);

- Transportation of passengers and dangerous goods;

- Private security services.

Notification Procedure: When You Just Need to Notify

For some types of activities, a license is not required, but it is necessary to send a notification to state bodies. This is easier than obtaining a license, but still mandatory. For example, notification is required for:

- Starting activities in the field of public catering;

- Providing personal services;

- Certain types of retail trade;

- Taxi services.

How Many Codes Can Be Added?

The maximum number of codes that can be specified during registration is 5 (one main and four additional). But this does not mean you are forever limited to five types of activities. After registration, you can add new codes through the same services — there are no restrictions on the total number. The main thing is that all added codes correspond to actual or planned activities.

Changes in 2026: What to Pay Attention To

From 2026, important amendments come into force in Kazakhstan for certain categories of business.

- For the self-employed, a specific list of activities (40 KVED codes) has been approved for which the special tax regime is allowed. If the type of activity is not included in this list, the regime for the self-employed cannot be applied. For LLPs, this is not a direct restriction, but a signal: the state is beginning to regulate more clearly which types of activities are allowed under which regimes.

- The possibility of retaining simplified taxes for the creative industry and IT is being discussed, but the final lists are still being formed. If your business is related to this area, it is advisable to monitor updates on the "Open NLA" portal and, if necessary, send inquiries to the authorized bodies.

11. Choosing an Address for the Company in Kazakhstan

When the question arises about the location of an LLP's registration, many entrepreneurs think: "Maybe I'll just indicate my home address or buy a 'legal' address? If I work remotely, why pay for an office?"

The logic is understandable. But the law and tax authorities think differently.

We will analyze the main points: the difference between a “physical office” and a “legal address,” what options exist, what has changed this year, and what risks someone takes who decides to save on an address.

Kazakhstan, the legislation does not contain the concept of "legal address." There is the concept of the "location of the legal entity." According to Article 39 of the Civil Code of the RK, this is the location of its permanent working body – usually, the executive body (director, board).

In simple terms: it is the address where the company's management actually works, where documents are stored, where you can come for an inspection, and where the tax authority has the right to find you.

This address is entered into:

The Main Change in 2026: Ban on Fake Addresses

If previously it was possible to register an LLP at a "rubber" address by buying a lease agreement from a dubious firm, the rules have become significantly stricter since November 2025.

Order No. 687 of the Ministry of Justice dated November 21, 2025, introduced:

What does this mean in practice:

LLP Address Options: What Works in 2026

1. Founder's Home Address

If the founder is the owner of an apartment, they can register the LLP at their home address.

Advantages:

2. Renting an Office in a Business Center or from an Individual

The most common option for small and medium businesses.

What is needed: