Can I register an LLP with a single founder?

Step-by-Step Guide for Non-Residents: Opening an LLP in Kazakhstan

May 06, 2026

Kazakhstan is a promising country for establishing a company, offering a favorable investment climate, developed infrastructure, and stable economic growth. This article provides a detailed overview of each step involved in starting a business in Kazakhstan: from choosing the appropriate legal form to registration nuances, required documentation, and tax obligations. Special focus is given to one of the most popular forms of entrepreneurship — the Limited Liability Partnership (LLP), including its advantages, registration process, and key operational aspects.

Contents

Advantages of Establishing a Company in Kazakhstan

The Republic of Kazakhstan offers impressive prospects for business development, becoming an increasingly attractive destination for investors worldwide. The country's position on the international stage is supported by a number of significant advantages, including:

- Strategic Geographical Location

Situated at the crossroads of Europe and Asia, Kazakhstan plays a key role in international transport and logistics networks. The country provides efficient connections between major economic regions, making it an important hub in global trade routes. This creates extensive opportunities for expanding logistics infrastructure, reducing transportation costs, and making Kazakhstan more attractive to foreign businessmen.

- Economic Stability

Kazakhstan’s economy demonstrates stable macroeconomic indicators: moderate GDP growth, low inflation, and a stable tenge exchange rate. Economic diversification and balanced fiscal policy ensure long-term sustainability, making Kazakhstan a reliable place for entrepreneurial activity and investment.

- Domestic Market Potential

Kazakhstan’s domestic market comprises over 20 million consumers with growing purchasing power. The expanding middle class stimulates demand for goods and services, providing opportunities for retail, manufacturing, and service organizations.

- Qualified Workforce

Kazakhstan’s education system trains specialists who meet modern labor market requirements. The country offers access to skilled labor at competitive costs, which is especially important for industrial and technological projects.

- Modern and Well-Developed Infrastructure

Kazakhstan invests significant financial resources in improving its transport network, manufacturing sector, and digital environment. New highways, railways, airports, industrial clusters, and technology parks create a favorable environment for entrepreneurship. Intensive use of digital solutions promotes the transition to a digital economy and strengthens companies’ competitive positions.

- Active Participation in International Relations

Kazakhstan is a member of the Eurasian Economic Union (EAEU), ensuring free access to the EAEU markets with a population of over 180 million people. The country also actively develops trade relations with other regions, including Asia and Europe, opening additional opportunities for export and international cooperation.

- Stable Political and Economic Environment

Kazakhstan is one of the most stable countries in the region. The country pursues a policy of multilateral constructive cooperation, does not follow the interests of third countries, but pursues its own national interests. Kazakhstan maintains balanced relations with major world economies such as Russia, China, the USA, and the EU.

- Full Foreign Ownership of Business

Kazakhstan does not restrict foreign investors in terms of business ownership. 100% foreign capital is allowed in most sectors of the economy. The legislation does not require mandatory involvement of local partners. This is especially relevant for companies wishing to retain full control over their structure and management.

- High Level of Investor Protection

Kazakhstan’s legal system guarantees equal rights to both local and foreign businessmen. International investment agreements apply, including treaties with the EAEU and OECD member countries. The country operates an Arbitration Court that ensures independent and transparent dispute resolution (including in Russian). Foreign companies can be protected from unjustified administrative interference.

- Ease of Business Registration

LLP registration can be completed electronically without the founder’s personal visit. However, personal presence is required for fingerprinting to obtain a business migrant temporary residence permit (a mandatory requirement before establishing a business), obtaining an Individual Identification Number (IIN), and opening a bank account.

- Flexible Requirements for Charter Capital

There is no minimum charter capital requirement for small companies. An LLP (Limited Liability Partnership) can be registered with a charter capital starting from 0 tenge for small and medium businesses. This makes business registration accessible and economically advantageous. - Attractive Tax System

Kazakhstan offers competitive tax conditions that make business more profitable.

- VAT – 12% (for domestic transactions and imports).

- 0% VAT on export trade within EAEU countries.

- Simplified tax regime (simplified declaration) – 3% of turnover for small businesses.

- General tax regime – 20% on profit, comparable or lower than in most regional countries.

- Tax incentives are available for companies operating in special economic zones (SEZs).

- Special Economic Zones (SEZs)

- Astana HUB for companies operating in information technology.

- International Financial Center for providing financial services.

- SEZs for enterprises specializing in manufacturing.

- Special economic zones offer preferential tax conditions for profile companies generating qualified income.

- E-Government

A unified platform for interaction with government authorities. Licensing, permits, and other documents can be processed online. Remote participation in court hearings. Quick access to all government services.

- Russian Language as a Working Tool

Russian is one of the official languages in Kazakhstan. Business documentation, negotiations, reports, and court proceedings can be conducted in Russian. This is especially convenient for entrepreneurs from CIS countries where Russian is the business lingua franca. It simplifies interaction with government bodies and local partners. - Access to Large Markets of the EAEU and Asia

Kazakhstan is a member of the Eurasian Economic Union (EAEU), providing access to the markets of:

- Russia,

- Belarus,

- Kyrgyzstan,

- Armenia.

- The country also borders China, enabling direct supplies and participation in Asian supply chains. This makes Kazakhstan an attractive platform for establishing international business. However, it is important to note that Kazakhstan does not position itself as a hub for international financial operations. Legislation and banking regulations focus on ensuring that financial flows correspond to goods transactions.

- Developed Banking System

Free execution of foreign currency transactions in compliance with currency legislation and financial monitoring requirements. A developed banking network with modern internet banking. Fast payments via mobile applications.

- Liberal Visa Regime

- Visa-free stay up to 90 days for citizens of EAEU countries.

- Simplified procedure for obtaining temporary residence permits (TRP) for foreign employees from EAEU countries planning to live and work in Kazakhstan permanently. No TRP is required if they do not intend to reside in Kazakhstan.

- Simplified TRP issuance for business migrants who are company participants. This requirement was introduced on May 28, 2024, obliging citizens of Russia, Belarus, and other EAEU countries wishing to open a business in Kazakhstan to obtain a TRP for business migrants.

- For individuals from other countries (e.g., EU, USA, China), the previous procedure remains – a business visa category C5 is required.

- Time Zone

Since March 1, 2024, Kazakhstan has adopted a single time zone (UTC+5). The time difference with Moscow is now +2 hours (previously, some regions had +3 hours).

Legal Forms of Business Organization

In the current economic environment of Kazakhstan, entrepreneurs are offered a wide range of legal forms for conducting business, each distinguished by its unique characteristics and benefits. Let’s explore the key options available for business owners to choose from.

Individual Entrepreneur (IE):

The IE is the simplest and most accessible way to organize entrepreneurial activity, particularly attractive for novice entrepreneurs and self-employed individuals. An IE can be registered electronically using the eGov service. The procedure takes from 5 to 15 minutes, significantly simplifying and speeding up the process of starting a business.

An IE bears full responsibility for obligations with personal property. However, this form has several advantages: minimal reporting requirements, the possibility to operate under a patent system, and no need for complex accounting. IE is an optimal choice for small businesses not aiming for significant expansion, but it is not the preferred option for innovative startups or enterprises associated with higher risks.

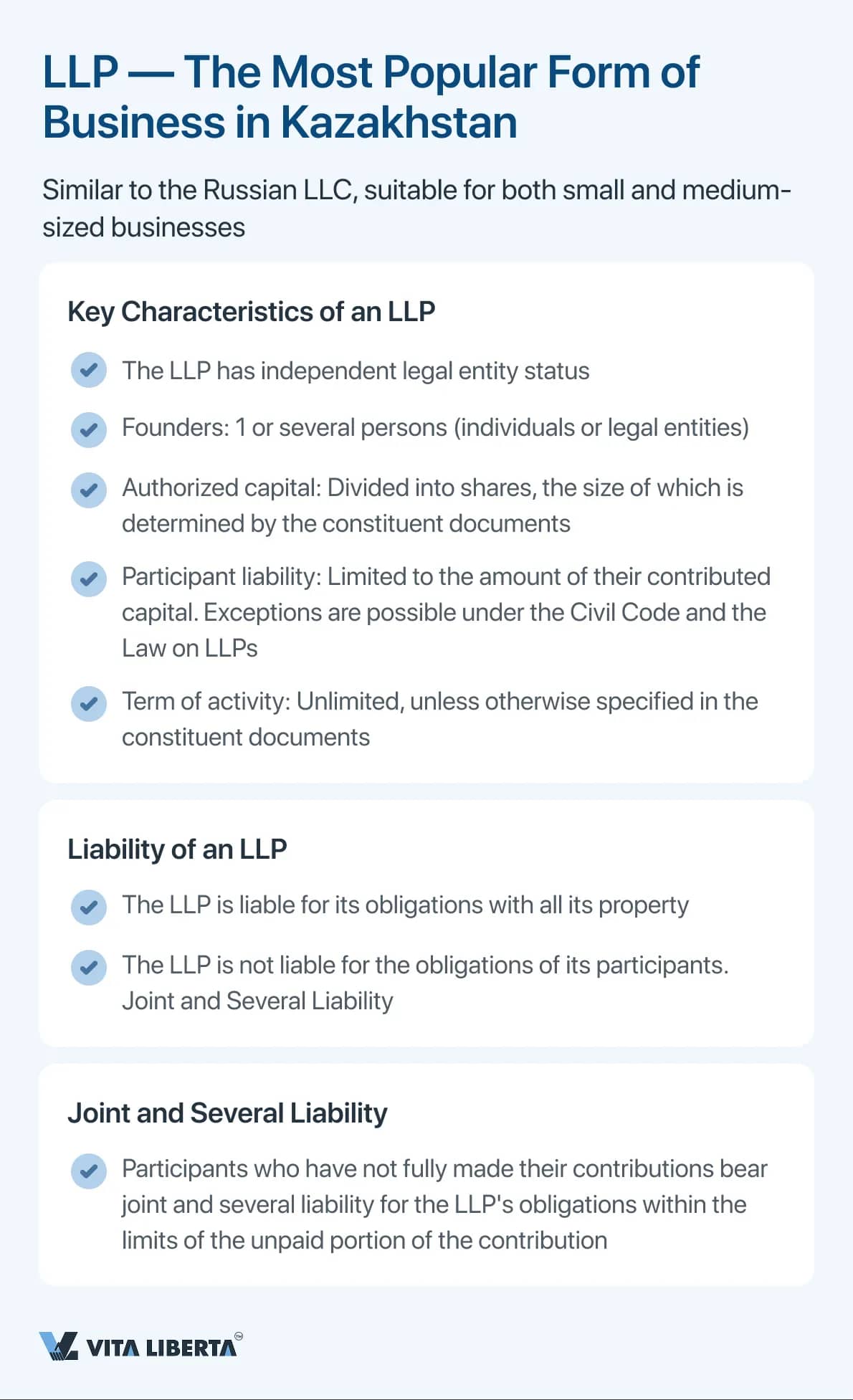

Limited Liability Partnership (LLP):

In Kazakhstan, the LLP is the most in-demand legal form for entrepreneurial activity. Essentially, it is similar to the Russian LLC and represents an optimal choice for both small and medium-sized enterprises.

An LLP is a legal entity established by one or more persons. The charter capital is divided into shares, the size of which is defined by the founding documents. Participants are liable for the LLP’s obligations only within the limits of their contributions. Exceptions are possible under the Civil Code and the LLP Law.

The LLP is considered established for an indefinite period unless otherwise specified in the founding documents. The LLP is a legal entity.

LLP Liability:

Individual Entrepreneur (IE):

The IE is the simplest and most accessible way to organize entrepreneurial activity, particularly attractive for novice entrepreneurs and self-employed individuals. An IE can be registered electronically using the eGov service. The procedure takes from 5 to 15 minutes, significantly simplifying and speeding up the process of starting a business.

An IE bears full responsibility for obligations with personal property. However, this form has several advantages: minimal reporting requirements, the possibility to operate under a patent system, and no need for complex accounting. IE is an optimal choice for small businesses not aiming for significant expansion, but it is not the preferred option for innovative startups or enterprises associated with higher risks.

Limited Liability Partnership (LLP):

In Kazakhstan, the LLP is the most in-demand legal form for entrepreneurial activity. Essentially, it is similar to the Russian LLC and represents an optimal choice for both small and medium-sized enterprises.

An LLP is a legal entity established by one or more persons. The charter capital is divided into shares, the size of which is defined by the founding documents. Participants are liable for the LLP’s obligations only within the limits of their contributions. Exceptions are possible under the Civil Code and the LLP Law.

The LLP is considered established for an indefinite period unless otherwise specified in the founding documents. The LLP is a legal entity.

LLP Liability:

- The LLP is liable for its obligations with all its property.

- The LLP is not liable for the obligations of its participants.

Joint Liability:

- Participants who have not fully contributed their shares to the charter capital bear joint liability for the LLP’s obligations within the limits of the unpaid part of the contribution.

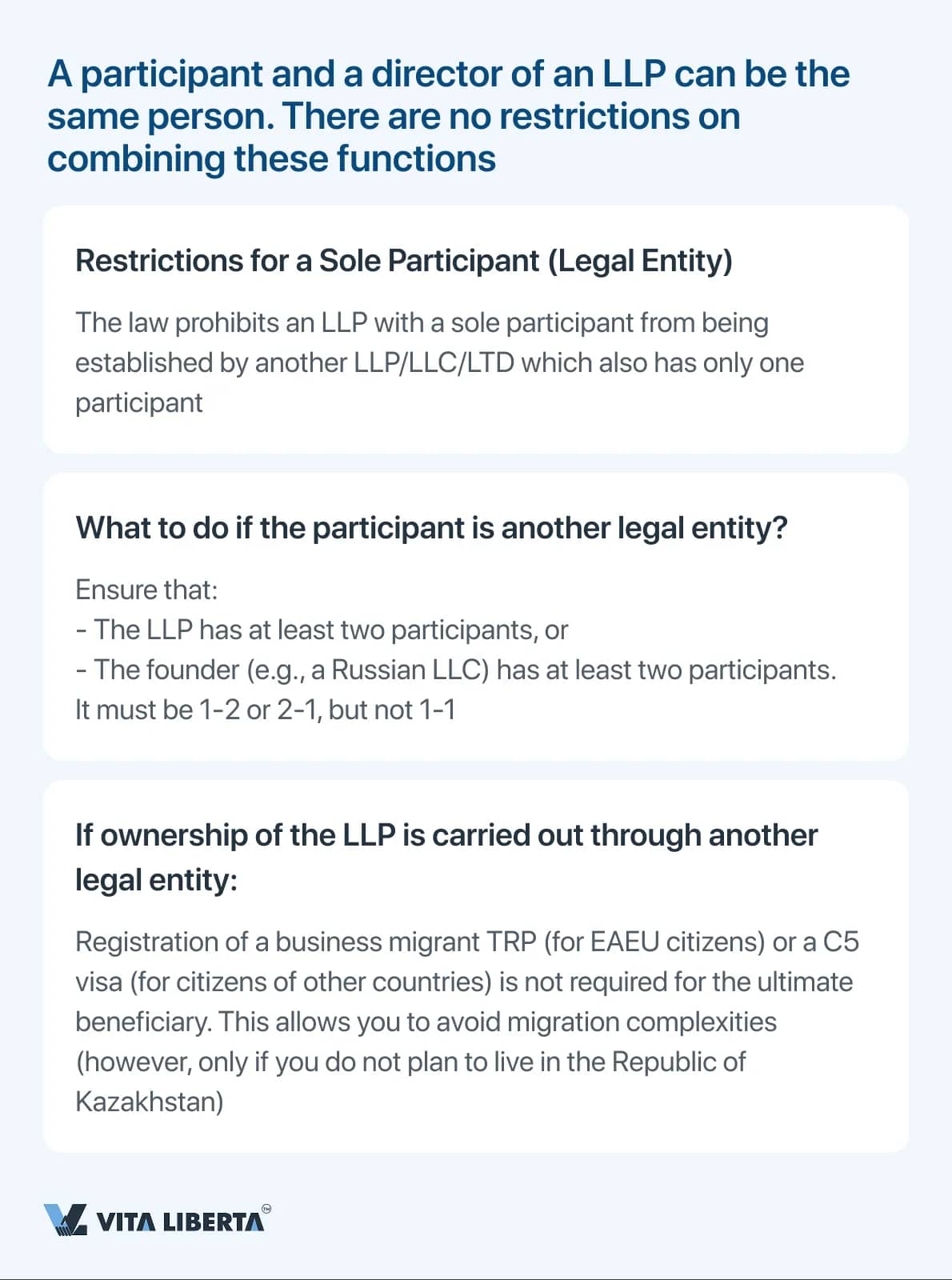

The same person can be both a participant and the director of an LLP; there are no restrictions in this regard. However, attention should be paid to restrictions related to a single participant if that participant is another legal entity. For example, the legislation of the Republic of Kazakhstan prohibits an LLP with a sole participant from being established by another business partnership that also has a single participant.

Example:

Example:

- An individual establishes LLP "B".

- LLP "B" becomes a participant in another LLP "A".

- If "A" has no other participants, such a structure is not permitted.

Therefore, if you plan to establish an LLP where another legal entity (for example, a Russian LLC) will be a participant, you need to ensure one of the following:

- The LLP has more than one participant;

- Or the LLC has more than one participant.

A significant advantage when registering an LLP with another legal entity as a participant is that the ultimate foreign beneficiary does not need to obtain a business migrant temporary residence permit (for EAEU citizens) or a C5 visa (for citizens of other countries).

If the LLP has a sole participant (individual or legal entity), then:

- All decisions usually made at the general meeting of participants are taken solely by this participant.

- Decisions are documented in writing (e.g., as an order or protocol in free form).

- There is no need to follow general meeting procedures (notifications, quorum, voting, etc.).

Joint Stock Company (JSC):

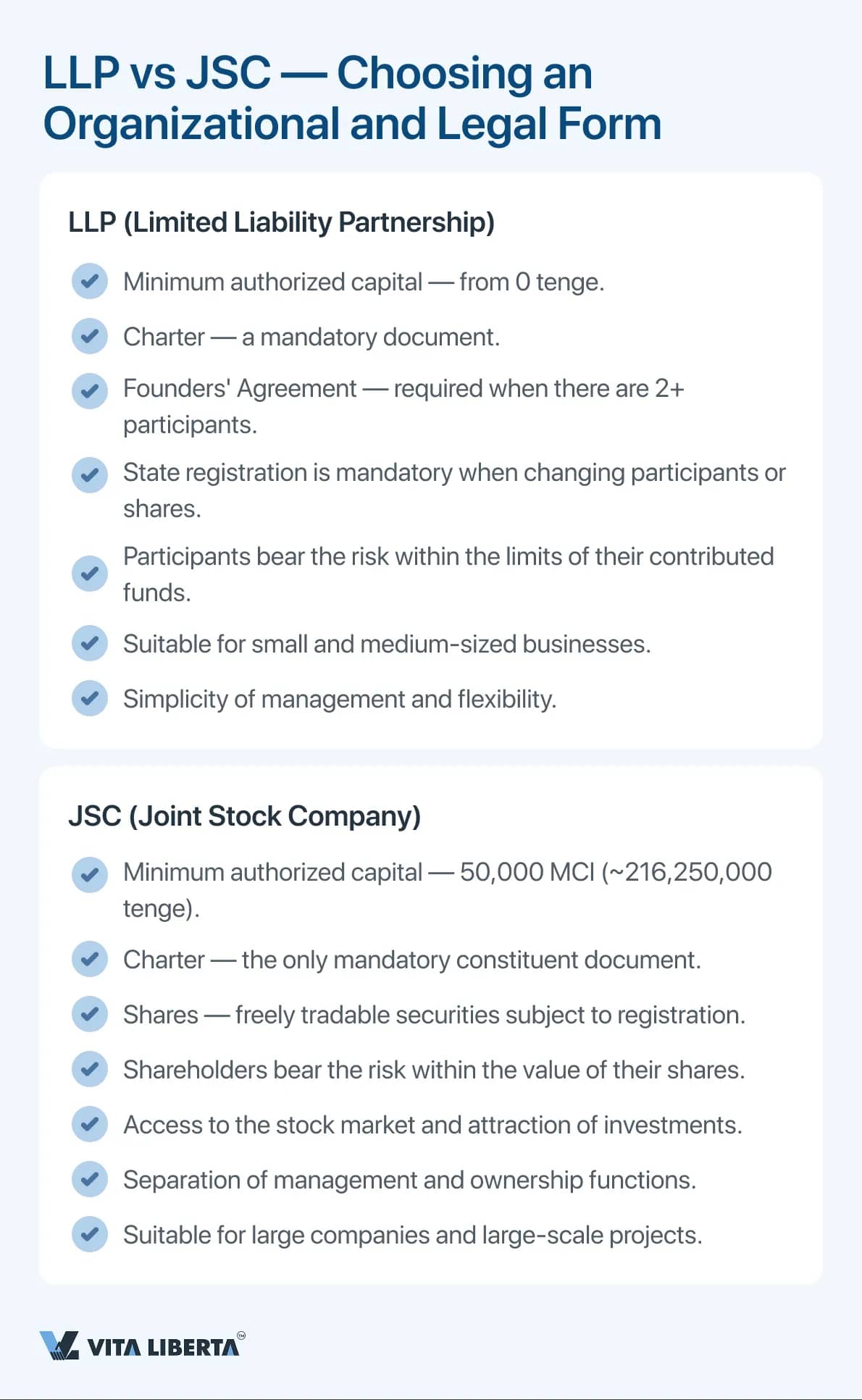

A JSC represents an optimal organizational form for large enterprises with a high level of financial potential. The company’s capital is formed by issuing securities, with owners risking only the amount equal to the price of their share package. The key advantage of this organizational structure is the clear separation of ownership and operational management functions, which is especially important in the development of large-scale commercial projects.

This form is characterized by a more labor-intensive registration process and increased reporting requirements, including mandatory audits and disclosure of financial data. At the same time, a JSC opens up opportunities to attract significant capital through share issuance and gain the status of a public company.

The main difference between an LLP (Limited Liability Partnership) and a JSC (Joint Stock Company) lies in the form of the charter capital:

This difference affects:

Minimum charter capital requirements also differ:

The set of founding documents for LLP and JSC has fundamental differences:

A JSC represents an optimal organizational form for large enterprises with a high level of financial potential. The company’s capital is formed by issuing securities, with owners risking only the amount equal to the price of their share package. The key advantage of this organizational structure is the clear separation of ownership and operational management functions, which is especially important in the development of large-scale commercial projects.

This form is characterized by a more labor-intensive registration process and increased reporting requirements, including mandatory audits and disclosure of financial data. At the same time, a JSC opens up opportunities to attract significant capital through share issuance and gain the status of a public company.

The main difference between an LLP (Limited Liability Partnership) and a JSC (Joint Stock Company) lies in the form of the charter capital:

- The charter capital of an LLP consists of shares that are not securities. Shares represent property rights of participants, and their issuance does not require registration with specialized authorities.

- The charter capital is divided into shares, which are subject to issuance and mandatory registration with the Agency for Regulation of the Financial Market (ARFM).

This difference affects:

- Complexity of establishment: creating a JSC requires compliance with securities market regulations.

- Management flexibility: LLP shares are not freely transferable, unlike JSC shares.

Minimum charter capital requirements also differ:

- The minimum charter capital is from 0 tenge, making this legal form accessible for small and medium businesses.

- JSC: The minimum charter capital is 50,000 minimum wage units (MWU), which currently amounts to approximately

The set of founding documents for LLP and JSC has fundamental differences:

LLP:

JSC:

The procedure for changing the composition of participants in LLP and JSC also differs in complexity and procedural burden:

- Charter — mandatory document.

- Founding agreement — required if there are two or more participants.

- The founding agreement may contain additional provisions regulating relations between participants.

JSC:

- Charter — the only mandatory founding document.

- Shareholder agreement is not provided by law but is allowed.

The procedure for changing the composition of participants in LLP and JSC also differs in complexity and procedural burden:

Any change in the composition of LLP participants or the size of shares requires:

- Amendments to the founding agreement;

- Adjustment of the charter;

- Submission of documents for state registration.

- All participants must sign the amendments, which may complicate prompt changes.

Changes in the composition of JSC shareholders are recorded in the shareholder register and do not require:

- Amendments to the charter;

- State registration;

- Consent of other shareholders (unless otherwise provided in the charter).

- Signing of the new version of the charter is done by an authorized person (e.g., the director).

The choice between LLP and JSC depends on several factors:

- Business scale and development plans;

- Number of founders and their structure;

- Investment attraction potential;

- Willingness to comply with corporate procedures;

- Plans to go public on the stock market.

Branches and Representative Offices:

Foreign companies can operate in Kazakhstan by opening branches and representative offices.

Branch is a separate structural unit with extended authority. This form allows not only representing the interests of the parent company but also conducting the main type of the organization’s activity. The branch has the right to:

Foreign companies can operate in Kazakhstan by opening branches and representative offices.

Branch is a separate structural unit with extended authority. This form allows not only representing the interests of the parent company but also conducting the main type of the organization’s activity. The branch has the right to:

- Conclude commercial contracts;

- Represent the company before government authorities;

- Conduct full operational activities.

- Representing the interests of the parent organization;

- Information and consulting activities;

- Maintaining business contacts.

Advantages of LLP

Since an LLP is the most common legal form for company registration in Kazakhstan, let us take a broader look at the advantages and disadvantages of this type of legal entity.

Reasons why an LLP is a beneficial choice:

Financial Security of Participants:

Limited liability of participants is one of the main advantages of the LLP legal form. This feature significantly distinguishes a partnership from the status of an individual entrepreneur, where the business owner bears full personal liability for obligations.

In the case of an LLP, the founders are legally protected: their liability is strictly limited to the amount of invested capital. This means that in the event of financial difficulties or debts to creditors, the personal assets of the participants remain untouchable.

This system creates an important financial buffer that:

Reasons why an LLP is a beneficial choice:

Financial Security of Participants:

Limited liability of participants is one of the main advantages of the LLP legal form. This feature significantly distinguishes a partnership from the status of an individual entrepreneur, where the business owner bears full personal liability for obligations.

In the case of an LLP, the founders are legally protected: their liability is strictly limited to the amount of invested capital. This means that in the event of financial difficulties or debts to creditors, the personal assets of the participants remain untouchable.

This system creates an important financial buffer that:

- Protects founders' personal assets from seizure;

- Minimizes entrepreneurial risks;

- Increases the attractiveness of the LLP form for investors;

- Allows for more confident business development;

- Contributes to company stability.

However, it is important to keep in mind that Kazakhstan has a subsidiary liability form. According to Kazakh legislation, the bankruptcy procedure is aimed at protecting creditors' interests and ensuring their satisfaction from the debtor’s assets. However, if the assets are insufficient, the law provides for the possibility of holding founders, participants, or company officials additionally (subsidiary liability). This applies in cases where such persons are guilty of intentional bankruptcy or violated legal requirements, leading to the deterioration of the company's financial condition. The Civil Code and the Law “On Rehabilitation and Bankruptcy” establish that if a legal entity lacks sufficient funds after the bankruptcy procedure is completed, the founders and officials may be held liable to creditors. Such liability arises if they are found guilty within administrative or criminal proceedings.

Moreover, officials bear joint subsidiary liability if they:

- Did not apply to the court for recognition of the debtor as bankrupt when a liquidation decision was made and the assets were insufficient to fully satisfy creditors' claims;

- Did not provide necessary information about the financial and economic activities of the company;

- Did not transfer documents, accounting and title documents, as well as the debtor’s property to the temporary manager.

The bankruptcy manager is obliged within 10 working days after the court decision on bringing a person to administrative or criminal liability comes into force to file a subsidiary liability claim. The creditor also has the right to file a claim in a similar manner if the fault of the founder or official was established after the completion of the bankruptcy procedure.

The amount of claims made against a person under subsidiary liability is determined by the court decision based on the established fault.

It is important to note that funds received into the asset mass as a result of subsidiary liability decisions cannot be used to cover administrative expenses. All proceeds are directed to satisfy creditors' claims.

Partnership Potential

An LLP provides broad opportunities for implementing joint business initiatives. This form allows combining the efforts of an unlimited number of partners, which is especially important when launching large-scale projects or entering new markets. Such cooperation enables effective distribution of responsibilities, pooling of resources and competencies of participants to achieve common goals.

Prestige and Trust

An LLP is traditionally perceived as more solid and reliable compared to individual entrepreneurship. This creates an additional competitive advantage when interacting with partners, clients, and suppliers, who often prefer legal entities.

Flexibility of Transformation

Partnership Potential

An LLP provides broad opportunities for implementing joint business initiatives. This form allows combining the efforts of an unlimited number of partners, which is especially important when launching large-scale projects or entering new markets. Such cooperation enables effective distribution of responsibilities, pooling of resources and competencies of participants to achieve common goals.

Prestige and Trust

An LLP is traditionally perceived as more solid and reliable compared to individual entrepreneurship. This creates an additional competitive advantage when interacting with partners, clients, and suppliers, who often prefer legal entities.

Flexibility of Transformation

An LLP has significant potential to adapt to changing market conditions. The company can be transformed into other forms of legal entities, for example, a joint-stock company, which is especially relevant with substantial business growth. Additionally, legislation provides for the possibility of conducting complex corporate procedures: mergers, spin-offs, accession, and division, allowing flexible responses to market challenges.

Business Integrity upon Sale

Business Integrity upon Sale

An important advantage of an LLP is the possibility to sell the business as a whole. Such a transaction transfers not only the company’s property but also the established client base, developed reputation, and business relationships. For clients, the change of ownership remains unnoticed, which helps maintain stability of business processes and continue operations without loss of counterparties’ trust.

Thus, an LLP is a universal and flexible form of doing business, combining financial security, partnership opportunities, growth and development potential, as well as prestige in the business community.

Thus, an LLP is a universal and flexible form of doing business, combining financial security, partnership opportunities, growth and development potential, as well as prestige in the business community.

Step-by-Step Guide to Registering an LLP in Kazakhstan

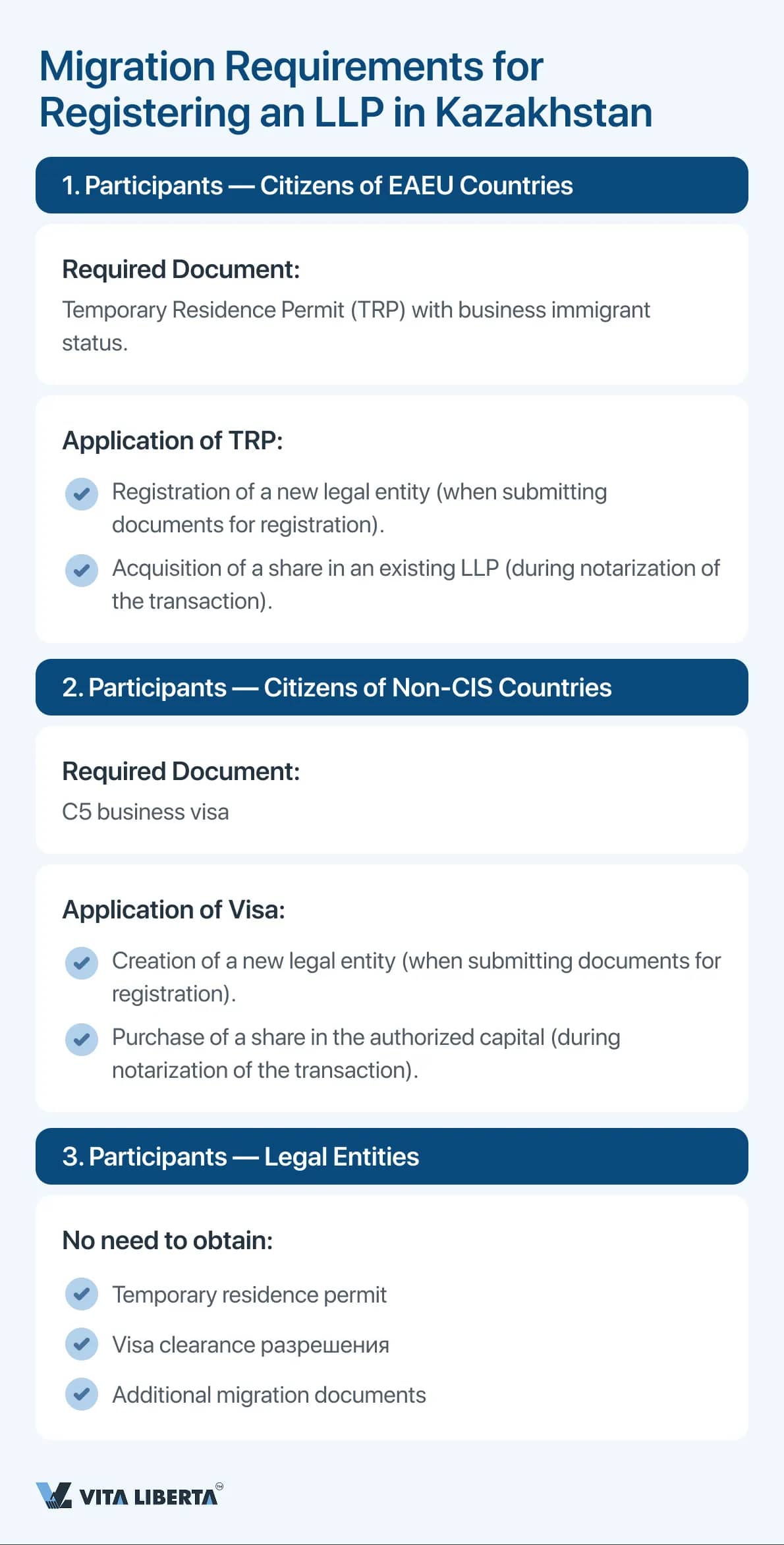

Step 1: Obtaining a Migration Permit for LLP Founders

Residents who plan to open or become participants in an LLP in Kazakhstan must undergo the procedure for obtaining a special migration permit.

Citizens of EAEU Countries

Entrepreneurs from countries that are members of the Eurasian Economic Union (including Russia, Belarus, Armenia, Uzbekistan, and Kyrgyzstan) and have visa-free agreements with Kazakhstan must obtain a temporary residence permit (TRP) as business migrants. This document allows them to stay in Kazakhstan without a visa and conduct entrepreneurial activities.

Citizens of Other Countries

For businessmen from countries not belonging to the Eurasian Economic Union, a business visa of category C5 is required. This document is necessary in the following cases:

Residents who plan to open or become participants in an LLP in Kazakhstan must undergo the procedure for obtaining a special migration permit.

Citizens of EAEU Countries

Entrepreneurs from countries that are members of the Eurasian Economic Union (including Russia, Belarus, Armenia, Uzbekistan, and Kyrgyzstan) and have visa-free agreements with Kazakhstan must obtain a temporary residence permit (TRP) as business migrants. This document allows them to stay in Kazakhstan without a visa and conduct entrepreneurial activities.

Citizens of Other Countries

For businessmen from countries not belonging to the Eurasian Economic Union, a business visa of category C5 is required. This document is necessary in the following cases:

- When establishing a new company – the visa must be obtained in advance before submitting registration documents to the authorized bodies.

- When purchasing a share in an existing enterprise – the visa is required at the stage of notarizing the transaction and when submitting documents for changes to the company registry.

Without this visa, carrying out these operations with legal entities within the country is impossible.

Foreign Legal Entities

When establishing an LLP by a foreign legal entity, regardless of its country of origin, obtaining a TRP or C5 visa is not required.

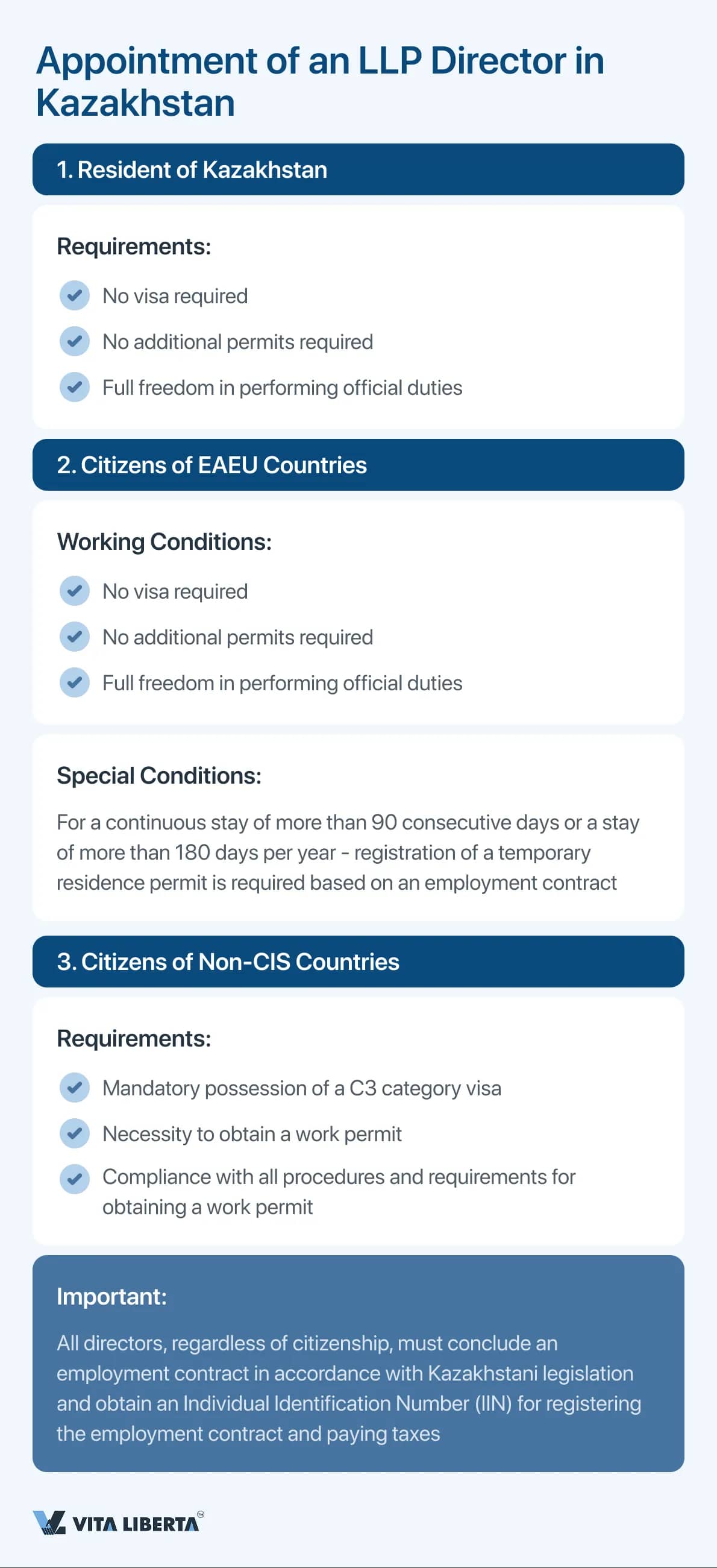

Step 2: Appointment of the LLP Director

When registering an LLP in Kazakhstan, it is necessary to appoint a company director. The document requirements depend on the citizenship of the appointed director.

Director – Citizen of Kazakhstan

When appointing a Kazakhstani citizen as director, no additional permits or visas are required. The director can fully exercise their powers without any restrictions.

Director from EAEU Countries

Citizens of Eurasian Economic Union countries have a special legal status when managing Kazakhstani companies. They can hold the position of director without additional approval from labor and migration authorities regarding the involvement of foreign specialists. They exercise their managerial powers fully without restrictions.

However, if a prolonged stay in Kazakhstan is planned (more than 90 consecutive days or more than 180 days in total per calendar year), it is necessary to obtain a temporary residence permit. The basis for its issuance is a concluded employment contract. The TRP acquisition process is significantly simplified if a complete set of correctly prepared documents is submitted, allowing the processing time to be minimized.

Director from Other Countries

For citizens of countries outside the EAEU planning to take the position of LLP director, a visa of category "C3" is required. This visa is intended for foreign specialists arriving in Kazakhstan to perform labor activities, including their family members (except citizens of EAEU countries). Holding a "C3" visa grants a foreign citizen the legal opportunity to work in the country, but only if all necessary conditions are met and a work permit is obtained according to the established procedure.

When registering an LLP in Kazakhstan, it is necessary to appoint a company director. The document requirements depend on the citizenship of the appointed director.

Director – Citizen of Kazakhstan

When appointing a Kazakhstani citizen as director, no additional permits or visas are required. The director can fully exercise their powers without any restrictions.

Director from EAEU Countries

Citizens of Eurasian Economic Union countries have a special legal status when managing Kazakhstani companies. They can hold the position of director without additional approval from labor and migration authorities regarding the involvement of foreign specialists. They exercise their managerial powers fully without restrictions.

However, if a prolonged stay in Kazakhstan is planned (more than 90 consecutive days or more than 180 days in total per calendar year), it is necessary to obtain a temporary residence permit. The basis for its issuance is a concluded employment contract. The TRP acquisition process is significantly simplified if a complete set of correctly prepared documents is submitted, allowing the processing time to be minimized.

Director from Other Countries

For citizens of countries outside the EAEU planning to take the position of LLP director, a visa of category "C3" is required. This visa is intended for foreign specialists arriving in Kazakhstan to perform labor activities, including their family members (except citizens of EAEU countries). Holding a "C3" visa grants a foreign citizen the legal opportunity to work in the country, but only if all necessary conditions are met and a work permit is obtained according to the established procedure.

Step 3: Preparation of the Document Package

Successful registration of a legal entity with foreign capital in Kazakhstan requires a specific set of documents.

For individuals acting as founders, the following are required:

Successful registration of a legal entity with foreign capital in Kazakhstan requires a specific set of documents.

For individuals acting as founders, the following are required:

- Proof of identity: a copy of the foreign passport or other identity document of the foreign founder, with mandatory notarized translation into Kazakh and Russian.

- Documents related to migration status: a temporary residence permit in Kazakhstan or, if necessary, the corresponding business visa, as well as a document granting the right to conduct entrepreneurial activity in Kazakhstan.

- A notarized power of attorney (if registration is carried out through a representative) confirming the authority of the proxy.

- Individual Identification Number (IIN), mandatory for all participants including the director, as a unique identifier for interaction with government bodies.

For legal entity participants, the following are required:

- Business Identification Number (BIN) – a unique code for identifying the legal entity, necessary for registration actions.

- A notarized power of attorney from the legal entity confirming the right to register the LLP and certifying the representative’s authority.

- An extract from the commercial register of the country of registration confirming the legal status of the company, with notarized translations into Kazakh and Russian.

Important to remember: All documents must be properly executed, legalized or apostilled, and provided in originals or notarized copies. Documents not in Russian require notarized translation. Compliance with all requirements is the key to successful registration.

Step 4: Obtaining Identification Numbers

During the registration process of a business with foreign participation in Kazakhstan, each applicant must obtain the corresponding identification code depending on their legal status.

IIN is intended for individuals, both residents and non-residents of the country. This unique code is a key element when interacting with Kazakhstan's government bodies. The Individual Identification Number allows access to many government services, including:

- Issuance of documents for temporary stay in the country;

- Registration of a company or enterprise in the prescribed manner;

- Opening a bank account;

- Obtaining employment and official registration;

- Using electronic platforms for interaction with government bodies.

To obtain an IIN, a foreign citizen must:

- Appear in person at the Public Service Center (PSC) under the JSC "Government for Citizens";

- Present a valid foreign passport;

- Provide a notarized translation of the passport (if necessary);

- Processing takes from one to two working days. The service is free of charge;

- After obtaining the IIN, access to the "Mobile Citizens" database and electronic digital signature (EDS) issuance is enabled.

To obtain a BIN, a foreign organization must prepare the following documents:

- Company founding documents;

- Proof of registration in the country of origin (certificate of state and tax registration);

- Current extract from the commercial register (in two copies);

- Foreign passports of founders and director with translation into Kazakh;

- IIN of the company director;

- Notarized power of attorney for LLP registration.

All documents must be:

- Notarized;

- Apostilled or legalized according to the legislation of the country where the company is registered;

- Translated into Russian with notarized translation (if originally in another language).

Step 5: Registration in the Mobile Citizens Database (MCB)

After successfully obtaining the IIN at the Public Service Center, access opens to the next important step – registration in the Mobile Citizens Database (MCB). This is a necessary step for full use of Kazakhstan's government online services, including obtaining an electronic digital signature (EDS).

Mobile Citizens Database is a centralized system playing a key role in the country's electronic document flow. It stores current mobile phone numbers of citizens, allowing:

- Receiving SMS passwords for multi-factor authentication;

- Using one-time passwords when logging into government portals;

- Receiving proactive and composite government services;

- Accessing the electronic government portal.

Registration process in the MCB for non-residents requires:

- A mobile phone capable of receiving SMS;

- A local operator's phone number;

- A SIM card activated for the first time on the territory of Kazakhstan.

It is important to note that after initial activation of the SIM card in Kazakhstan, it will be able to receive SMS messages anywhere in the world where cellular service is available. Without registration in the MCB, access to most government online services will be limited, significantly complicating interaction with government bodies and obtaining necessary services electronically.

Registration in the MCB is a mandatory condition for full use of all electronic government capabilities in Kazakhstan, including document submission, obtaining certificates, and performing other administrative procedures online.

Step 6: Electronic Digital Signature (EDS)

Electronic Digital Signature is a modern digital tool that is a full legal equivalent of a traditional handwritten signature. It is a unique set of digital symbols ensuring legal validity when signing documents electronically.

EDS Structure includes two separate files with individual symbol sets. These files can be stored on various media:

- Personal computer;

- Smartphone;

- Tablet;

- USB drive.

EDS files can be transmitted via:

- Email;

- Messengers;

- Other digital communication channels.

The legal basis for the use of EDS is established at the state level in accordance with the Law of the Republic of Kazakhstan "On Electronic Document and Electronic Digital Signature". This legislative act states that electronic documents certified by EDS have identical legal force compared to documents signed manually on paper. This provision ensures the equivalence of electronic and traditional document flow in the country's legal field.

Prerequisite for obtaining an EDS is having an IIN. Only after obtaining it is it possible to issue an electronic digital signature, which becomes a key tool for:

- Interaction with government bodies;

- Signing business documents;

- Using electronic government services;

- Conducting electronic business correspondence.

EDS significantly simplifies document flow and makes it more efficient, allowing legally significant actions to be performed in digital form.

Step 7: Determining the Business Entity Status

When registering an LLP, it is necessary to determine the business size according to established criteria:

Small Business is characterized by:

- Up to 50 employees;

- Assets not exceeding 60,000 MCI.

Medium Business is defined by:

- From 51 to 250 employees;

- Assets up to 325,000 MCI.

Large Business includes:

- More than 250 employees;

- Assets exceeding 325,000 MCI.

It is important to consider that the Monthly Calculation Index (MCI) for 2025 is 3,932 tenge and is used for calculating various social payments and tax obligations.

Step 8: Determining the Size of the Charter Capital

LLP Charter Capital is the initial capital of the company formed from the founders' contributions. It serves as:

LLP Charter Capital is the initial capital of the company formed from the founders' contributions. It serves as:

- The basis for starting activities;

- A guarantee for fulfilling obligations to creditors;

- A means for initial expenses (rent, equipment, prepayment).

Minimum requirements for charter capital:

- For small business – from 0 tenge;

- For medium and large business – 100 MCI (393,200 tenge).

Practical recommendations:

- To minimize costs – from 0 tenge;

- To cover first month’s rent expenses – 100,000 - 250,000 tenge;

- When planning large contracts – the size should correspond to the scale of activities.

Important Note:

- The charter capital is contributed by the founders, not the director;

- The funds must be contributed within one year after registration;

- It is necessary to plan the mechanism for contribution in advance if the founders do not intend to visit the bank personally.

Step 9: Choosing the LLP Name

LLP Name must meet the following requirements:

LLP Name must meet the following requirements:

- Be unique (not identical to existing companies);

- Not cause legal conflicts;

- Avoid confusion with other brands.

When choosing a name, it is recommended to:

Check its uniqueness through special services;

Consider features of the Kazakh language (if planning to use a Kazakh name);

Think about international recognition (if planning to operate in the international market);

Check its uniqueness through special services;

Consider features of the Kazakh language (if planning to use a Kazakh name);

Think about international recognition (if planning to operate in the international market);

Ensure there are no registered trademarks with the same name.

Step 10: Selecting LLP Activities (OKED). In Kazakhstan, entrepreneurs have wide opportunities to conduct business, as they can engage in any activities not prohibited by law. This allows flexible response to market changes and expansion of the company's scope.

Step 11: Preparing Founding Documents

For a sole founder, it is necessary to prepare:

Step 11: Preparing Founding Documents

For a sole founder, it is necessary to prepare:

- A decision of the sole participant on establishment;

- An order appointing the General Director.

For multiple founders, the following are required:

- Minutes of the general meeting of founders;

- Founding agreement;

- Order appointing the General Director.

All documents must be printed, signed, and sealed. Regardless of the number of founders, it is necessary to develop and approve the LLP charter using the standard form.

Step 12: Submitting Documents to the Registrar

After preparing all necessary documents and information, they must be submitted to the registrar to complete the LLP registration process.

Step 13: Making the LLP Seal. In modern business conditions, many entrepreneurs question the necessity of making a seal for the LLP. Legislation has undergone significant changes, and today having a seal is not mandatory for registration and operation of a legal entity.

Legal Basis. According to current legislation, an LLP can operate without a seal. This provision is enshrined in normative acts, giving companies the right to independently decide on the need to make a seal.

Practical Aspects. Despite being optional, a seal may be required in the following cases:

Step 12: Submitting Documents to the Registrar

After preparing all necessary documents and information, they must be submitted to the registrar to complete the LLP registration process.

Step 13: Making the LLP Seal. In modern business conditions, many entrepreneurs question the necessity of making a seal for the LLP. Legislation has undergone significant changes, and today having a seal is not mandatory for registration and operation of a legal entity.

Legal Basis. According to current legislation, an LLP can operate without a seal. This provision is enshrined in normative acts, giving companies the right to independently decide on the need to make a seal.

Practical Aspects. Despite being optional, a seal may be required in the following cases:

- Interaction with government bodies

- Signing contracts with certain counterparties;

- Opening a bank account in certain financial institutions;

- Participation in government procurement.

Recommendations for Use

If there is no seal, it is necessary to:

- Indicate in the founding documents that the organization operates without a seal;

- Use the director’s facsimile signature;

- Stamp documents with “No Seal”;

- Maintain a log of outgoing documents.

Advantages of Not Having a Seal

- Savings on seal production and maintenance;

- Simplification of document flow;

- Reduced risk of losing the seal;

- Possibility of electronic signature.

Thus, the decision on whether to have a seal for the LLP remains at the discretion of the company’s management. It is important to consider the specifics of the activity and the requirements of counterparties with whom the company will interact. In any case, the absence of a seal is not an obstacle to the full operation of the legal entity.

Step 14: Obtaining an EDS for the Director.

An electronic digital signature for a legal entity is the digital equivalent of the director’s personal signature. It is a single file that gives electronic documents the same legal force as a signature and seal on paper documents.

Step 14: Obtaining an EDS for the Director.

An electronic digital signature for a legal entity is the digital equivalent of the director’s personal signature. It is a single file that gives electronic documents the same legal force as a signature and seal on paper documents.

Step 15: Formalizing the Director. After registering the LLP, it is necessary to officially employ the General Director:

- Conclude an employment contract;

- Issue an order on employment;

- Register the employment contract on the electronic employment contracts portal within three days.

Step 16: Opening Bank Accounts

It is necessary to open:

- An account for the company’s operational activities;

- An account for paying the director’s salary.

Step 17: Employer Liability Insurance.

After the director’s official employment, it is mandatory to arrange employer liability insurance. This is a legal requirement that helps avoid fines and legal issues.

Step 18: Obtaining Licenses and Notifying the Akimat.

If the company’s activity requires licensing, it is necessary to:

- Obtain the relevant licenses;

- Submit a notification to the Akimat about the start of activities.

Step 19: Installing a POS Terminal. For some types of activities, having a POS terminal – a device for cashless payments – is required. Installing such equipment not only meets modern requirements but also enhances customer service convenience, which can become a competitive advantage for the business.

Tax System for LLPs in Kazakhstan

When organizing a business in Kazakhstan, it is important to consider the tax burden. Let's look at the main tax obligations for an LLP.

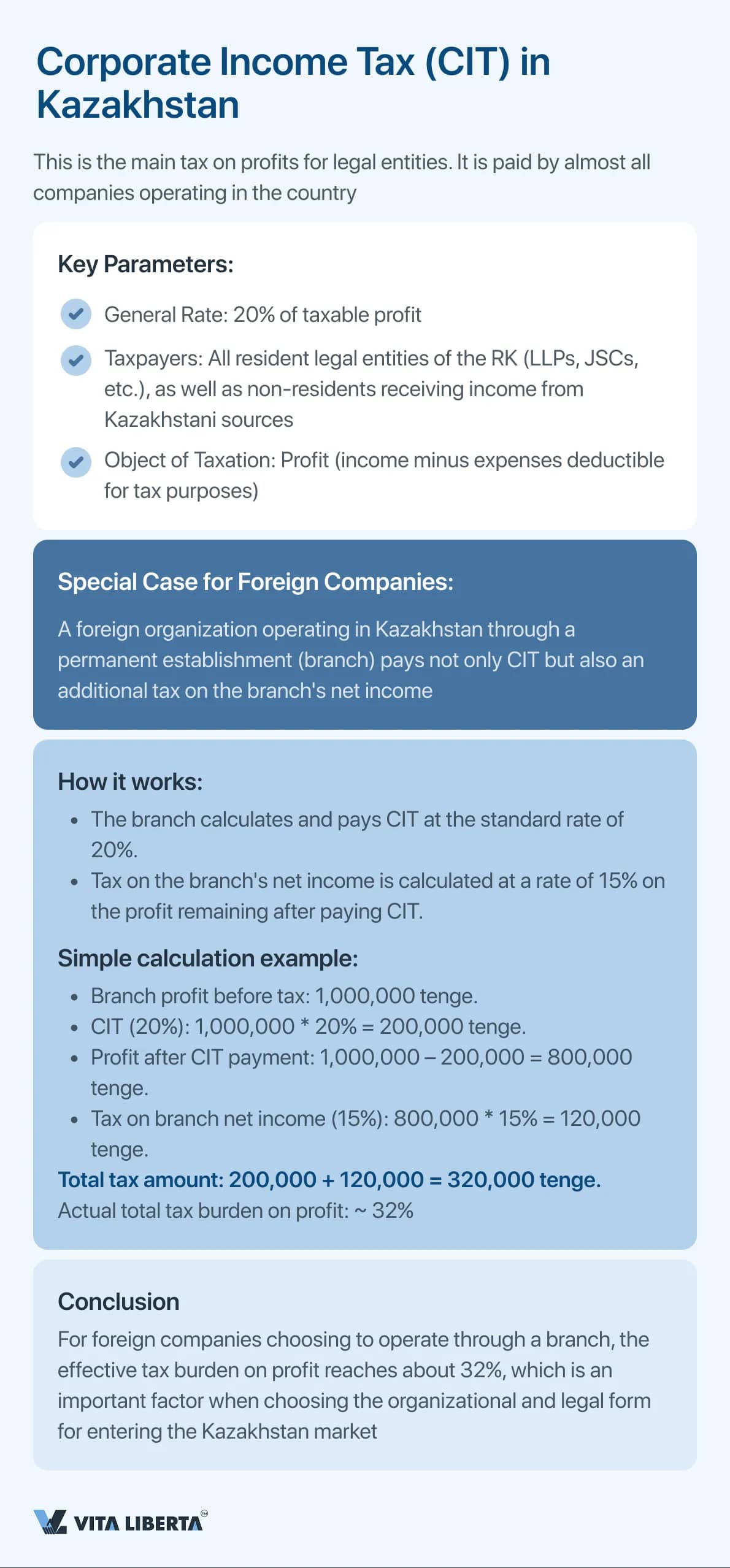

Corporate Income Tax in Kazakhstan

One of the key taxes faced by legal entities in Kazakhstan is corporate income tax. The general rate of this tax is 20%.

This levy is collected on the profits of organizations of all forms of ownership - from LLPs and Additional Liability Partnerships to Joint-Stock Companies. It is paid by both residents and non-residents if they carry out activities in Kazakhstan through a permanent establishment or receive income from sources located within the country.

- It is important to note that foreign companies with a permanent establishment in Kazakhstan, in addition to corporate income tax, must pay a tax on the net income of branches, which is 15% of the remaining amount after paying corporate income tax.

One such regime is the simplified taxation system.

Under this scheme, entrepreneurs pay only 4% of the income received for a six-month period. This regime, known as the "simplified regime," is designed to significantly reduce the administrative and financial burden on entrepreneurs. However, its application is strictly regulated and not available to everyone.

The Essence of the Regime and Key Advantages

Taxpayers who choose the Special Tax Regime based on a simplified declaration receive a number of significant preferences:

- Single Payment: A single aggregate payment is made, replacing corporate or individual income tax. The rate is 4% of the semi-annual income amount.

- Exemption from Key Taxes: Enterprises under this regime are not payers of social tax or value added tax (VAT).

- Exception for VAT: An important clarification — the VAT exemption does not apply to import operations. VAT on the import of goods into the territory of the Republic of Kazakhstan is paid in the generally established manner.

The right to apply the regime is available to both individual entrepreneurs and resident legal entities of Kazakhstan, subject to the simultaneous fulfillment of three criteria:

- Income Limit: The total annual income must not exceed 600,000 MCI. Considering the MCI amount in 2026 (4,235 tenge), this is 2.541 billion tenge.

- Permitted Types of Activities: The company must carry out types of activities that are not included in the prohibited list approved by the Government of the Republic of Kazakhstan.

- "Purity" of the Business Structure: A number of restrictions are related to the corporate structure:

- The share of participation of other legal entities in the authorized capital must not exceed 25%.

- The founders/participants of the company themselves must not apply the SRT or be founders in another company on the "simplified regime."

The regime is not available to non-profit organizations, residents of special economic zones, and participants in joint activity agreements.

The Government has approved a list of 44 types of economic activities (according to OKED) for which the use of the simplified declaration is prohibited. This list traditionally includes:

- Activities in the financial and insurance sector.

- Extraction of crude oil and natural gas.

- Production of excisable goods.

- Trade in precious metals and stones.

- Auditing and legal practice.

- Gambling business.

Before switching to the SRT, it is critically important to check your OKED codes against the current prohibited list.

The tax period for calculating the single aggregate payment is six months. This means that the tax calculation and submission of the simplified declaration are done twice a year, which reduces the volume of regular reporting.

SME Support Measures from 2026

As part of further debureaucratization, additional guarantees are provided for conscientious taxpayers under the SRT:

- Limitation of Tax Audits: A moratorium has been introduced on conducting scheduled documentary and on-site tax audits on compliance with tax legislation.

- Simplified Tax Control: The grounds for unscheduled control have been significantly narrowed, creating more stable and predictable conditions for doing business.

Abolition of Tax Regimes from 01/01/2026 in Kazakhstan

From January 1, 2026, large-scale changes to the system of special tax regimes in Kazakhstan came into force, aimed at its unification and simplification. As part of the tax reform, four previously existing special regimes were completely abolished:

Entrepreneurs who applied the abolished SRTs needed to switch to another valid tax regime (in most cases — to the SRT based on a simplified declaration or the generally established procedure) before January 1, 2026, and adapt their accounting and tax records to the new rules.

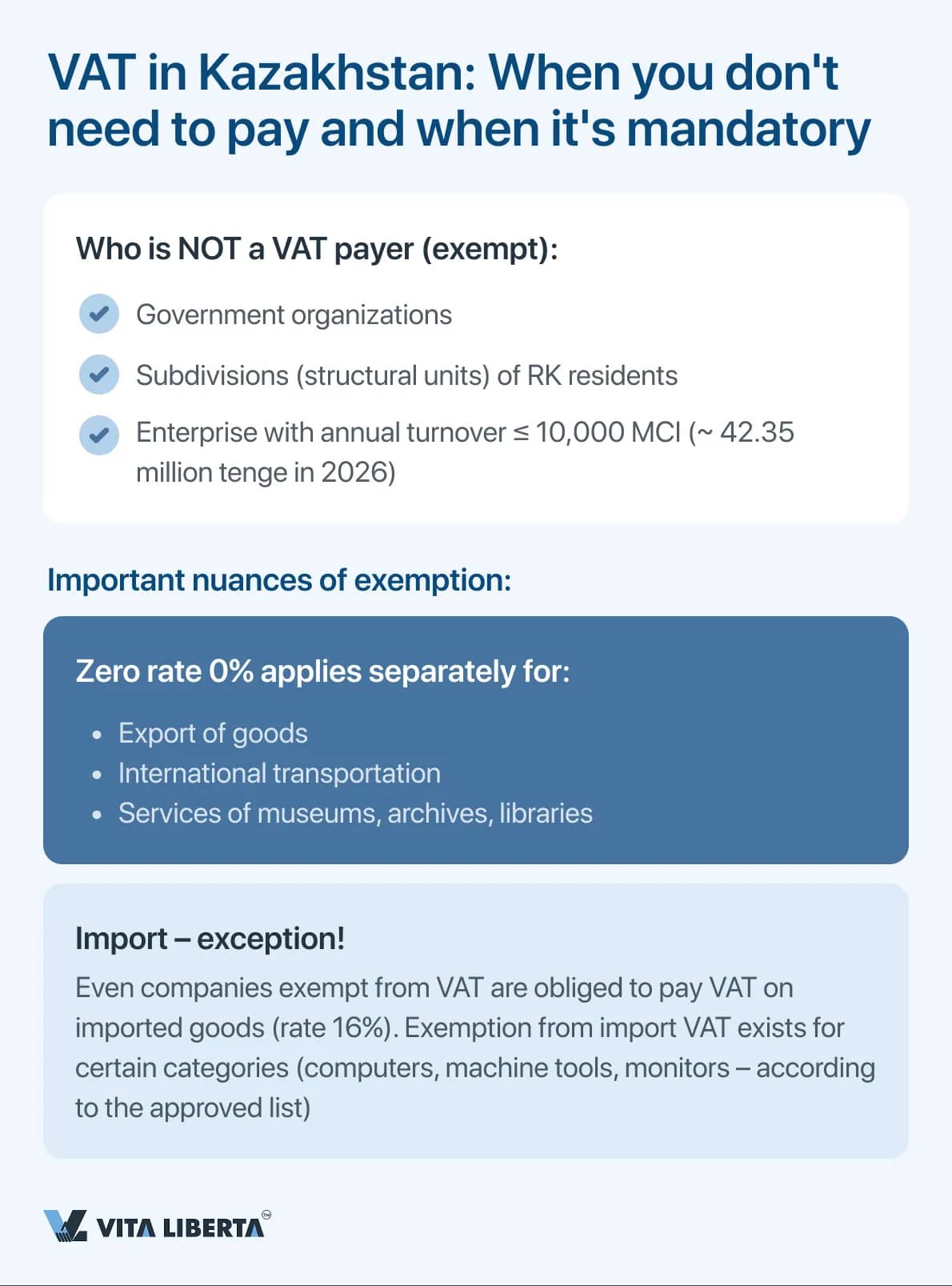

Value Added Tax (VAT) in Kazakhstan

One of the factors contributing to business development in Kazakhstan is the relatively low value-added tax rate - 16%. This favorably distinguishes Kazakhstan from countries such as Belarus (25%) and Russia (22%).

However, it is important to consider that not all participants in economic activity are required to pay VAT. For example, tax is not levied on:

Important: even if an organization is not registered as a VAT payer, it is still obliged to pay tax when importing goods. At the same time, some categories of imported goods are exempt from VAT - these include, for example, computer equipment, color monitors, storage devices, and certain types of machine tools.

Value Added Tax is paid four times a year, i.e., quarterly.

All businesses whose turnover exceeds 10,000 MCI must be registered for VAT. This rule applies regardless of whether the company applies the general tax regime or a special tax regime.

From January 1, 2026, large-scale changes to the system of special tax regimes in Kazakhstan came into force, aimed at its unification and simplification. As part of the tax reform, four previously existing special regimes were completely abolished:

- SRT using a fixed deduction — a regime that allowed applying a fixed deduction to income.

- SRT of retail tax — a special regime for retail trade entities.

- SRT based on a patent — a taxation system based on purchasing a patent for certain types of activities.

- SRT using a mobile application — an experimental digital regime for micro-businesses.

Entrepreneurs who applied the abolished SRTs needed to switch to another valid tax regime (in most cases — to the SRT based on a simplified declaration or the generally established procedure) before January 1, 2026, and adapt their accounting and tax records to the new rules.

Value Added Tax (VAT) in Kazakhstan

One of the factors contributing to business development in Kazakhstan is the relatively low value-added tax rate - 16%. This favorably distinguishes Kazakhstan from countries such as Belarus (25%) and Russia (22%).

However, it is important to consider that not all participants in economic activity are required to pay VAT. For example, tax is not levied on:

- government organizations;

- subdivisions of residents;

- enterprises whose annual turnover does not exceed 10,000 monthly calculation indices (MCI).

- enterprises applying the special tax regime based on a simplified declaration.

Important: even if an organization is not registered as a VAT payer, it is still obliged to pay tax when importing goods. At the same time, some categories of imported goods are exempt from VAT - these include, for example, computer equipment, color monitors, storage devices, and certain types of machine tools.

Value Added Tax is paid four times a year, i.e., quarterly.

All businesses whose turnover exceeds 10,000 MCI must be registered for VAT. This rule applies regardless of whether the company applies the general tax regime or a special tax regime.

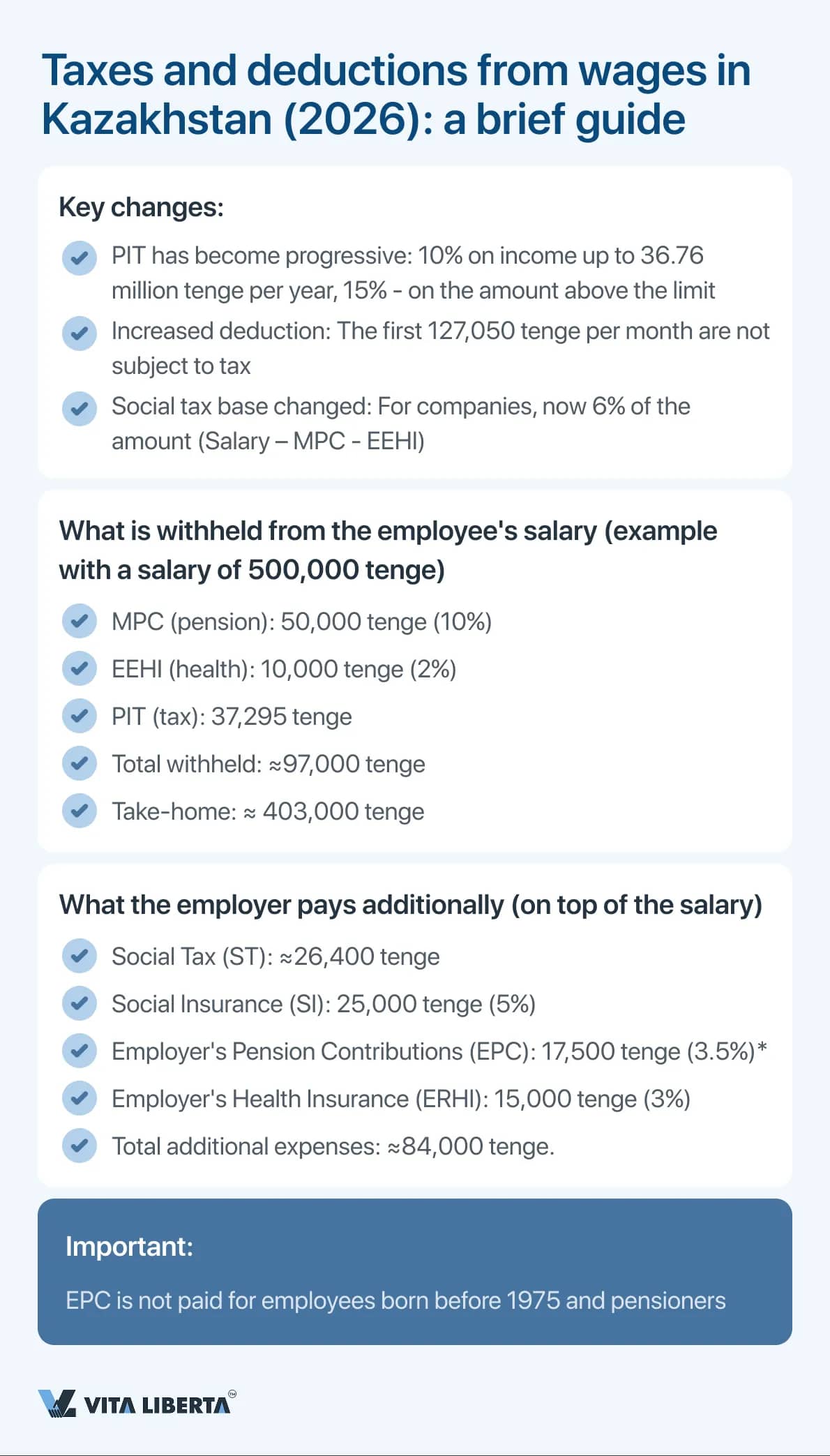

Taxes and Deductions from Wages in Kazakhstan

From January 1, 2026, key changes in the taxation of the wage fund come into force in Kazakhstan. Employers on the general regime and individual entrepreneurs hiring employees need to take into account new rates, limits, and the principle of progressive taxation. All calculations are based on indicators established by the state:

The main innovation is the introduction of a second PIT rate for high incomes.

Important: For all employees, there is an increased standard tax deduction of 30 MCI (127,050 tenge per month), on which income is not subject to PIT. This is the first money that the employee receives "net".

2. Social Tax (ST): new calculation base

From 2026, social tax is calculated differently for individual entrepreneurs and legal entities (LLP, JSC).

In addition to taxes, the law requires the employer to make contributions to social funds. There are minimum and maximum limits tied to the minimum wage. The minimum base for calculation is 1 minimum wage (85,000 tenge), the maximum varies (e.g., 50 minimum wages for pension contributions).

Let's take a salary of 500,000 tenge per month for clarity.

A. What the employee receives (deductions from salary)?

Salary 500,000 tenge + Additional expenses 83,900 tenge = 583,900 tenge.

Key conclusion for business: The real cost of an employee for a company exceeds their official salary by more than 16-17% (in this example, 83,900 tenge from 500,000 tenge). At the same time, the employee receives only about 80% of the accrued amount in hand. Accounting for this total burden is critically important for correctly forming the financial model, budgeting, and pricing. All calculations, especially for PIT and ST, must be carried out taking into account the new rules from the beginning of 2026.

From January 1, 2026, key changes in the taxation of the wage fund come into force in Kazakhstan. Employers on the general regime and individual entrepreneurs hiring employees need to take into account new rates, limits, and the principle of progressive taxation. All calculations are based on indicators established by the state:

- Minimum Wage: 85,000 tenge (maintained at the 2025 level).

- Monthly Calculation Index: 4,235 tenge (increased from 3,932 tenge).

The main innovation is the introduction of a second PIT rate for high incomes.

- Annual income up to 36.76 million tenge (8,500 MCI): Rate 10%.

- Annual income over 36.76 million tenge: A rate of 15% applies to the excess amount.

Important: For all employees, there is an increased standard tax deduction of 30 MCI (127,050 tenge per month), on which income is not subject to PIT. This is the first money that the employee receives "net".

2. Social Tax (ST): new calculation base

From 2026, social tax is calculated differently for individual entrepreneurs and legal entities (LLP, JSC).

- For individual entrepreneurs for themselves: A fixed amount of 1 MCI (4,235 tenge) per month.

- For LLP/JSC per employee: Rate of 6%, but not on the entire salary. The base for calculation is the employee's salary minus their pension contributions minus their medical insurance contributions. At the same time, the resulting base must not be less than 14 MCI (59,290 tenge).

Example: With a salary of 600,000 tenge, after deducting pension contributions (60,000 tenge) and medical insurance contributions (12,000 tenge), the base will be 528,000 tenge. Social tax = 528,000 * 6% = 31,680 tenge (paid by the employer).

In addition to taxes, the law requires the employer to make contributions to social funds. There are minimum and maximum limits tied to the minimum wage. The minimum base for calculation is 1 minimum wage (85,000 tenge), the maximum varies (e.g., 50 minimum wages for pension contributions).

- Pension system:

- MPC (mandatory pension contributions): 10% of salary, withheld from the employee (maximum 425,000 tenge/month).

- EPC (employer's pension contributions): 3.5% of salary, paid by the employer (maximum 148,750 tenge/month). Not accrued for employees born before 1975 and pensioners.

- Social Insurance (SI): 5% of salary, paid by the employer. Minimum payment — 4,250 tenge, maximum — 212,500 tenge per month. These contributions form the fund for sick leave, pregnancy, and childbirth benefits.

- Health Insurance (HI): Bilateral financing.

- EEHI (employee's health insurance contribution): 2%, withheld from salary (max. 85,000 tenge/month).

- ERHI (employer's health insurance contribution): 3%, paid by the employer (max. 254,100 tenge/month).

Let's take a salary of 500,000 tenge per month for clarity.

A. What the employee receives (deductions from salary)?

- MPC (10%): 50,000 tenge

- EEHI (2%): 10,000 tenge

- PIT: (500,000 - 127,050 (deduction)) * 10% = 37,295 tenge

- Total withheld: 50,000 + 10,000 + 37,295 = 97,295 tenge

- Take-home pay: 500,000 - 97,295 = 402,705 tenge

- Social Tax (ST): (500,000 - 50,000 - 10,000) * 6% = 26,400 tenge

- Social Insurance (SI) contributions (5%): 25,000 tenge

- Employer's Pension Contributions (EPC) (3.5%): 17,500 tenge

- Employer's Health Insurance (ERHI) contributions (3%): 15,000 tenge

- Total additional employer expenses: 26,400 + 25,000 + 17,500 + 15,000 = 83,900 tenge

Salary 500,000 tenge + Additional expenses 83,900 tenge = 583,900 tenge.

Key conclusion for business: The real cost of an employee for a company exceeds their official salary by more than 16-17% (in this example, 83,900 tenge from 500,000 tenge). At the same time, the employee receives only about 80% of the accrued amount in hand. Accounting for this total burden is critically important for correctly forming the financial model, budgeting, and pricing. All calculations, especially for PIT and ST, must be carried out taking into account the new rules from the beginning of 2026.

Taxes for Property Owners

In the course of doing business, an organization may own various types of property - from land plots to vehicles. All these assets are subject to taxation in accordance with current legislation.

Entrepreneurs who own land are obliged to pay land tax. Its amount is not fixed and depends on many factors, including the category of land, its cadastral value, and other characteristics.

Property tax applies to all types of real estate - buildings, structures, residential houses, and other objects. It is important that tax payment is mandatory even if such objects are not used for commercial purposes and do not generate profit. The tax rate is 1.5% of the average annual book value of the object.

Vehicles registered in Kazakhstan are also subject to tax. As with land, the rate is not a single indicator - it is determined depending on the type of vehicle, engine size, and other parameters.

In the course of doing business, an organization may own various types of property - from land plots to vehicles. All these assets are subject to taxation in accordance with current legislation.

Entrepreneurs who own land are obliged to pay land tax. Its amount is not fixed and depends on many factors, including the category of land, its cadastral value, and other characteristics.

Property tax applies to all types of real estate - buildings, structures, residential houses, and other objects. It is important that tax payment is mandatory even if such objects are not used for commercial purposes and do not generate profit. The tax rate is 1.5% of the average annual book value of the object.

Vehicles registered in Kazakhstan are also subject to tax. As with land, the rate is not a single indicator - it is determined depending on the type of vehicle, engine size, and other parameters.

Frequently Asked Questions (FAQ)

Can I register an LLP without the personal presence of the founder?

How long does LLP registration take?

Is it mandatory to make a seal for an LLP?

Disclaimer

All service pricing and information provided on vitaliberta.kz are for informational purposes only and do not constitute a public offer under Article 395 of the Civil Code of the Republic of Kazakhstan.

While the website has been prepared with due regard to current legislation and relevant case law, LLP “Vita Liberta” does not guarantee the absolute accuracy, completeness, or timeliness of the content. For definitive guidance, please consult with our team directly.

All service pricing and information provided on vitaliberta.kz are for informational purposes only and do not constitute a public offer under Article 395 of the Civil Code of the Republic of Kazakhstan.

While the website has been prepared with due regard to current legislation and relevant case law, LLP “Vita Liberta” does not guarantee the absolute accuracy, completeness, or timeliness of the content. For definitive guidance, please consult with our team directly.