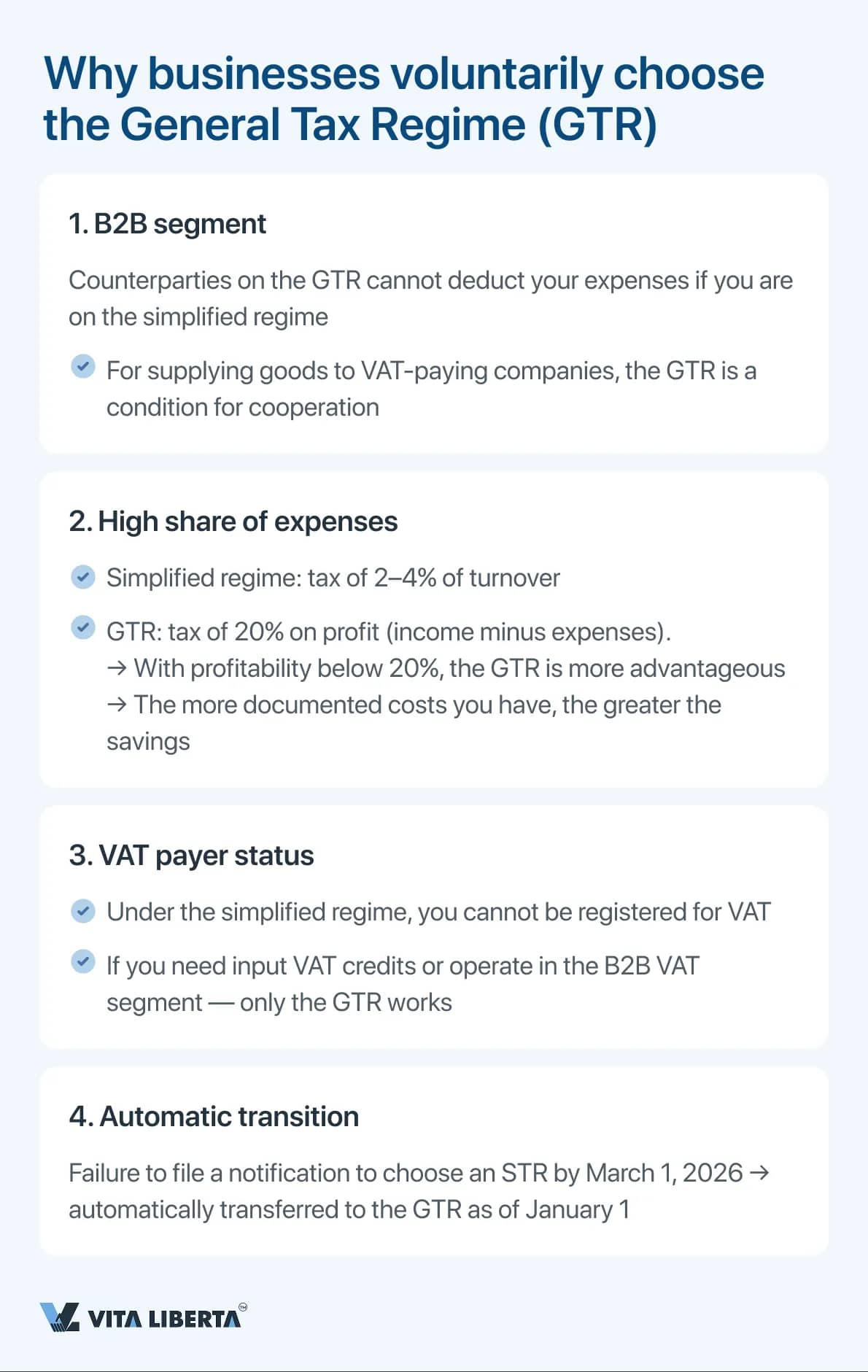

Can GTR counterparties refuse to cooperate with me if I remain on the simplified regime? Is it true that working with me will become unprofitable?

Yes, it is true, and since 2026 the situation has taken on harsh forms. For large businesses, you cease to be a "green" partner and turn into a tax burden. Refusals will not be related to the quality of your product, but to the pure mathematics of corporate taxation.

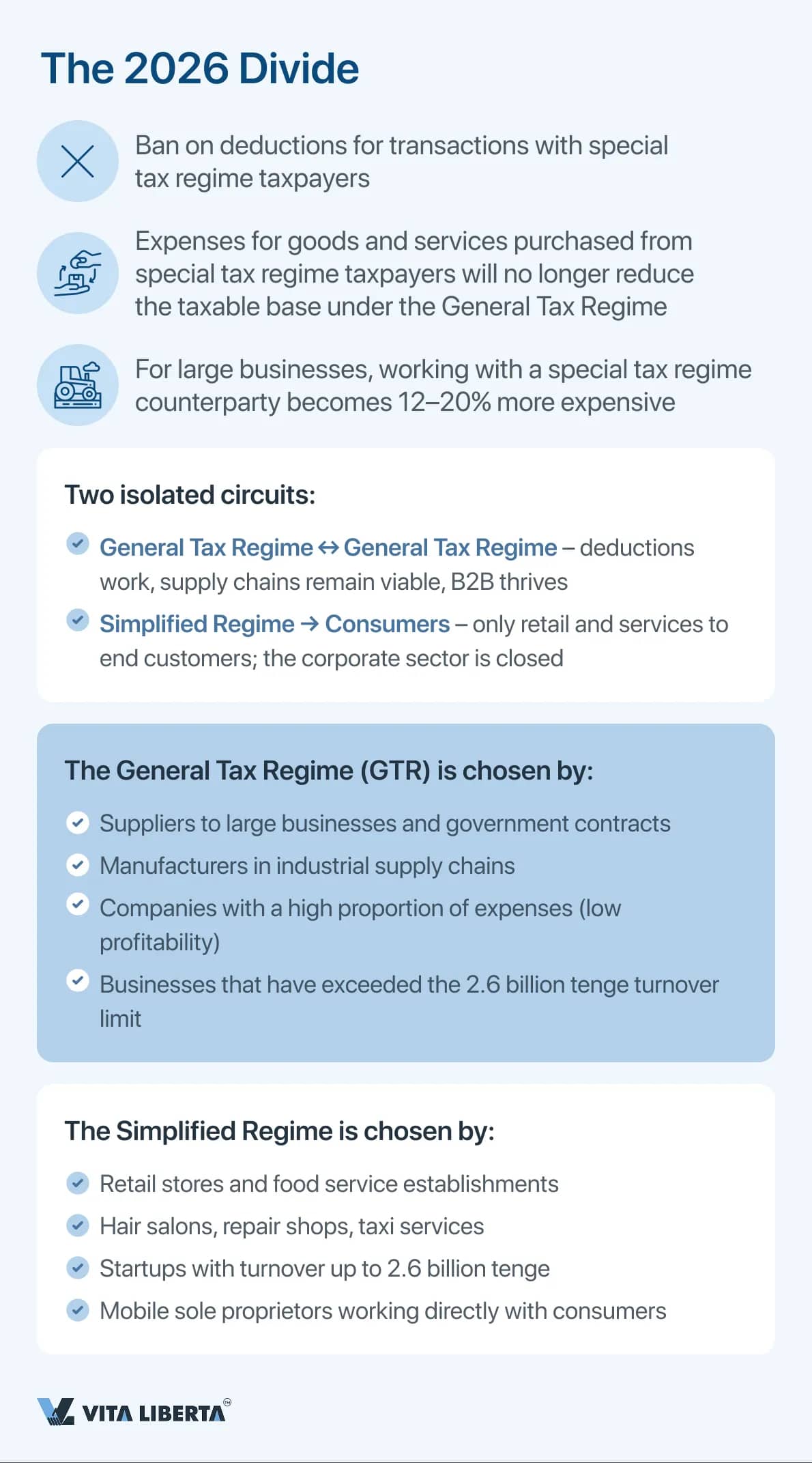

Why You Become an "Expensive" Supplier

Previously, large companies (GTR, CIT payers at 20%) could take your invoices and confidently claim them as deductions. They didn't care whether you paid taxes or not — the main thing was that the expenses "offset" their profit.

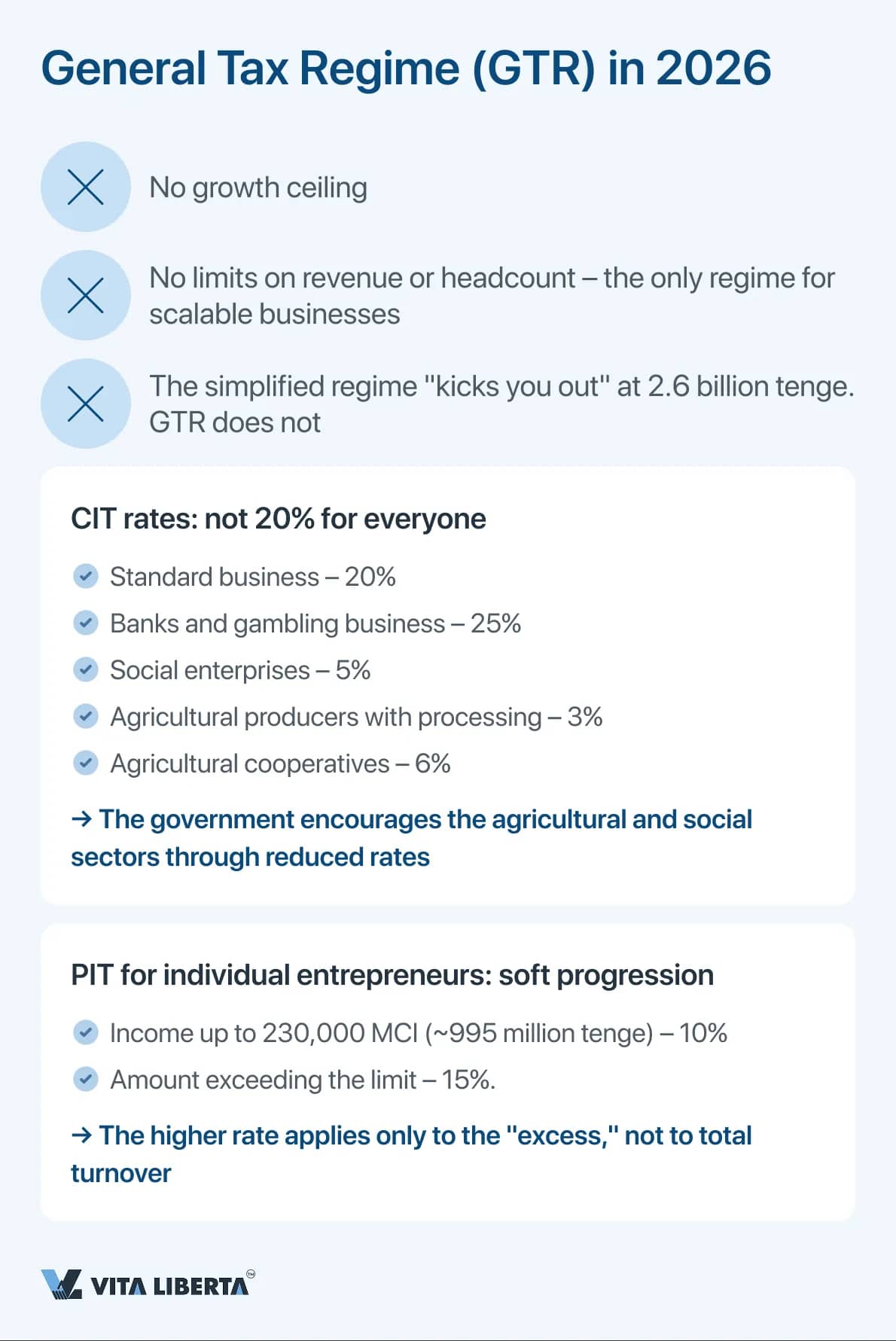

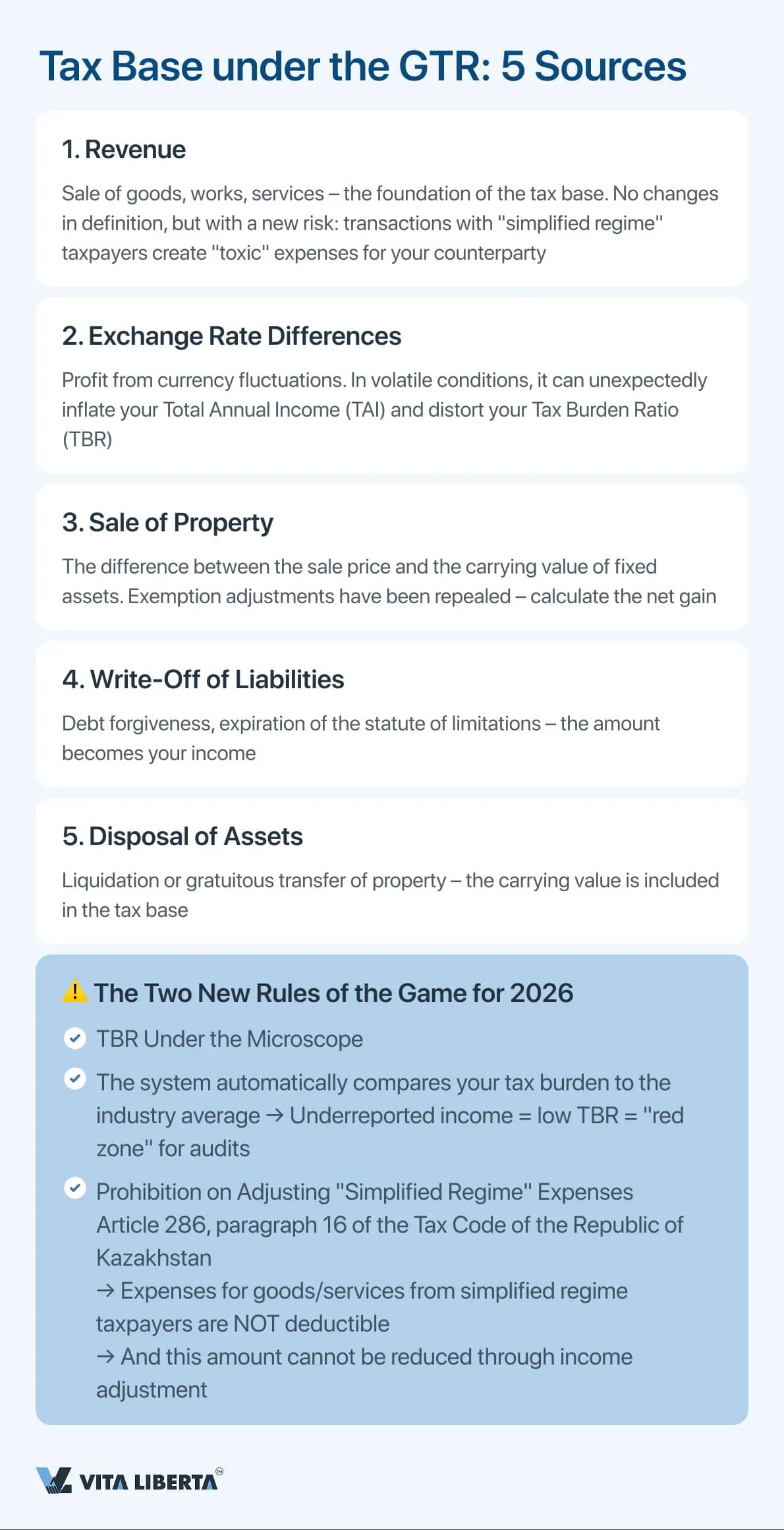

Since 2026, the Tax Code has closed this loophole. Now the principle is: "No tax — no deduction."

1. Loss of CIT Deduction (The Biggest Disadvantage)

Imagine that "Asia" LLP earned 10 million tenge. If it buys chairs from you for 1 million tenge, previously the taxable profit became 9 million, and tax (CIT) was paid on 9 million.

Now: the cost of your chairs for the LLP is like buying air. The deduction does not work. This means the tax base remains 10 million. Effectively, the LLP pays tax on money it has already given to you.

→ The result: Your transaction costs the customer an extra +20% in the form of uselessly paid CIT.

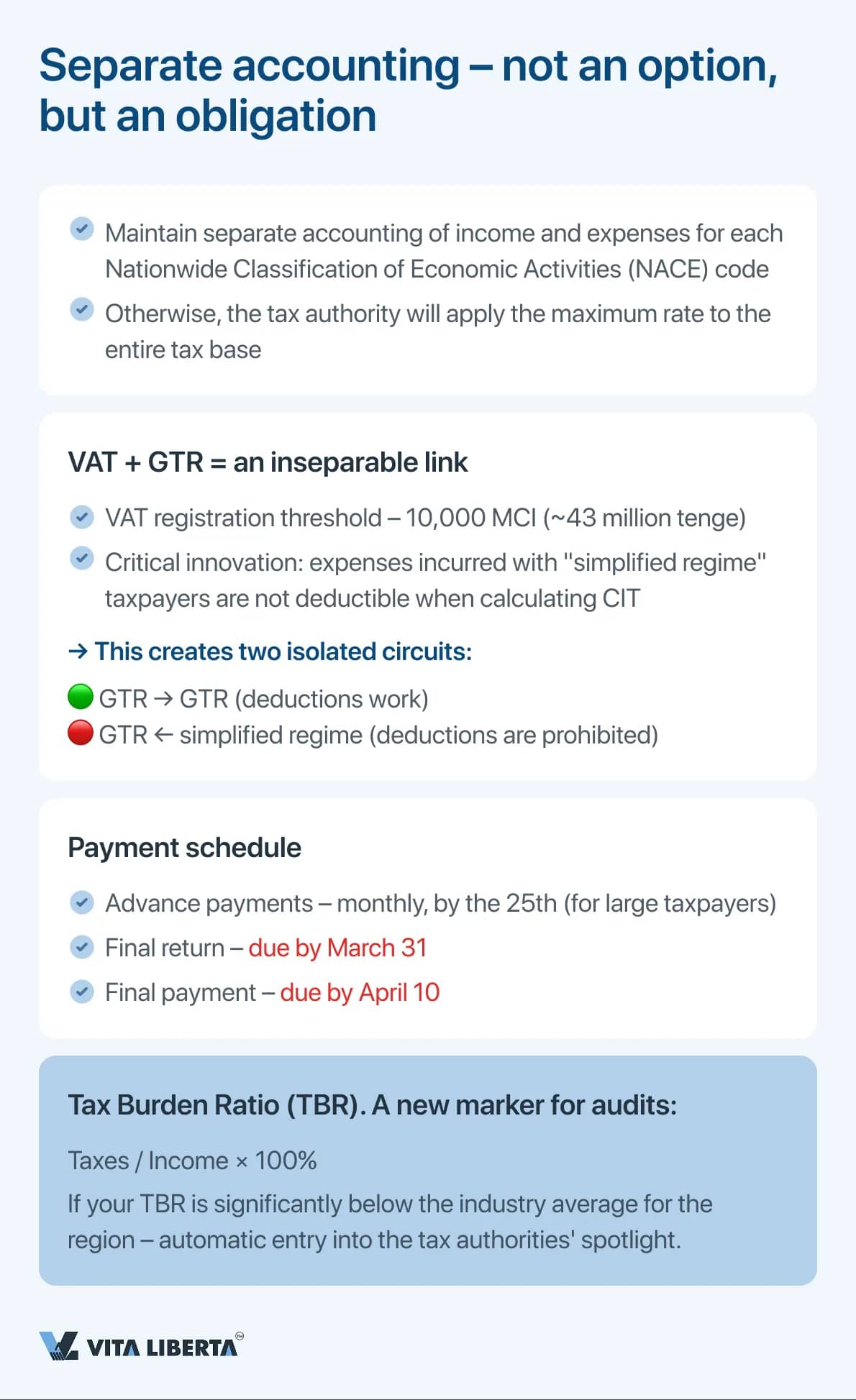

2. "Lost" VAT (The Second Blow)

If your customer is a VAT payer and you operate without VAT, their accountant sees it like this:

— We sold goods for 12 million (including VAT of 2 million).

— We bought materials from you for 6 million (without VAT).

Tax payable to the budget is calculated "top down": 2 million minus 0 = 2 million VAT due.

If you had issued an invoice with VAT, the customer would have reduced their 2 million by your "input" VAT. But this way — they pay the full amount.

This is not just "unprofitable" — it's a blow to liquidity.

What to Expect from Counterparties?

Large customers now divide suppliers into two categories:

— "White partners" (GTR/VAT) — they willingly work with them, even overlook minor issues, because the tax burden is reduced.

— "Simplified regime without VAT" — they work with them only if there is no choice, or they demand a 20–25% discount.

Real scenario for 2026:

They will call you and say: "We found a supplier just like you, but he is on the GTR and provides VAT. His price is 1 million, yours is 950 thousand. Even with the overpayment, it is more profitable for us to take from him because we will save on taxes." And this is not an excuse — it's pure accounting.

Who on the Simplified Regime Has Nothing to Fear?

1. B2C (individuals) — people don't care what regime you are on; they need a low price.2. Mass market, small retail — buyers do not take closing documents.3. Subcontracting, working with micro-businesses — if your clients are themselves on the simplified regime, they have the same problems, but at least they won't complain to you.Your Move:

If 30–40% of your turnover comes from large LLPs or public procurement (GTR):

— Prepare to give a discount equal to the amount of their tax overpayment, or

— Consider voluntarily transitioning to the GTR with VAT. This will give you the right to issue VAT invoices, and customers will again be able to claim expenses as deductions.

If you remain on the simplified regime — look for niches where price is primary and "paper cleanliness" is secondary.

Summary in one sentence:

They will refuse only in one case — if you are selling a unique product that no one else has. In all other cases, your simplified tax regime becomes a hidden loss for them.

Why You Become an "Expensive" Supplier

Previously, large companies (GTR, CIT payers at 20%) could take your invoices and confidently claim them as deductions. They didn't care whether you paid taxes or not — the main thing was that the expenses "offset" their profit.

Since 2026, the Tax Code has closed this loophole. Now the principle is: "No tax — no deduction."

1. Loss of CIT Deduction (The Biggest Disadvantage)

Imagine that "Asia" LLP earned 10 million tenge. If it buys chairs from you for 1 million tenge, previously the taxable profit became 9 million, and tax (CIT) was paid on 9 million.

Now: the cost of your chairs for the LLP is like buying air. The deduction does not work. This means the tax base remains 10 million. Effectively, the LLP pays tax on money it has already given to you.

→ The result: Your transaction costs the customer an extra +20% in the form of uselessly paid CIT.

2. "Lost" VAT (The Second Blow)

If your customer is a VAT payer and you operate without VAT, their accountant sees it like this:

— We sold goods for 12 million (including VAT of 2 million).

— We bought materials from you for 6 million (without VAT).

Tax payable to the budget is calculated "top down": 2 million minus 0 = 2 million VAT due.

If you had issued an invoice with VAT, the customer would have reduced their 2 million by your "input" VAT. But this way — they pay the full amount.

This is not just "unprofitable" — it's a blow to liquidity.

What to Expect from Counterparties?

Large customers now divide suppliers into two categories:

— "White partners" (GTR/VAT) — they willingly work with them, even overlook minor issues, because the tax burden is reduced.

— "Simplified regime without VAT" — they work with them only if there is no choice, or they demand a 20–25% discount.

Real scenario for 2026:

They will call you and say: "We found a supplier just like you, but he is on the GTR and provides VAT. His price is 1 million, yours is 950 thousand. Even with the overpayment, it is more profitable for us to take from him because we will save on taxes." And this is not an excuse — it's pure accounting.

Who on the Simplified Regime Has Nothing to Fear?

1. B2C (individuals) — people don't care what regime you are on; they need a low price.2. Mass market, small retail — buyers do not take closing documents.3. Subcontracting, working with micro-businesses — if your clients are themselves on the simplified regime, they have the same problems, but at least they won't complain to you.Your Move:

If 30–40% of your turnover comes from large LLPs or public procurement (GTR):

— Prepare to give a discount equal to the amount of their tax overpayment, or

— Consider voluntarily transitioning to the GTR with VAT. This will give you the right to issue VAT invoices, and customers will again be able to claim expenses as deductions.

If you remain on the simplified regime — look for niches where price is primary and "paper cleanliness" is secondary.

Summary in one sentence:

They will refuse only in one case — if you are selling a unique product that no one else has. In all other cases, your simplified tax regime becomes a hidden loss for them.