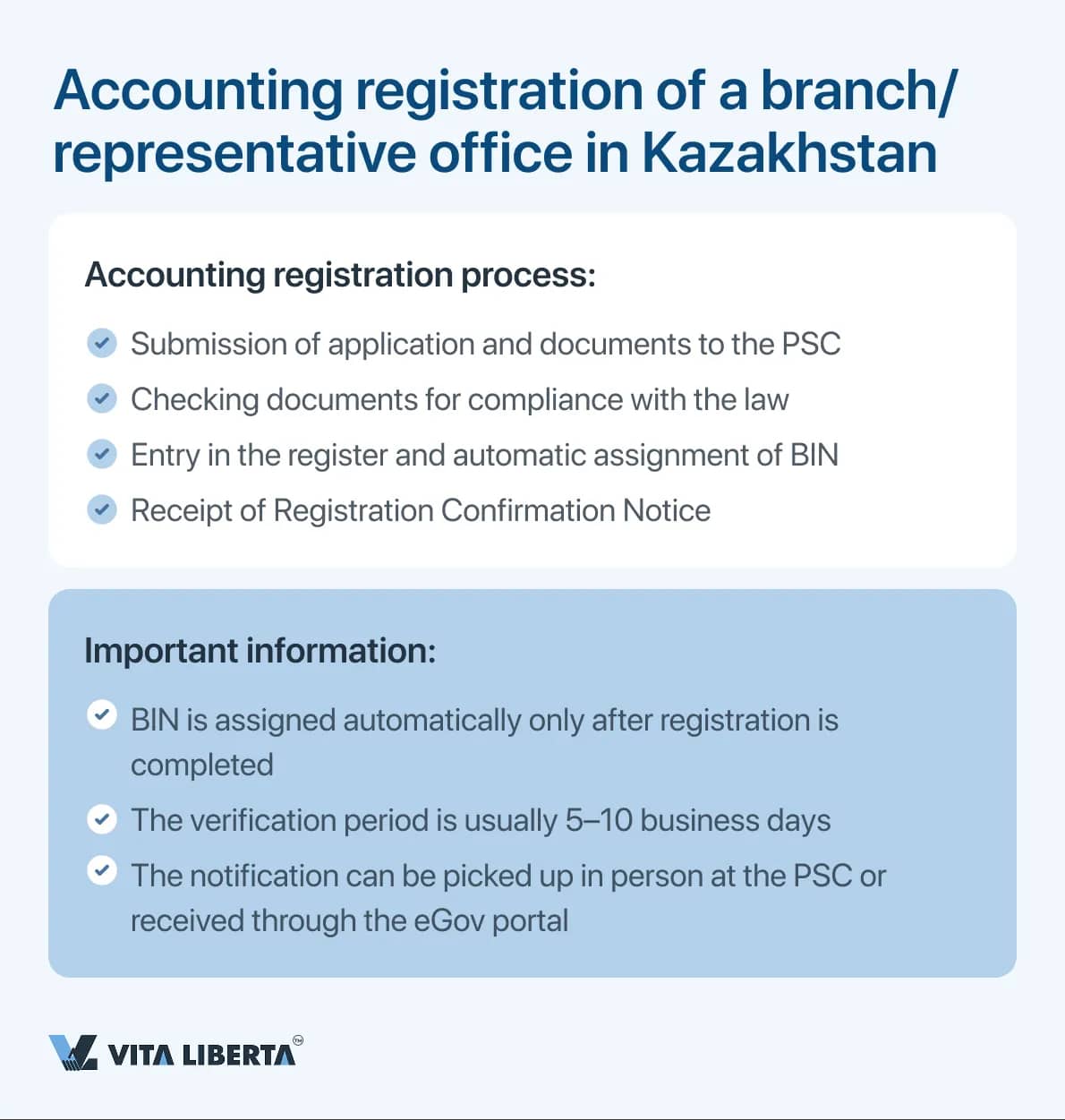

Branches of foreign companies in Kazakhstan keep accounting records and pay taxes on an equal basis with legal entities - residents of Kazakhstan, but with some peculiarities.

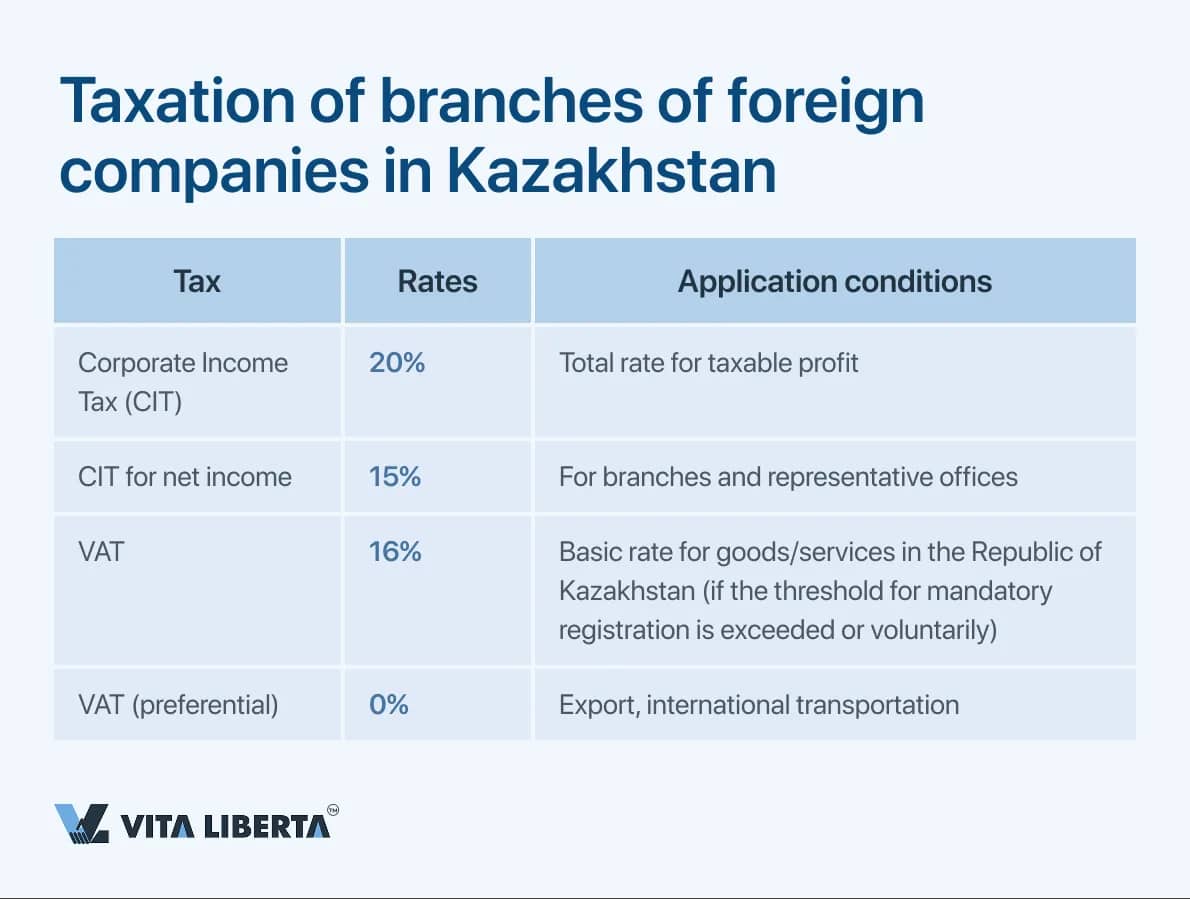

Corporate income tax Branches are obliged to work under the general CIT (corporate income tax) tax regime at a rate of

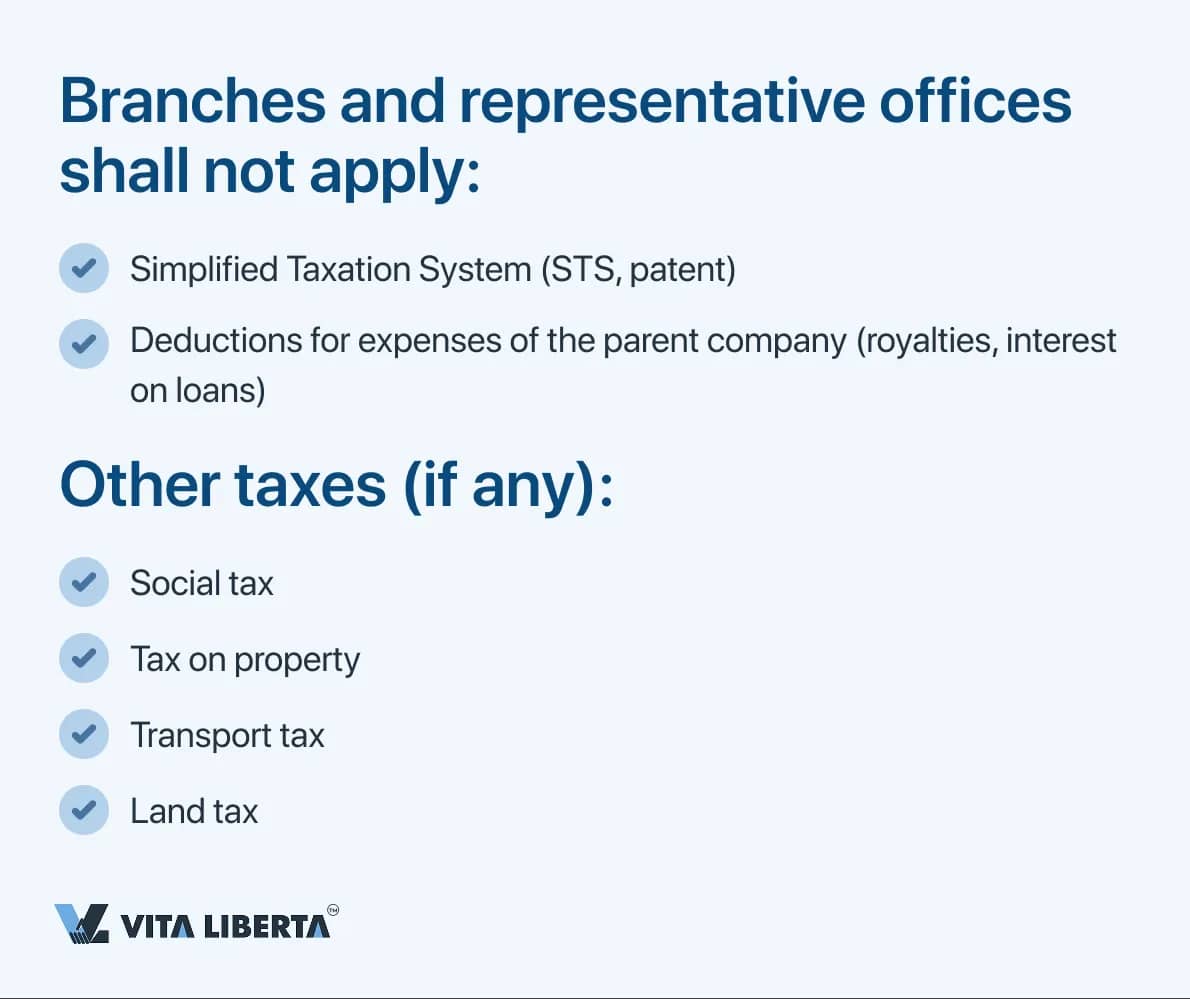

20% of taxable profit. According to paragraph 4 of Art. 683 of the Tax Code of the Republic of Kazakhstan, branches and representative offices of foreign companies are not entitled to apply simplified taxationsystem (STS) intended for small and medium-sized businesses.

The law expressly prohibits the use of special regimes for: - Legal entities with structural subdivisions (including branches).

- The structural subdivisions (branches and representative offices) themselves.

- Taxpayers with separate subdivisions in different settlements.

Exception: if the company only leases the property, the prohibition does not apply.

The branch cannot take into account the following types of expenses as deductions: - Royalties, fees, charges for the use of intellectual property of the parent company;

- Payments for services rendered by the parent company;

- Interest on loans from the parent company;

- Expenses not related to the activities of the branch in Kazakhstan;

- Undocumented expenses;

- General administrative and management expenses of the parent company that are not related to the activities of the branch.

Corporate income tax on net income of a branch According to paragraph 1 of Article 199 of the Tax Code of the Republic of Kazakhstan, net income received by a legal entity that is not a tax resident of the Republic of Kazakhstan from activities through a permanent establishment is taxed on

net income at a rate of 15%. The following formula is used to calculate net income:

- Net income = taxable income – (income and expenses recorded in accordance with Article 133 of the Tax Code of the Republic of Kazakhstan) – (losses carried forward in the manner prescribed by Article 137 of the Tax Code of the Republic of Kazakhstan).

Further, the amount of net income tax is deducted from the obtained value, which is calculated as:

- Tax rate (15%) × (taxable income – income and expenses under Article 133 – losses under Article 137).

Thus, net income is the net profit remaining after taking into account all expenses allowed for deduction and carry-over losses, and is taxed at the established rate.

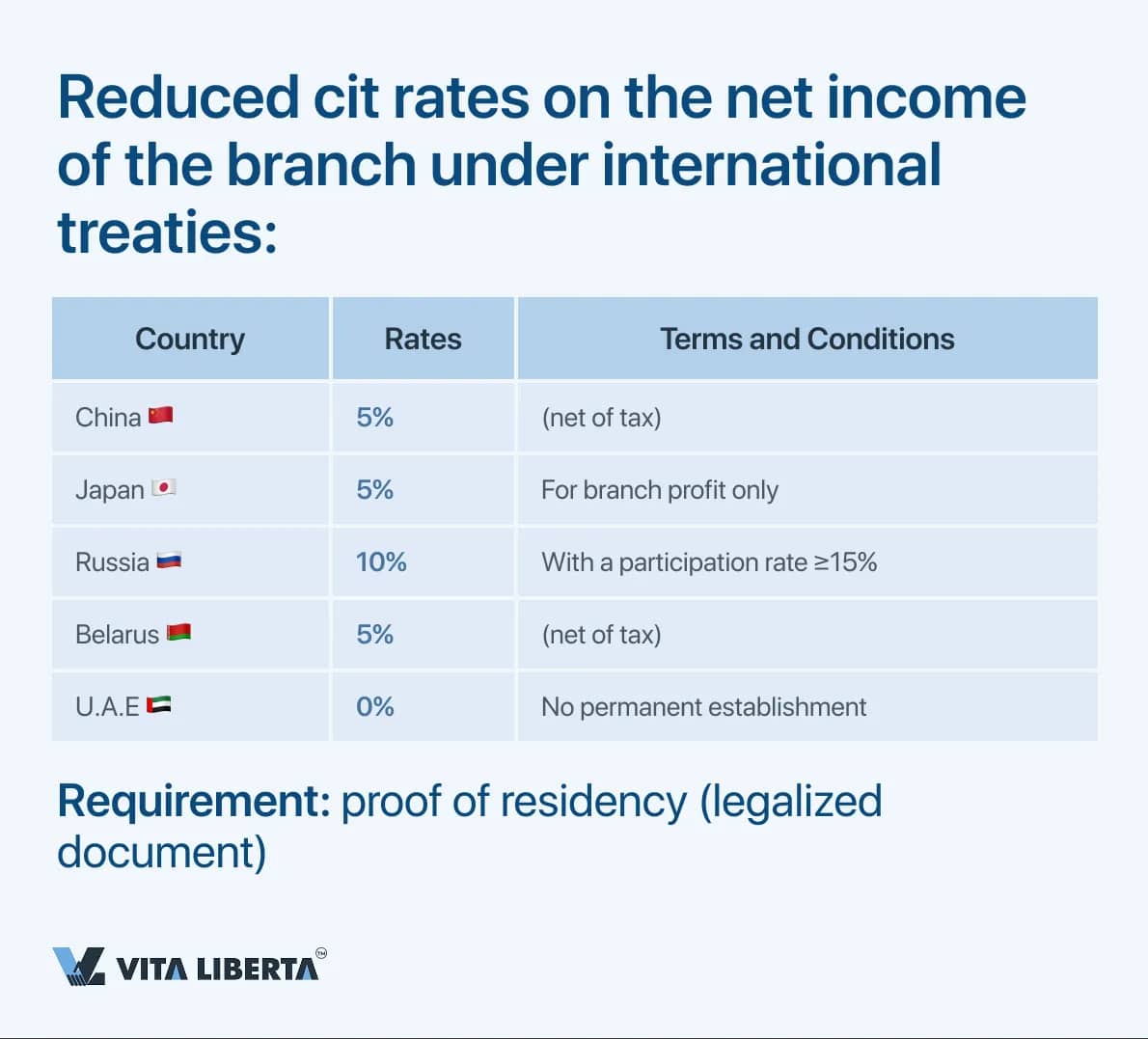

Reduced rates under international treaties According to paragraph 1 ofArticle 214 of the Tax Code of the Republic of Kazakhstan, a non-resident legal entity has the right to apply a reduced net income tax rate if:

- it is a resident of a country with which the Republic of Kazakhstan has concluded an international treaty;

- this agreement provides for a different taxation procedure, different from Article 199 of the Tax Code of the Republic of Kazakhstan.

For example, a reduced rate may be applied for a branch whose parent organization is registered in the following countries.

- China – 5% (after-tax profit)

- Japan - 5% (only for branch profit (not transportation)

- Russia -10% (if the share of participation is ≥ 15% (otherwise 15%))

- Belarus – 5% (profit after taxes)

- Turkey - 10%(for branches not related to real estate)

- UAE – 0% (full exemption, if there is no permanent establishment)

- The Netherlands - 5-15% (depending on the type of income)

- Germany - 5-15% (limited benefits)

- France - 5-10% (for some activities)

- South Korea - 5-10% (depending on the type of income)

However, the application of a reduced rate is possible only if the non-resident at the time of filing the declaration has a document confirming residence that meets the requirements of paragraphs 4 and 5 of Article 219 of the Tax Code of the Republic of Kazakhstan. The document confirming residency must be legalized and with a notarized translation into Kazakh and Russian.

Important: - If an international treaty provides for a benefit, it is necessary to submit documents to the tax office of the Republic of Kazakhstan in a timely Without proof of residency, the standard rate of 15% applies.

VAT Thebasic VAT rate in Kazakhstan is 12% and applies to:

- Sale of most goods and services on the territory of Kazakhstan

- Import operations (charged at customs clearance)

- Domestic transportation and transport services

- Construction and installation services

When importing, VAT is calculated on the customs value of goods, taking into account duties and excises (if any), and not on the amount of the company's turnover.

The zero rate (0%) is applied in the following cases: - When exporting goods outside the customs territory of the EAEU

- For international freight and passenger services

- When providing related forwarding services

- For goods processing services placed under the customs procedure of free customs zone

The right to a zero rate must be documented (contracts, customs declarations, consignment notes).

New rules for VAT registration in Kazakhstan from 2026 A key change for business has occurred in Kazakhstan since January 1, 2026: the threshold for mandatory registration as a VAT payer has been halved. This means that many more companies and individual entrepreneurs are now required to register, accrue and pay value added tax.

What has changed in numbers?

- In 2025, it was necessary to register if the annual turnover exceeded 20,000 MCI — this is 78,640,000 tenge (at MCI = 3,932₸).

- Since 2026, the threshold is 10,000 MCI. Due to indexation, the MCI increased to 4,325 tenge, so the cash equivalent of the limit is 43,250,000 tenge. * Important: this norm applies only to turnovers that arose from January 1, 2026.

In simple words: If the annual income of your business exceeds 43.25 million tenge, you must become a VAT payer. This is 35.4 million tenge less than was required last year.

Who does this concern in the first place? - Common mode enterprises that have not previously reached the old threshold.

What should be done?

- Keep an eye on your turnover: Keep a close eye on your total earnings since the beginning of the year.

- Plan ahead: If you're nearing the ₸43.25 million limit, start preparing for a status change.

- Apply: Within 5 business days of the end date of the month in which the excess occurred.

Important: From January 1, 2026, significantly stricter rules for mandatory registration as a VAT payer come into force in Kazakhstan. Amendments to the Tax Code (Article 101 of the Tax Code of the Republic of Kazakhstan) establish strict and tight deadlines for filing an application, the violation of which will lead to financial sanctions.

Scenario 1: Gradually exceeding the annual threshold - If the total income of the taxpayer from the beginning of the calendar year at the end of any month exceeded the limit of 10,000 MCI (43,250,000 tenge), then he is obliged to submit an application for registration to the tax authority within five working days after the end of this month.

Example: At the end of June, the total income of the company amounted to 45 million tenge, which is more than the established threshold. The application must be submitted before the end of the fifth working day of July.

Scenario 2: One-Time Transaction Above Threshold - A special rule has been introduced for large one-time transactions. If it is planned to make one transaction (transaction), the amount of which exceeds the threshold of 43,250,000 tenge, the taxpayer is obliged to register for VAT until the moment of signing the contract or making this transaction. This rule radically changes the approach: registration becomes a prerequisite for the legal conduct of a major transaction, and not its consequence.

Consequences of registration:

- Duty: To charge and pay VAT at a rate of 16% on taxable transactions, to file quarterly returns.

- Right: Accept the "input" VAT paid to your suppliers for offset (deduction), which may improve financial conditions.

This change is aimed at expanding the tax base and formalizing the business. Timely fulfillment of the new requirements will allow you to avoid fines and continue working without hindrance.

Who is no longer subject to mandatory registration and is deprived of the right to voluntary registration? On the basis of Article 99 of the Tax Code of the Republic of Kazakhstan (paragraph 3), the list of persons who are not subject to VAT registration on a mandatory basis has been expanded. These are:

- Persons engaged in private practice (lawyers, notaries, private appraisers, doctors, etc.).

- Taxpayers applying a simplified taxation system (STS).

- Individuals (not registered as individual entrepreneurs).

Important: Even on a voluntary basis, such taxpayers cannot register for VAT.

Other taxes Branches of non-resident legal entities may be subject to other taxes, such as (if there are objects of taxation with these taxes):

- social tax

- property tax

- transport tax

- land tax